Vodafone is the world’s second-largest mobile service provider or perhaps the seventh largest, as measured by revenue. In its past year ending in March 2013, Vodafone revenue fell 4.2 percent to £44.4 billion.

The shortfall was caused principally by economic conditions in Europe and new EC rules on wholesale termination revenue, both of which are hitting revenues in European markets.

But there is a broader trend at work. In developed markets, revenue drivers continue to evolve.

Before 2000, global telecom revenue growth was driven by voice revenues. After 2000, as voice declined, total revenue was sustained by growth of mobile service revenues, driven by voice, and then supplemented by text messaging revenue.

So mobile service revenues became the growth driver for the global business, which also expanded to include the formerly separate video entertainment business.

In many markets, though, mobile voice revenue now is flagging, as are text messaging revenues. In the business as a whole, growth rates of mobile revenue have been dropping since 2007, while average mobile revenue per subscriber has been under pressure as well, as first voice usage and now text messaging usage has begun a decline.

The obvious next growth driver is mobile data, which grew about 14 percent. But Vodafone’s revenue issues show that is not an easy or foolproof process. Mobile data revenue is growing, to be sure.

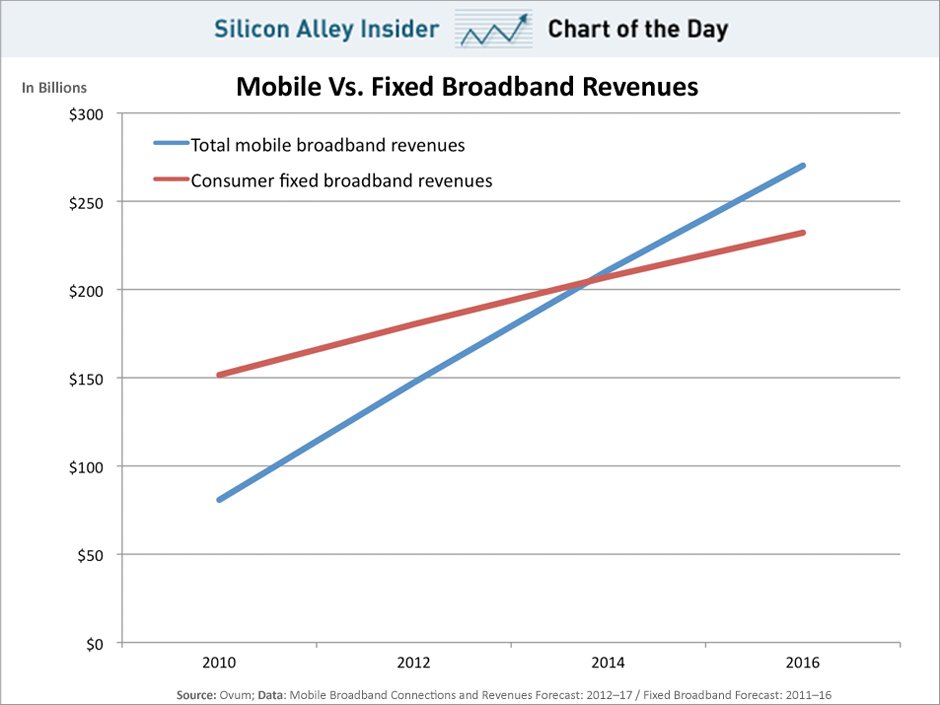

In 2014, telecommunications companies will make more money from mobile broadband than from fixed broadband for the first time.

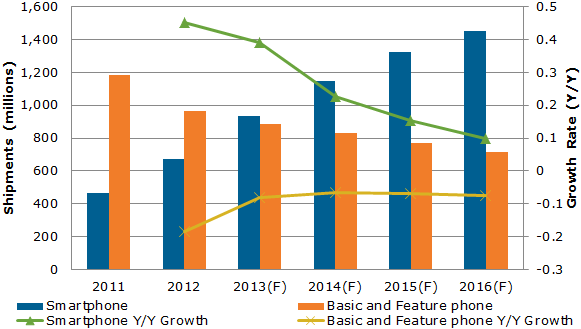

But nothing remains the same in the communications business, these days. At some point, as smart phones displace most use of feature or basic phones, and as most consumers therefore start buying mobile data plans, mobile data will itself become a legacy revenue source.

So the big question is “what comes next?” For most service providers, machine-to-machine services are part of the answer. Bigger mobile data plans, generating more revenue, are part of the answer as well. For some, mobile applications will be part of the creation of new revenue sources. Mobile payments, mobile banking and mobile commerce likewise are among the potential new sources of revenue.

So the big question is “what comes next?” For most service providers, machine-to-machine services are part of the answer. Bigger mobile data plans, generating more revenue, are part of the answer as well. For some, mobile applications will be part of the creation of new revenue sources. Mobile payments, mobile banking and mobile commerce likewise are among the potential new sources of revenue.

The point is that the next big transition for the mobile industry will come rather soon. And that transition will entail the maturation of the mobile data revenue “growth” story and its eventual replacement by a next wave of revenue drivers.

Much will hinge on how fast those new sources can be developed and scale.