"One of the things we’ve seen from all our data crunching is that G.P.A.’s are worthless as a criteria for hiring, and test scores are worthless — no correlation at all except for brand-new college grads, where there’s a slight correlation," says Laszlo Bock, senior vice president of people operations at Google.

Google doesn't ask for transcipts, test scores or GPA, unless a candidate is straight out of school and hasn't worked anywhere else. "We found that they don’t predict anything," Bock says.

In fact, some teams at Google have about 14 percent of associates who never have gone to college.

Anecdotes such as this are a reason some believe a big disruption of higher education both is coming, and is needed. People might be essentially wasting money and time in hopes of getting a job, when the experience does not predict success at work.

Thursday, June 20, 2013

You Might Question the Value of a College Education: Google Now Does

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Clearwire Board Now Recommends Sprint Buyout Offer

Sprint has raised its buyout offer for Clearwire Corp to $5 per share, causing the board to reverse course again, and recommend that shareholders accept the Sprint offer, after previously recommending support for the Dish Network offer of $4.40 a share.

Sprint has raised its buyout offer for Clearwire Corp to $5 per share, causing the board to reverse course again, and recommend that shareholders accept the Sprint offer, after previously recommending support for the Dish Network offer of $4.40 a share. In addition to reversing course again, Clearwire also postponed a June 24 shareholder vote until July 8, meaning there is yet more time for more developments in the see-saw battle between Sprint and Dish Network for control of Clearwire and its spectrum.

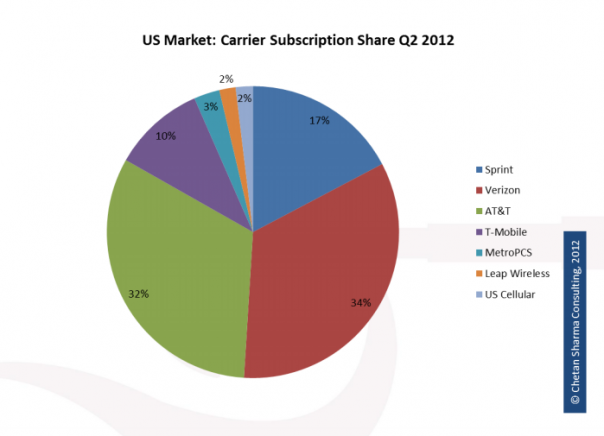

As fixated as investors might be on the outcome both of the SoftBank and Clearwire acquisition efforts, some might say it is time for the deals to be finalized, so the eventual victors can try and gain some traction in a U.S. mobile market that Verizon and AT&T simply dominate.

And there are precious few new accounts to be activated in the U.S. market. In the first quarter of 2013, 1.1 million net new mobile connections were activated, a decline of 60 percent, year over year. But most of those net additions were of the prepaid variety.

U.S. operators added 200,000 postpaid subs and 1.2 million total net new subscribers. Verizon got 720,000 of the net adds. AT&T got 291,000 and T-Mobile added 5,000.

So between them, Verizon and AT&T accounted for 86 percent of the net adds.

On top of that, Verizon and AT&T have at least 66 percent share of the U.S. mobile market, by customers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Data Revenues Might Hit 50% of Total in 2013

Data revenues now represent nearly 45 percent of U.S. mobile industry service revenues and the 50-percent level might happen in 2013.

After that point, data will represent the majority of U.S. service provider revenue, for the first time, according to projections by analyst Chetan Sharma.

The U.S. mobile data market grew 14 percent year-over-year to reach $21 billion in mobile data revenues, according to Sharma.

In 2013, U.S. mobile service providers will earn $90 billion in mobile data service revenues. Verizon and AT&T between them represent 70 percent of the mobile data services revenue and 66 percent of the customer base.

The data also illustrates how the maturing market now will be lead by changes in revenues per account, as the number of new human accounts (not machine to machine connections) that can be added is dwindling.

In the first quarter of 2013, 1.1 million new connections were activated, a decline of 60 percent, year over year, Sharma says. But most of those net additions were of the prepaid variety.

U.S. operators added 200,000 postpaid subs and 1.2 million total net new subscribers. Verizon got 720,000 of the net adds. AT&T got 291,000 and T-Mobile added 5,000.

So between them, Verizon and AT&T accounted for 86 percent of the net adds.

Though overall average revenue per user increased 35 cents, voice ARPU declined by 42 cents. Average data ARPU grew by 87 cents, sequentially.

Smart phones represented about 85 percent of the devices sold in the first quarter of 2013.

And it never is too soon for service providers to get ready for the next wave of growth after mobile data.

The next wave of growth might be significantly more challenging, though, as it might involve creating new lines of business beyond today’s voice, messaging, Internet access framework, and involve multiple lines of business such as cloud computing, commerce, payments, connected home or connected automobile, identity management and analytics that each will face serious competitors.

Beyond that, each of the new businesses are vertical rather than horizontal, meaning each new opportunity is a niche, compared to the universal “voice, data, messaging” appeal of basic mobility.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Investing in Dumb Pipe Not so "Dumb"

Telco executives sometimes appear to be “conflicted” about their core revenue strategies.

Many decry “dumb pipe” access revenues, even though those dumb pipe access revenues now provide the growth engine for fixed line telco, cable TV and mobile service providers alike.

Others say service providers will be able to overcome that “dumb pipe” issue by creating new content or application or enabling businesses.

Some say “over the top messaging” is a revenue opportunity; others say it will destroy most of the revenue now earned by text messaging services. In part, that is because many users seem to prefer OTT messaging to text messaging.

Half of US users claimed they prefer OTT messaging services over text messaging, a study by Acision suggests. “Speed” was viewed as an advantage, but also “rich features,” such as the ability to see when a message is delivered, and reliability.

In the United Kingdom, speed likewise was said to be a top reason users preferred OTT messaging over text messaging. In the U.K. market, cost also was a key value, presumably because fewer U.K. users have unlimited domestic texting plans.

Granted, both types of statements will be true for some suppliers, in some roles, in some markets, to some degree. In a service provider’s core markets, over the top messaging might be a revenue threat. Outside a service provider’s area of service, OTT messaging or apps could well be a net revenue generator.

But some might say that, for the most part, more significant revenue results will be obtained by improving the value provided by dumb pipe access, compared to all the new initiatives.

Part of the reason is that small changes to existing services can generate vastly more revenue than brand new business ventures.

Consider a “small change” to post paid customer bills. AT&T mobile customers on postpaid accounts will be paying a new 61 cent a month “administration fee” that will raise $512 million a year in revenue ($7.32 per year per post paid customer), on a base of roughly 70 million customers.

That might seem a "small" thing, and in one sense it is. But it another sense it is a big deal. The amount of money AT&T makes from that 61-cent charge will be roughly equal, every month, to the amount of gross revenue Verizon Communications fixed network operations makes from all small business customer operations every month.

That is a practical example of the ways large telcos most easily can create new $1 billion annual revenue streams, namely by creating small revenue enhancements to products most of their customers already buy.

Generating $1 a month in incremental revenue from 70 million customers creates $840 million a year in incremental revenue.

By way of comparison there probably are very few “new lines of business” initiatives launched by telcos that have reached that level, if any have done so.

In the messaging business, mobile service providers might well make more money by changing the way they package text messaging, than by investing in new OTT services of their own.

Mobile service provider text messaging revenue will decline on average by around 40 percent across Europe and the Middle East, many telco executives seem to believe. Mobile voice isn't that far behind, with a 20 percent decline foreseen, STL Partners predicts.

As a practical matter, it will be hard to create brand-new revenue streams that equal in magnitude the loss of 40 percent of SMS revenue, or 20 percent of voice revenue. Some might argue retail packaging (making unlimited domestic texting part of a basic connection fee) will have more revenue impact than most new lines of business.

That has implications for investment. Telstra Global Managing Director Martijn Blanken says telcos face "a fine balancing act," when it comes to plowing cash into their networks without having a clear view on what the return on that investment will be.

In other words, there not only still is money to be made in plain old connectivity, and big returns might come from ways to enhance those services, or at least package them in ways that retain significant revenue, if not as much as had been the case in past years.

"You don't want to over-invest," Blanken warns. But that's the issue: what balance of investment in core products and new lines of business.

For large telcos making capital investments, the "80/20" rule holds, a study suggests. Some 80 percent of the attention goes to decisions that produce less than 20 percent of operating results.

For large telcos making capital investments, the "80/20" rule holds, a study suggests. Some 80 percent of the attention goes to decisions that produce less than 20 percent of operating results.

Conversely, decisions that drive 80 percent to 90 percent of operating results tend to get 10 percent to 20 percent of attention, when capital investment choices are to be made.

Firms that earn more from their capex expenditures typically have proposals justified on the basis of improving performance metrics from existing services or territories, a PwC study has found.

Most of the telecoms executives in the survey distinguish between ‘business-as-usual’ capex and ‘project’ capex (also known as ‘innovation’ or ‘growth’ capex).

But though project capex typically represents just 20 percent to 30 percent of an operator’s total capex, it receives 80 percent to 90 percent of the capex committee’s attention. That is not to say innovation and revenue growth is unimportant. It is to note that capital allocation is failing to pay attention to the 20 percent of decisions that drive at least 80 percent of the financial impact (the “80/20 rule”).

That might seem to run counter to the notion that tier-one telcos must find new revenue sources. It isn’t. It means that the emphasis for capital investment has to be related to actual impact on revenue generation.

The logic is simple enough. A $5 a month swing in revenue has huge impact when the revenue-generating units involved number in the scores of millions, compared to a $5 a month revenue swing on a revenue-generating service involving a hundred thousand units.

In other words, $5 a month incremental revenue on a base of 30 million units generates $150 million a month, or $1.8 billion a year. A $5 a month incremental increase in revenue on a service with 100,000 units generates $500,000 a month, or $6 million a year.

PwC analysed the financial performance of 78 fixed-line, mobile and cable telecoms operators around the world and then surveyed 22 senior telecoms executives from a representative cross-section of companies in terms of size, services, location and financial performance.

of money on new infrastructure, but it’s not optimizing financial returns. PwC claims “most

telecoms executives admit as much.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, June 19, 2013

Backhaul Still a Major Issue in Sub-Saharan Africa

Strategists in urban and other relatively-dense areas in developed markets typically do not worry excessively about wide area backhaul services. That generally is not the case for ISPs or mobile service providers working in rural and thinly-populated areas.

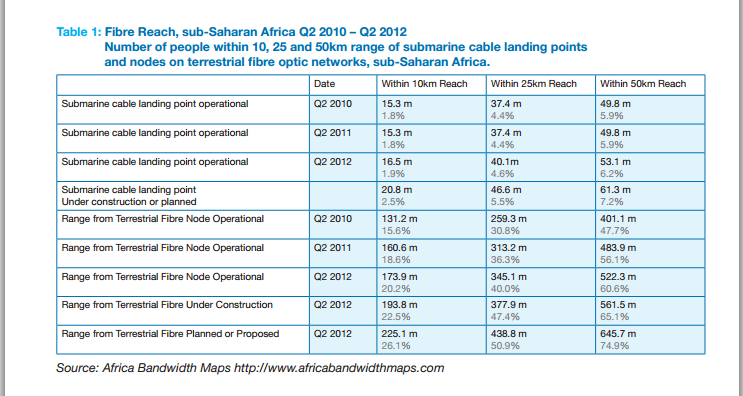

In June 2012, some 341 million people in sub-Saharan Africa lived beyond a 50-kilometer range of a terrestrial fiber optic backhaul network. What that could mean is a huge need for middle-mile connectivity provided by wireless networks, one might argue, since 50 km is a feasible distance for some microwave systems, assuming terrain is favorable.

The average price of a broadband connection represents just 1.5 percent of monthly income in Europe, but can represent over 100 percent to several thousand percent of monthly income for some African countries.

This level of affordability varies tremendously across sub-Saharan Africa, with the cost

of broadband access ranging from 5.7 percent of Gross National Income (GNI) per capita in South Africa, to 59.9 percent in Kenya, 259 percent in Madagascar, 1,070.8 percent in Ethiopia and 2,595 percent in Guinea Conakry, according to the International Telecommunications Union.

And there is no question but that new sources of wide area Internet access are having an impact on costs. In those countries recently connected to submarine cables, broadband has become much more affordable and the growth in broadband subscribers has accelerated.

Following the entry into service of the SEACOM and EASSy submarine cables in Kenya, for example, the price of fixed broadband decreased from 261 percent of GNI per capita in 2008 to 60 percent in 2010, in Mozambique from 312 percent in 2008 to 60 percent in 2010, and in Tanzania from 174 percent in 2008 to 50 percent in 2010.

These include Uganda (through Kenya) where the price of fixed broadband decreased from 375 percent of GNI per capita in 2008 to 36 percent in 2010, Ethiopia (via Sudan and Djibouti) from 2,721 percent in 2008 to 1,071 percent in 2010, and Burkina Faso (through Senegal, Cote d’Ivoire, and Benin) which decreased from 4,466 percent of GNI per capita in 2008 to 194 percent in 2010.

In Guinea Conakry, one of the eight countries that is wholly dependent on satellites, the monthly price of fixed broadband usage has decreased slightly to 2,595 percent of

GNI per capita in 2010 compared to 2,824 percent in 2008.

Growing availability of optical connections has reduced, but hardly eliminated, the need for satellite backhaul.

The supply of international trunk Internet bandwidth supplied by satellite to the sub-Saharan region reached a peak of around 9 Gbps in 2008, but has dropped back since then.

Kenya, for example, peaked at about 2 Gbps of international bandwidth supplied entirely by satellite in July 2009 until the entry of the SEACOM (2009), followed by the TEAMS (2009), EASSy (2010) and LION2 (2012) submarine cables.

That has dramatically increased the supply and decreased the cost of international bandwidth. Within two and half years, Kenya’s international bandwidth had increased from 2 Gbps to 53 Gbps by December 2011, but the amount supplied by satellite had shrunk to 108 Mbps, according to the Commonwealth Telecommunications Organization.

In June 2012, eight African countries remained 100 percent dependent on satellite for their international connectivity. Even in those countries with national fiber backbones, another 298 million or so people lived beyond the reach of terrestrial fiber networks, according to the Commonwealth Telecommunications Organization.

Most of Africa’s main urban hubs are now reached by fiber transmission backbones connected to submarine cable landing points, however.

In June 2012 a total of 40.1 million people lived within a 25 km range of a submarine cable landing point, but 345.1 million people lived within a 25 km range of a terrestrial fiber optic node.

By the time new networks enter service in 2013 to 2014, about 377.9 million people will live with a 25 kilometer range of an optical access point. Over the next three to five years, that range will increase to 438.8 million.

That still will leave 423.2 million people, or 49.1 percent of the population, beyond a 25-km reach of a terrestrial fiber optic node.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

What Balance of Licensed, Shared, Unlicensed Spectrum is "Best?"

It isn’t surprising that mobile service providers argue in favor of licensed spectrum as a principal way of dealing with spectrum and bandwidth needs in the wireless business. It isn’t surprising that would-be attackers often argue in favor of unlicensed spectrum.

Dedicated, licensed mobile broadband spectrum tends to create more-concentrated markets where license holders are few in number (normally three to five facilities-based operators in a country). That tends also to favor larger, well-capitalized service providers.

Unlicensed spectrum tends to appeal to smaller and entrepreneurial firms without the means to pay millions to hundreds of millions for spectrum, and tends to create a larger number of competitors.

In other words, licensed spectrum tends to favor larger incumbents, while non-licensed spectrum tends to favor smaller, upstart providers and innovators.

On the other hand, one might also argue that licensed spectrum tends to make technology transitions much easier, while non-licensed spectrum tends not to promote big changes so easily, since the wide range of non-licensed devices and providers makes any coordinated changes more difficult.

So licensed spectrum arguably is more amenable to “re-purposing” spectrum to new and better uses, compared to non-licensed spectrum.

Ericsson argues that licensed spectrum also promotes global roaming and allows for economies of scale. Also, non-licensed spectrum can lead to such interference that many of the advantages of the spectrum are not always optimized.

“Licensed but shared” spectrum is a newer concept that might arguably combine some of the better elements of each approach.

Ericsson perhaps logically argues for a primary reliance on licensed spectrum, with unlicensed and shared access as complements.

“Increasing the use of unlicensed spectrum as an independent main track is not an effective or sufficient approach for mobile communications,” Ericsson says.

The issue, of course, is in the details of how much shared access and unlicensed spectrum is made available. New competitors and smaller firms logically will argue for more reliance on unlicensed and shared approaches, there being little to no possibility regulators globally will suddenly adopt a new preference for unlicensed approaches.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Developed Asia-Pacific Telecom Markets Will Shrink Between 2012 and 2017

Aggregate statistics do not tell us very much about the health of various markets and product segments. Consider revenue projections for the Asia-Pacific region, generally acknowledged to be the fastest-growing region globally, with some estimates pegging revenue growth at about seven percent a year.

But telecom retail revenue in developed Asia–Pacific markets, for example, is set to decline at a compound annual growth rate of –0.4 percent during the next five years, according to new research by Analysys Mason.

Overall revenue is expected to fall from US$217 billion in 2012 to US$213 billion in 2017, even as gross domestic product grows three percent during this period.

As you might guess, the revenue decline will be driven by a fall in fixed revenue from US$86 billion in 2012 to US$74 billion in 2017.

The mobile sector will grow at around 1.5 per year from US$131 billion in 2012 to US$139 billion in 2017.

Fixed voice connections will decline by five percent between 2012 and 2017, from 138 million at the end of 2012 to 132 million at the end of 2017.

Mobile network connections will increase by 21 percent, from 255 million to 267 million in the same period, but mobile retail revenue will decline because the average revenue per voice minute will decrease – drastically in some countries.

“It is becoming increasingly difficult to extract the value of a mobile minute in developed economies,” says Tom Mowat, Analysys Mason principal analyst.

Still, mobile penetration will grow from 115 percent at the end of 2012 to 133 percent by the end of 2017.

Smart phones represented 42 percent of handset subscriber information modules at the end of 2012 and will grow to 84 percent by 2017.

By the end of 2013, smartphone SIMs in the region will outnumber those of non-smartphones.

The number of fixed broadband subscribers will grow from 75 million at the end of 2012 to 81 million by the end of 2017.

The proportion of fiber-to-the-home and business connections will grow from 42 percent of the region’s fixed broadband connections at the end of 2012 to 48 percent at the end of 2017.

The most rapid growth will be in Australia and Singapore, where national broadband projects could life penetration from about one percent up to perhaps 13 percent in Australia and 46 percent in Singapore by the end of 2017.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...