Anybody familiar with the underlying trends in the communications business, and who looks at the business dispassionately, sooner or later has to wonder what the future of the fixed network actually will be. That is not to say the fixed network has no obvious role.

Bandwidth, and affordable bandwidth, is the chief advantage a fixed network has, and always will have, over a mobile or wireless network. But that isn't a terribly comforting thought for a fixed network executive, or any of the ecosystem partners. For saying "bandwidth is the enduring value" is tantamount to saying that "dumb pipe" is the enduring value.

That is not to say that applications are unimportant. Video entertainment and voice are key revenue generators for fixed networks. But the irreducible core of value is the "access to the Internet." At the moment, the U.S. Federal Communications Commission even enforces the "dumb pipe" model by barring fixed networks from providing quality of service distinctions.

In other words, fixed network service providers specifically are prohibited from creating and selling "smart pipe" Internet access that can prioritize voice and real-time applications over others. "Managed services" such as carrier voice or entertainment video thankfully are exempted from those rules, but the point remains: dumb pipe is the unique and enduring value provided by a fixed network.

No other network--satellite, fixed wireless or mobile--can claim to match the theoretical bandwidth of an optical fiber network. And no other network can match the price-performance of a fixed network at very-high speeds. You don't hear proponents talking about mass deployment of gigabit per second wireless or satellite networks, for example, because it is not technologically or economically possible.

Some think that could change in some decades, but for the moment fixed networks have the strategic advantage. Some of us would argue that growing use of Wi-Fi-supported devices such as tablets and smart phones will enhance the value proposition for fixed networks.

The increase in number of devices using the home networks is one reason why “median monthly usage” (half of consumers use more, half use less) on North America’s fixed access networks has increased from 10.3 GB to 16.8 GB in the second half of 2012.

Over the same period, “mean monthly usage” (arithmetic average) grew by over 70 percent increasing to 51.3 GB from 32.1 GB. Growing subscriber consumption is not limited to North America or fixed networks, either.

Relatively slow growth of mobile data consumption probably is a direct result of the shift to offloading of mobile data demand to the fixed network.

In North America, monthly usage on mobile networks has experienced only minor growth, Sandvine says. In the second half of 2012, Sandvine has observed mean monthly usage increasing moderately from 312.8 MB to 317.2 MB.

More noticeable change can be seen in the median which has increased to 32.9 MB from 25.5MB just six months ago. But it also is possible that new smart phone consumers account for some of the slower growth of mobile data, as newer users tend to consume less data than experienced users.

As you would guess, consumption of entertainment video and audio remains the largest

traffic category on virtually every network examined. North America continues to lead in adoption of this traffic category, with almost two thirds of downstream traffic during peak period being streaming audio or video.

Netflix now accounts for 33 percent of peak period downstream traffic, Sandvine notes.

Mobile data consumption increased only slightly, very likely a direct consequence of people using at-home Wi-Fi. From a traffic distribution standpoint, the top one percent of mobile data subscribers account for 23.9 percent of total upstream traffic.

The top one percent of downstream users account for 18.7 percent of bandwidth consumption.

The mobile network’s lightest 50 percent of users account for only 0.8 percent of total traffic.

So the value of fixed networks is assured. What is not clear is how the economics of operating a fixed network business might have to evolve, though. Video and high speed Internet access are two apps that the fixed network is ideally suited to supply.

The unique value proposition drops sharply after that, as voice and messaging would seem better supported by mobile devices. Fixed mobile substitution therefore is a key issue. But mobile offload is the countervailing development.

If telcos can get their cost structures revamped, broadband would seem to offer the highest profit margin of any potential service, long term.

Video entertainment margins will be lower since gross revenue has to be shared with program suppliers.

Still, the move to use of "untethered" devices does not mean a move to use of "mobile" networks in a linear fashion.

Once upon a time, consumers and businesses primarily used fixed networks for all communications. These days, mobile networks are used as much, or more. But even "mobile" devices are used mostly at home, or at the office, on Wi-Fi networks that are a logical and direct extension of fixed network service.

That provides one obvious clue about the future value of the fixed network. Though mobile broadband and voice might be sufficient for many people, much of the time, the value-price relationship will, in all likelihood, "always" favor untethered use of the fixed network.

Wednesday, November 14, 2012

What is the Future of the Fixed Network?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

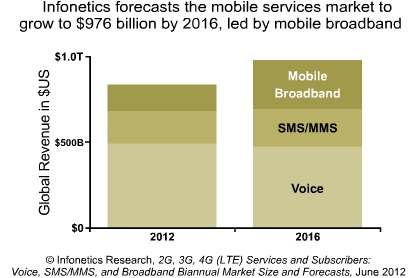

Global Telecom Revenue to Grow 6% or More, Annually

According to International Telecommunications Union forecasts, global communications revenue will grow at least six percent annually through 2015.

According to International Telecommunications Union forecasts, global communications revenue will grow at least six percent annually through 2015. Nearly 80 percent of that revenue will be generated by mobile services in 2015. In 2012, perhaps a third of total revenue will be generated by fixed network services.

In other words, as some of us are fond of saying, communications now is a mobile business with a fixed component.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, November 13, 2012

Mobile Data Will Reach 22% of Total Mobile Service Revenue by 2016

Mobile broadband is the biggest single revenue opportunity in Africa in the immediate and longer term, according to the results of a recent Industry Outlook survey commissioned by Informa Telecoms &Media. By way of contrast, data service revenues represent about 43 percent of service provider revenue in the North American markets.

Informa forecasts that annual mobile data revenues in Africa will reach $18.5 billion by 2016. In 2011 mobile data represented 12 percent of service provider revenue.

Informa forecasts that annual mobile data revenues in Africa will reach $18.5 billion by 2016. In 2011 mobile data represented 12 percent of service provider revenue.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Legacy Regulation a Barrier to Network Modernization?

Nothing is more normal in the communications business than contestants lobbying for regulations that support their own business interests, whatever the "public policy" implications might be. Equally normal is the "lag" between regulatory frameworks that represent a technology neutral approach to getting citizens and consumers the "best" services at the lowest possible price.

It might be tempting to blame regulators for being "behind the curve," but that isn't quite fair. Regulators work in a highly political environment where substantial political pressures have to be accommodated. Many competitive communications providers simply acknowledge that larger enterprises in the communications business have more employees, hence voters, hence influence.

Likewise, small rural telcos have incumbency in their favor: they are the established providers of "last resort" communications services in isolated or rural communities, and regulators are loathe to upset them. None of that has prevented upstart competitors, including satellite, fixed wireless and even "dominant" mobile service providers from making the argument that the best way to provide advanced services in rural areas is to support efficient providers that can deliver services the fastest, at the lowest cost.

But there always are political issues. Economic issues are a factor as well. Though the Federal Communications Commission has in past years given subsidies to mobile and fixed network providers, few argue that such disbursements, supporting two or more providers in an area, make as much sense as choosing one provider and targeting resources.

State regulators increasingly agree, and are regularly granting wireless providers status as carriers of last resort, meaning mobile service providers are eligible for subsidies that in past years have gone exclusively to landline telcos.

Beyond that, competing providers are governed by industry-unique rules. Satellite, cable TV, competitive local exchange carriers and fixed wireless providers, for example, operate under distinct regulatory frameworks, though providing the same services.

In a world without politics, that might not happen. But we do not live in a world without politics. And for that reason, virtually all competitors will complain, from time to time, that the rules are unfair. They are.

It might be tempting to blame regulators for being "behind the curve," but that isn't quite fair. Regulators work in a highly political environment where substantial political pressures have to be accommodated. Many competitive communications providers simply acknowledge that larger enterprises in the communications business have more employees, hence voters, hence influence.

Likewise, small rural telcos have incumbency in their favor: they are the established providers of "last resort" communications services in isolated or rural communities, and regulators are loathe to upset them. None of that has prevented upstart competitors, including satellite, fixed wireless and even "dominant" mobile service providers from making the argument that the best way to provide advanced services in rural areas is to support efficient providers that can deliver services the fastest, at the lowest cost.

But there always are political issues. Economic issues are a factor as well. Though the Federal Communications Commission has in past years given subsidies to mobile and fixed network providers, few argue that such disbursements, supporting two or more providers in an area, make as much sense as choosing one provider and targeting resources.

State regulators increasingly agree, and are regularly granting wireless providers status as carriers of last resort, meaning mobile service providers are eligible for subsidies that in past years have gone exclusively to landline telcos.

Beyond that, competing providers are governed by industry-unique rules. Satellite, cable TV, competitive local exchange carriers and fixed wireless providers, for example, operate under distinct regulatory frameworks, though providing the same services.

In a world without politics, that might not happen. But we do not live in a world without politics. And for that reason, virtually all competitors will complain, from time to time, that the rules are unfair. They are.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobile Data Now 43% of Total U.S. Mobile Revenue

The U.S. mobile data market grew three percent quarter over quarter and 17 percent year over year to reach $19.9 billion worth of revenue in the third quarter of 2012, according to mobile analyst Chetan Sharma.

The U.S. mobile data market grew three percent quarter over quarter and 17 percent year over year to reach $19.9 billion worth of revenue in the third quarter of 2012, according to mobile analyst Chetan Sharma. That’s the good news: mobile data continues to drive revenue growth as messaging and voice revenue matures.

Data is now almost 43 percent of U.S. mobile industry service revenue. But the possibly troubling implication is that the industry is about half way to saturating the mobile data market.

If you want to know why mobile service providers are launching mobile payments, mobile wallet, mobile banking or mobile commerce initiatives, or machine-to-machine services, that is the reason. Another wave of revenue growth, big enough to displace voice, messaging and even mobile broadband, is necessary.

Most western markets have seen messaging revenue decline, though up to this point the U.S. market has resisted the trend. But in the third quarter, for the first time, there was a decline in both the total number of messages sent and received, as well as total messaging revenue.

Voice traffic will dip below 10 percent of the overall traffic in 2012 (revenue is another matter).

For much of the last three decades, voice has dominated the revenue streams for almost all operators, Sharma argues.

In 2013, global voice revenues will fall below 60 percent. So far, the drop in voice revenues has been matched by the rise of messaging revenues and mobile data. But mobile data also will reach saturation at some point, raising the question of what comes next.

The answer to that question is not yet clear. But most observers believe some combination of new applications, using network resources as an input, must be a large part of the answer.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, November 12, 2012

Technology Shifts Can Take 10 to 20 Years

Being late to get into a market can be dangerous, but being too early might be the more prevalent mistake.

Though the tablet might be the fastest-growing consumer appliance of all time, most devices and appliances take quite a long time to reach ubiquity. Consider smart phones, which many rightly consider to be among the faster-growing devices of all time.

BellSouth launched the IBM Simon, with its rudimentary touch screen, in 1993. It didn’t catch on. About 2002, personal digital assistants started to have the ability to make and receive phone calls. RIM shipped its first BlackBerry about that time.

In late 2006 only 715,000 smart phones were sold, though, representing just six percent of U.S. mobile phone sales. Up to that point, the smart phone was spreading not much faster than personal computers had done, according to Technology Review.

Still, keep in mind that It took landline telephones about 45 years to get from five percent to 50 percent penetration among U.S. households, and mobile phones took around seven years to reach a similar proportion of consumers. Smart phones have gone from five percent to 40 percent in about four years.

But it likewise took about 11 years for use of mobile phones to reach 10 percent penetration, so it took about 18 years for use of mobile phones to reach about half of people in the United States.

Since it took about eight years for smart phone penetration to reach 10 percent of people, and then another seven years to reach half of users, it took about 13 years for smart phones to reach half of U.S. consumers. And that has been about the fastest adoption rate of any appliance, in the U.S. market.

Global adoption of mobile phones in the developing world has been stunningly rapid, as well.

In 1982, there were 4.6 billion people in the world, and not a single mobile-phone subscriber.

Today, there are seven billion people in the world and six billion mobile cellular-phone subscriptions. In other words, the world has gone to about 86 percent penetration in about 30 years.

From the standpoint of human progress, that is fast. From the standpoint of any single company, that is a long time. And that is worth keeping in mind. Most truly important consumer technologies take time to reach ubiquity. Would-be market leaders have plenty of time to misjudge market progress, and fail before “ubiquity” is reached.

Though the tablet might be the fastest-growing consumer appliance of all time, most devices and appliances take quite a long time to reach ubiquity. Consider smart phones, which many rightly consider to be among the faster-growing devices of all time.

BellSouth launched the IBM Simon, with its rudimentary touch screen, in 1993. It didn’t catch on. About 2002, personal digital assistants started to have the ability to make and receive phone calls. RIM shipped its first BlackBerry about that time.

In late 2006 only 715,000 smart phones were sold, though, representing just six percent of U.S. mobile phone sales. Up to that point, the smart phone was spreading not much faster than personal computers had done, according to Technology Review.

Still, keep in mind that It took landline telephones about 45 years to get from five percent to 50 percent penetration among U.S. households, and mobile phones took around seven years to reach a similar proportion of consumers. Smart phones have gone from five percent to 40 percent in about four years.

But it likewise took about 11 years for use of mobile phones to reach 10 percent penetration, so it took about 18 years for use of mobile phones to reach about half of people in the United States.

Since it took about eight years for smart phone penetration to reach 10 percent of people, and then another seven years to reach half of users, it took about 13 years for smart phones to reach half of U.S. consumers. And that has been about the fastest adoption rate of any appliance, in the U.S. market.

Global adoption of mobile phones in the developing world has been stunningly rapid, as well.

In 1982, there were 4.6 billion people in the world, and not a single mobile-phone subscriber.

Today, there are seven billion people in the world and six billion mobile cellular-phone subscriptions. In other words, the world has gone to about 86 percent penetration in about 30 years.

From the standpoint of human progress, that is fast. From the standpoint of any single company, that is a long time. And that is worth keeping in mind. Most truly important consumer technologies take time to reach ubiquity. Would-be market leaders have plenty of time to misjudge market progress, and fail before “ubiquity” is reached.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

U.S. LTE Arms Race Heats Up

U.S. mobile service providers are in the midst of a major “arms race” aimed at getting new Long Term Evolution fourth generation networks up and running, as customer adoption shows strong growth.

U.S. mobile service providers are in the midst of a major “arms race” aimed at getting new Long Term Evolution fourth generation networks up and running, as customer adoption shows strong growth.Verizon Wireless, the market leader, says it will complete its national network by mid-2013.

AT&T recently reiterated a timetable that some might call accelerated. T-Mobile USA likewise has stepped up its own efforts to build a nationwide LTE network. And Sprint likewise has purchased significant new assets in the U.S. midwest to support its planned LTE network.

LTE is not a commercial reality many other places in the world, in 2012, though, TeleGeography says.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Will We Break Traditional Computing Era Leadership Paradigm?

What are the odds that the next Google, Meta or Amazon--big new leaders of new markets--will be one of the leaders of the present market, b...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...