Nobody argues that end user bandwidth demand will keep growing. The issues are "how much" and "how fast" the demand will grow.

For many, the issue therefore is how to achieve a three order of magnitude increase in delivered end use bandwidth, over a relatively short time frame. the problem is most acute for wireless service providers, of course.

Expand image to read by clicking lower right corner of document.

userbandwidth.

Friday, April 12, 2013

1000 Times More Bandwidth Needed?

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

“Transparency,” Not “Choice” or “Savings” is Value of “Non-Subsidized” Phones

O2 in the Unitted Kingdom has launched “O2 Refresh,” a new service plan that decouples a two-year service contract from the consumer purchase of a phone.

O2 Refresh therefore offers two separate plans, one for the phone and one for the airtime.

The issue really is “transparency,” not savings, as some have suggested would be the consumer value of moving to “unlocked phone” policies.

“By signing up to and paying separately for their phone and airtime, customers are given complete transparency, while paying the same overall as they would on a standard 24 month pay monthly tariff,” O2 says.

That’s the key. Some observers have argued that consumers should be able to buy fully unlocked phones and use them on any mobile network, or buy service without a contract.

With some technology constraints where both GSM and CDMA are used, ipeople generally can do that.

What O2’s new plan shows is that the “remedy” of separating device purchases from service plans doesn’t actually provide all that much consumer benefit. If consumers can afford full retail price for phones, they already are free to buy them. If they want service without contracts, they already can buy such service (prepaid, generally).

Under the O2 Refresh plan, users actually will not save money, and still will have a contract. The incremental advantage for O2 is that it can advertise lower monthly fees for service. The advantage for a consumer is the ability to upgrade a phone at any time.

“Increasingly our customers are telling us that they don’t want to be tied to the same phone for two years,” said Feilim Mackle, Telefónica UK sales and service director.

Customers will have a choice of three O2 Refresh Airtime Plans, which have been tailored to meet varying call, text and data requirements. For £12 a month, customers get 600 minutes, unlimited texts and 750MB of data; for £17, customers will have unlimited minutes, unlimited texts and 1GB of data and for £22 they receive unlimited minutes, unlimited texts and 2GB of data.

At launch, O2 Refresh will be available on a range of phones including the HTC One, Sony Xperia Z, Blackberry Z10, Samsung Galaxy S3 and Apple iPhone 5. Following the launch, O2 Refresh will be extended to include a wider range of phones, with a specific focus on high-end smartphones including the Samsung Galaxy S4.

In essence, that approach is what T-Mobile USA is doing with its “no-contract” approach to mobile service pricing. Consumers can buy a full-price retail phone or under an installment contract, with service then offered without a contract.

As you might guess, the actual out of pocket monthly payments for T-Mobile USA service might not change very much.

If one assumes most consumers still are going to opt for device installment plans rather than buying their devices outright, the savings are relatively slight, on a recurring basis, for purchases involving high-end devices.

T-Mobile USA has a $60-a-month 2.5 gigabyte data plan is more than $300 cheaper over two years than an AT&T plan that offers 3 gigabytes and 450 minutes of talk time with the same device. For a user who opts for the installment plan, that works out to about $12.50 a month lower bills than for the rival AT&T plan.

There is an argument that T-Mobile USA plans will save more, compared to service from Verizon Wireless. A user buying that same T-Mobile USA plan, and using the installment plan, would save perhaps $20.83 a month, over two years, compared to a single-user Verizon Wireless plan with 2 gigabytes of data (though the Verizon Wireless plan also would offer unlimited talking and text messaging).

Transparency is a good thing, of course. But the notion that phone unbundling and an end to contracts necessarily provides huge end user value is not so clear.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, April 11, 2013

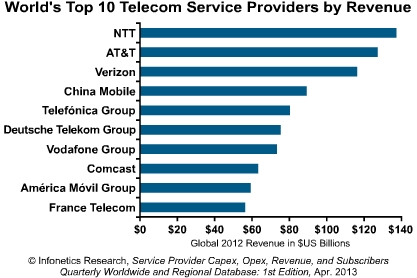

Largest 10 Telecom Service Providers: 90% Own Mobile Assets

Of the 10 largest telecom service providers in the world, only one does not have a facilities-based, owned-spectrum mobility business. On the other hand, one of the 10 is a “cable TV company.”

Both of those trends--mobility and cable TV--tell the story of how the global telecom business has changed over the past several decades.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Can Distributors Force Video Channel Unbundling?

Distributors might think channel unbundling is a good thing. But it doesn't matter. Programming networks think unbundling is a bad idea, and they control the programming people mostly want to watch. Distributors might think sports programming costs are exorbitant. Program networks do not.

Distributors might think channel unbundling is a good thing. But it doesn't matter. Programming networks think unbundling is a bad idea, and they control the programming people mostly want to watch. Distributors might think sports programming costs are exorbitant. Program networks do not. Some video distributors are willing to consider letting consumers buy channels one at a time. Few networks would do so voluntarily.

It isn't so clear how much leverage video distributors actually have, with one interesting exception, namely the efforts by Aereo and Aereokiller to disrupt the broadcast TV distribution system. What makes that a structurally different situation is that cable, satellite and telco providers, plus ISPs such as Google Fiber and others, must have direct contractual relationships with the programming networks.

Aereo and Aereokiller are trying to pioneer a way to deliver video without the need for a direct business relationship with the broadcaster. That's different, way different, in terms of the structure of the relationship.

In a sense, Aereo and Aerokiller operate much as any third party application on the Internet, with no direct business relationship with an access provider.

To be sure, there always is the theoretical possibility of government intervention to force unbundling, but that seems unlikely.

But Aereo and Aerokiller conceivably could provide a breakthrough of sorts. Assume for the moment that the concept survives legal challenge (whether or not either firm emerges in the end to take advantage of the opportunity).

Assume Aereo, Aerokiller or others can then amass a content offering including local TV channels, plus some other popular "cable channels," but without sports networks which drive much of the cost of traditional video subscription packages.

That could create a huge opportunity for lower-cost video services, and that in turn would increase pressure on programming networks to make some accommodations with distributors. Perhaps challenged by potential new lower-cost services, major programming networks would become more flexible about the ways they allow distributors to sell content, possibly including some forms of a la carte access.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

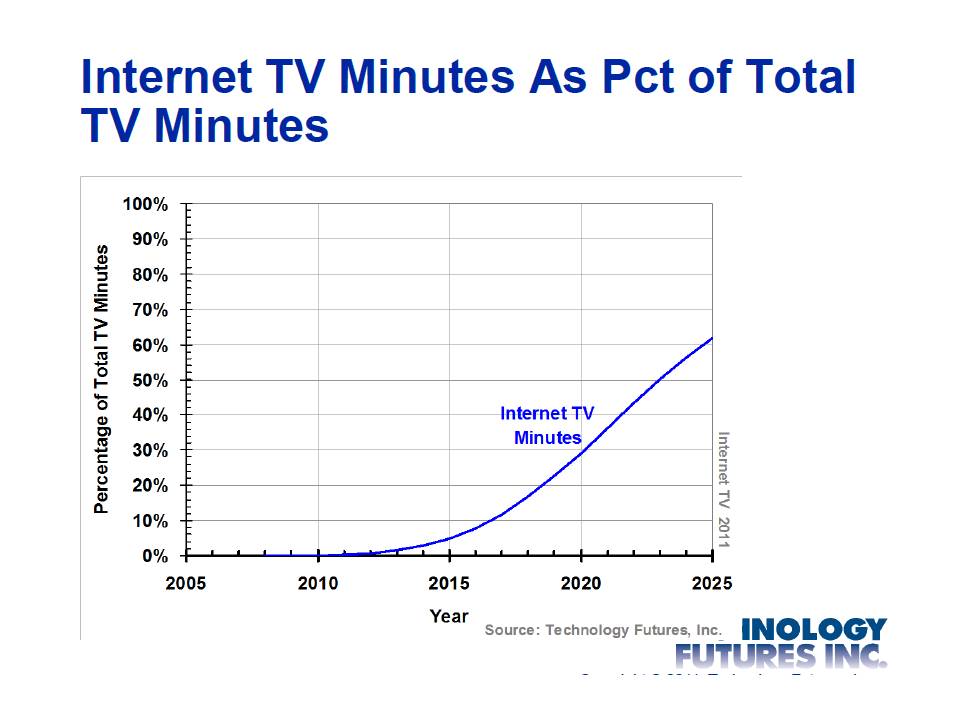

By 2023, 1/2 of all U.S. TV Viewing Will Use the Internet

By about 2023, half of all U.S. TV viewing will be of online video, Technology Futures predicts. In large part, that will be because virtually every household using the Internet will be watching Internet TV or Internet video.

By about 2020, half of all U.S. “television homes” will be “Internet TV homes” as well.

If you want to ask what households and users will be doing with all that bandwidth, the answer is “watching TV.” In fact, by about 2020, it is quite conceivable that 60 percent of all video being watched by an Internet-connected user will be viewed online.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, April 10, 2013

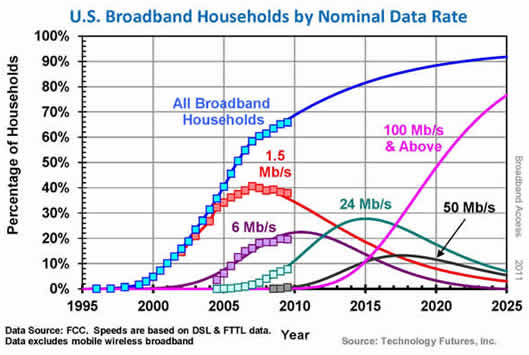

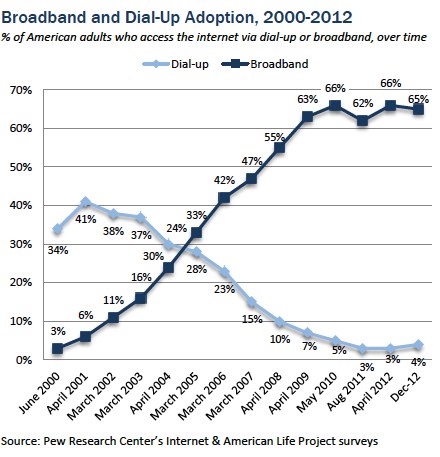

At Least 1/2 of Typical U.S. Consumers Will be Using 100 Mbps by About 2020, Really

Wireless, either mobile or fixed, seems an inevitable solution for providing broadband access in rural areas, everywhere in the world.

Wireless, either mobile or fixed, seems an inevitable solution for providing broadband access in rural areas, everywhere in the world.

Over time, the solution choices are likely to shift, if one assume gigabit access really is the future.

In the meantime, to about 2020 or 2025, the issue really will be getting to a fairly widespread 100 Mbps.

About 10 percent will be buying 50 Mbps connections.

Nearly 24 percent will still be buying 24 Mbps service.

That might seem a crazy amount of bandwidth for “many typical users,” but standard technology forecasting techniques have, for more than a decade, actually suggested that would happen.

In 2001, for example, Technology Futures predicted that by year-end 2004, over 25 percent of U.S. households will have adopted broadband services, up from about five percent at the end of 2000. The actual U.S. broadband penetration rate was 30 percent, according to the Pew Internet and American Life Project.

“By 2010, we expect that the percentage will exceed 60 percent,” Technology Futures predicted in 2001. The actual penetration wound up being 66 percent.

“Our forecasts indicate that 1.5 Mbps will meet the typical user's expectations until about 2005, that 6 Mbps will do so until about 2010, then 24 Mbps until 2015, and finally 100 Mbps thereafter,” Technology Futures said in 2001.

“Our forecasts indicate that 1.5 Mbps will meet the typical user's expectations until about 2005, that 6 Mbps will do so until about 2010, then 24 Mbps until 2015, and finally 100 Mbps thereafter,” Technology Futures said in 2001.

There is at this point little reason to doubt that the forecast will continue to be substantially correct. Keep in mind that the 100 Mbps forecast by 2020 represents the “typical user’s” access speed, not the top “headline speed.”

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

PC Shipments Post the Steepest Decline Ever

PC shipments dropped the most in history (or at least since 1994, when IDC began tracking PC shipments) in the first quarter of 2013, according to IDC. That will surprise virtually nobody, given the clear shift of consumer demand to tablets.

Worldwide PC shipments totaled 76.3 million units in the first quarter of 2013, down 14 percent compared to the same quarter in 2012 and worse than the forecast decline of 7.7 percent, according to IDC.

Worldwide PC shipments totaled 76.3 million units in the first quarter of 2013, down 14 percent compared to the same quarter in 2012 and worse than the forecast decline of 7.7 percent, according to IDC.

The results also marked the fourth consecutive quarter of year-over-year shipment declines.

"Fading Mini Notebook shipments have taken a big chunk out of the low-end market while tablets and smartphones continue to divert consumer spending," IDC says.

"At this point, unfortunately, it seems clear that the Windows 8 launch not only failed to provide a positive boost to the PC market, but appears to have slowed the market," said Bob O'Donnell, IDC Program Vice President, Clients and Displays.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...