Mobile connections for tablets might be developing as the first new revenue-generating "new app" of any significance for Long Term Evolution networks. In fact, the magnitude of those new revenue streams seems to be occurring faster than has been operator experience with third generation networks.

Mobile service providers, since at least the advent of third generation networks, have hoped for and touted the development of new revenue-generating applications, every time a next generation network is introduced.

That sometimes can take a while to develop. In fact, that has lead some observers to say there is no "killer app" for fourth-generation mobile networks, in the sense of some huge new revenue-generating application or feature.

That sometimes can take a while to develop. In fact, that has lead some observers to say there is no "killer app" for fourth-generation mobile networks, in the sense of some huge new revenue-generating application or feature.

In fact, in the near term, it might be logical to assume that “faster speed” is the closest thing to a new “killer app” that drives incremental revenue.

But one potentially new trend already might be developing for fourth generation Long Term Evolution networks, namely the additional connections to support tablet devices, and not necessarily new apps for smart phone users.

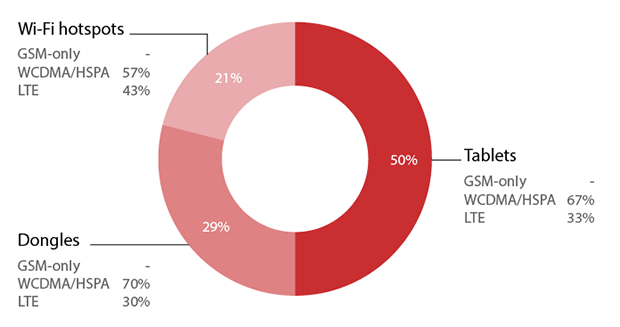

According to a survey sponsored by the GSM Association, about 33 percent of dongles, tablets or hotspots are 4G-enabled. That doesn’t mean all or even most of those devices are actively using 4G connections, but many do connect to the 4G network.

So some would argue that the first new 4G revenue source is network connections for tablets, which appear to offer a greater prospect for 4G growth than other data devices such as the traditional dongles.

On average, 4G operators surveyed by GSMA offered seven tablets in their data devices portfolio. Operators such as A1 Telekom (Austria), Polkomtel (Poland), MTS (Russia), STC (Saudi Arabia) and Telenor (Sweden) offered twice the number of tablets they were a year ago.

Australia’s Telstra, which launched its first 4G networks in the third quarter of 2011, recently noted a “really big swing in terms of tablet technology”. But tablets represented 24 percent of the operators’ mobile broadband customer base in the second half of 2012.

The introduction of shared data plans in developed markets, which allow, s users to attach several devices to a single plan and data allowance, is accelerating adoption of data devices.

Verizon Wireless CFO Francis Shammo says new customers often buy low end service plans, but then over a period of six months almost double the amount of devices that they put onto shared access plans.

Those additional shared data plans are boosting revenue per account. Even though many tablet users rely on WiFi as their main Internet connection, 4G LTE adn shared data plans will boost growth in broadband tablet data subscriptions, says Strategy Analytics.

Strategy Analytics forecasts global mobile broadband subscriptions on tablets will grow 800 percent from 2012 to 2017, as more than 165 million new tablets get connected to mobile networks.

But it would be odd, perhaps almost unprecedented, for 4G mobile networks to succeed wildly, which is what virtually everybody expects, without the emergence of some new qualitatively different experience or value driver.

It might be more important to say that "nobody knows" what such qualitatively-new experiences will emerge. But some might say it is unlikely 4G will remain "3G but faster."

About a decade ago, when the first commercial 3G networks were introduced, there was much talk about innovation and new applications the networks would enable, and the list looked remarkably similar to what people claim will happen with 4G.

E-commerce apps, for example, were thought to be an important 3G innovation. That is claimed for 4G as well, with more conviction, perhaps. “The availability of 3G services is going to have a profound effect on electronic commerce,” it was said.

That also is said of 4G. It was said that “3G works better” than 2G, and that was true. It also is said of 4G, and also is true.

3G wireless was sometimes characterized as a wireless version of the Internet, encompassing Web browsing, e-mail and media downloads. That sounds like 4G as well.

Over time, though, a distinctive lead application does tend to develop, though it might take some time. Voice and texting were the lead apps for 2G, while Internet access and email have emerged as the "killer app" for 3G, it can be argued.

For 3G networks, smart phones finally drove significant consumer uptake for broadband data. But it took quite some time for that new driver to be discovered and popularized.

To be sure, there is a line of thinking that the value of 4G might initially accrue in large part from significantly-lower the cost per-bit costs to provide mobile broadband. Verizon Wireless, for example, believes the cost to deliver a megabyte of data on 4G with LTE will be half to a third of the costs of a 3G network.

It now appears that tablets could be the device, and mobile network access the application, that first drives incremental new revenue for LTE networks.

Device type prevalence % in selected LTE operators' data device portfolios (Feb 2013)

Source: Wireless Intelligence