Orange is launching mobile payment services in partnership with Visa that will extend the range of operations for Orange Money beyond “mobile payments.” Though it is premature to speculate on just how far Orange will move into the banking business, Orange Money now will be issuing its own branded prepaid cards.

Orange is launching mobile payment services in partnership with Visa that will extend the range of operations for Orange Money beyond “mobile payments.” Though it is premature to speculate on just how far Orange will move into the banking business, Orange Money now will be issuing its own branded prepaid cards.

Whether most mobile service providers eventually will become “banks,” at least to some degree, is one question the initiatives raise.

Rogers in Canada already is certified as a bank by Canadian regulators, though it still appears Rogers is most interested in offering branded credit card services, not undertaking broader banking operations.

That is a traditional banking function, as is the processing of money exchanges between people and institutions.

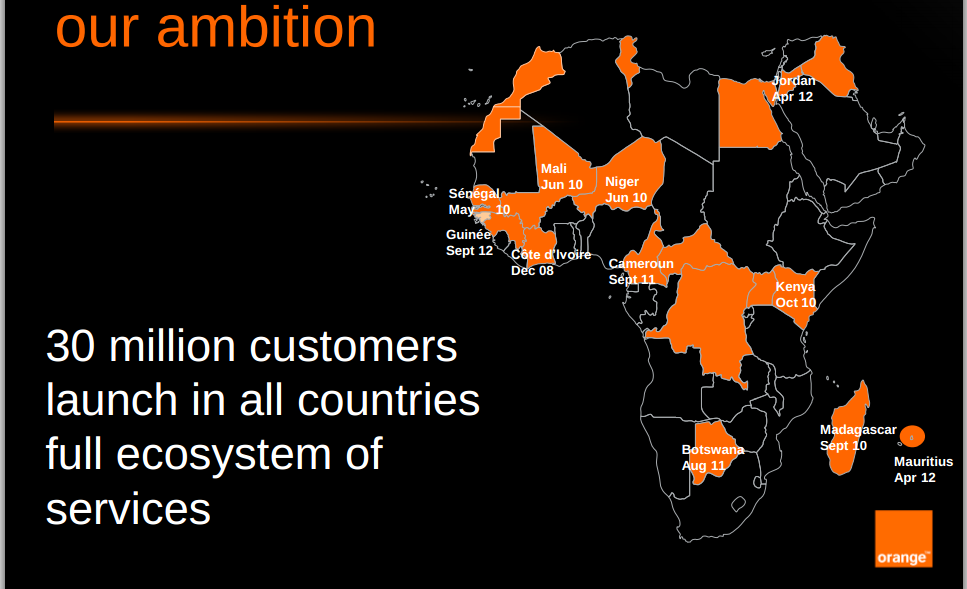

Botswana is slated to be the first country to get the new point-of-sale, online and ATM transaction options, in addition to the existing ability to use mobile phones to send and receive money and pay bills.

Starting in August 2013, though, Orange Money subscribers in Botswana will be able to use their Orange Money account to make Visa enabled payments and pay invoices at stores, international online merchants and at over 300 Visa ATMs across the country.

That moves Orange Money into the retail payments business in a new way.

Is "mobile banking" a key revenue opportunity for mobile service providers, or not? The answer is that "it depends" on what you mean by "mobile banking,” where those operations are conducted and how the business evolves.

According to a survey by ACI Worldwide, 76 percent of Indian mobile respondents used their mobiles for mobile banking in last six months (in 2012).

Comparatively, only 38 percent of respondents from the United States, and 31 percent from the United Kingdom said they had used mobile banking in last six months.

Obviously, money transfers are a bigger opportunity in regions where retail banking services are relatively rare, and less an opportunity where banking infrastructure is highly developed.

China, came in after India with 70 percent of users using mobile banking followed by South Africa (61 percent). The global average for Mobile Banking adoption rate stands at 35 percent of mobile users.

Where both online banking using PCs, and branch bank infrastructure are highly developed, people tend to use mobile banking to check balances or move money between accounts.

In regions where the banking infrastructure is undeveloped, and availability of PCs and Internet access is limited, people more often use mobile banking as a way to move money from one person to another, or from person to organization (to pay a utility or school bill, for example).

As you would guess, the revenue opportunity for a "mobile banking" services supplier is greater, and more direct, in scenarios where peer to peer payments are involved. As people pay fees to Western Union to move money, so mobile banking in a P2P context represents per-transaction fees that are easy to measure.

That is not the case for "softer" mobile banking transactions conducted in regions where the banking infrastructure is highly developed. In Western Europe or North America, for example, mobile banking more often is used in place of an online session to check balances, rather than as a way to move money from person to person, or person to organization.

Subscribers will need to have an Orange Money prepaid Visa card that is linked to their existing Orange Money account. The card will enable use of those funds to make point-of-sale payments at retailers and withdraw cash at ATMs, as well as make web purchases.

Other countries in Africa and the Middle East, where Orange Money is already available, will eventually offer the Orange Money prepaid Visa card as well.

Safaricom’s M-Pesa already offers the same service through Safari Pre-Pay card offered in conjunction with I&M Bank.

The moves illustrate one of the potential ways mobile service providers or telcos might diversify their core operations to replace declining voice and messaging revenues.

Mobile payments, something AT&T, Verizon Wireless and T-Mobile US now are preparing to introduce as a nationwide commercial service, is another example.

Isis, the mobile wallet service owned by the three carriers, plans its national U.S. launch before the end of 2013.

It is some measure of the new services revenue challenge now facing communications service providers in the developed regions that mobile payment and mobile banking are serious initiatives.

But it is hard to see right now just how far matters could eventually progress. What is clear is that Orange considers mobile money and possibly other mobile banking opportunities serious indeed.

In the second quarter of 2013, U.S. mobile service providers added an aggregate net new 139,000 connections, down about 95 percent from the second quarter of 2012.

In the second quarter of 2013, U.S. mobile service providers added an aggregate net new 139,000 connections, down about 95 percent from the second quarter of 2012.