There’s an inherent tension between promotion of competition and the normal and expected working of any market.

There’s an inherent tension between promotion of competition and the normal and expected working of any market. In fact, one might well argue that market concentration is the inevitable result of consumers making choices. In other words, people buy the products and services they consider better.

That inevitably means the less-preferred providers go out of business or are bought by the more-successful suppliers.

That leads to market concentration, and at some point, a reduction of competition and the benefits competition normally brings.

That sooner or later leads to regulatory action to break up successful firms and reignite competition, whereupon the cycle starts again. Telecommunications is the sort of industry, though, that causes issues.

It is a capital-intensive business, and like most capital-intensive businesses, has high barriers to entry. That means, under even the best of circumstances, that there will be relatively few suppliers in a market, because the market simply cannot support more than a handful.

The issue is “how many” firms it takes to sustain reasonable levels of competition. In France, the minimum number of suppliers in the mobile market is deemed to be four.

In other markets, the number might be three. It is probably unlikely that the number two will be viewed as so reasonable.

So consolidation in Canada, the United States, France or anywhere else is pretty much just part of the normal dynamics of any competitive market. But it isn't so clear just how much consolidation regulators will permit.

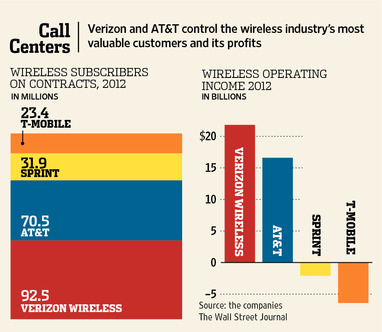

The biggest question is whether U.S. regulators would allow Sprint and T-Mobile USA to merge, a possibility executives of both companies have talked about. The Department of Justice seems to be signaling that it would not allow such a merger.

Some think such a merger would not be approved, based