Baltimore is hiring a consultant that would help the city develop a plan for expanding Internet service provider options for businesses and residents. For the moment, the only expectation is a study that provides options, such as creating greater incentives for any would-be ISPs to create a facilities-based new network.

Presumably, the study also will explore options for anchoring such a new metro network with fiber Baltimore could lay to support its own internal operations, or other initiatives to lure a few anchor tenants that could build on such a network.

Baltimore was among cities that had bid to become a site for the first Google Fiber operation.

And Verizon has decided not to upgrade Baltimore with FiOS.

In all likelihood, Baltimore will find it must hope for some sort of public-private partnership to "spot build" new facilities in Baltimore, as so far, the financial return for a full citywide build appear quite daunting.

Thursday, August 15, 2013

Baltimore to Explore Own Internet Access Network

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

PCs are for Work, Other Than That, People Will Prefer Tablets, Smart Phones

Perhaps some executives in the PC industry actually believe they can build a PC that entices people to part with their smart phones or tablets. Some of us think that is a fool's errand.

Some might say devices such as the Chromebook are designed for affordable browsing. Some of us would not agree. Browsing is what people prefer to do on other devices, when they are not working and producing large amounts of content.

That probably has implications for the use of all the devices. A "work" device is not necessarily as "personal" a device as a smart phone, or as much fun as a tablet. Some devices (think of most devices in your kitchen or livingroom or bedroom) just have to work. You don't think about them too much. They aren't necessarily personal statements, as your clothing or jewelry or fragrance most likely are.

And that's the issue with PCs. There's no such thing anymore as "web-centric" users. That's everybody, doing everything.

When the PC was the only computing device, people might have been more attached to them. These days, the PC increasingly is something you use when you have to work. Most other things you'd prefer to do on a tablet or smart phone.

That likely has implications for how much people are willing to spend on a work appliance, if they are spending their own money.

Some might say devices such as the Chromebook are designed for affordable browsing. Some of us would not agree. Browsing is what people prefer to do on other devices, when they are not working and producing large amounts of content.

That probably has implications for the use of all the devices. A "work" device is not necessarily as "personal" a device as a smart phone, or as much fun as a tablet. Some devices (think of most devices in your kitchen or livingroom or bedroom) just have to work. You don't think about them too much. They aren't necessarily personal statements, as your clothing or jewelry or fragrance most likely are.

And that's the issue with PCs. There's no such thing anymore as "web-centric" users. That's everybody, doing everything.

When the PC was the only computing device, people might have been more attached to them. These days, the PC increasingly is something you use when you have to work. Most other things you'd prefer to do on a tablet or smart phone.

That likely has implications for how much people are willing to spend on a work appliance, if they are spending their own money.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Lenovo Sells More Smart Phones, Tablets than PCs

Lenovo says it is becoming a "PC Plus" company. In its most recent quarter, Lenovo ’s sales of smart phones and tablets surpassed PCs for the first time. During the first quarter, Lenovo became the world’s fourth largest smart phone supplier and recorded the fastest growth among the top five vendors, growing 132 percent.

In China, Lenovo is now the second largest smart phone company, the company says.

One might point to several elements of that story. The rise of computing devices other than PCs, the shift of technology supply in the direction of Chinese suppliers and a concomitant retail pricing pressure on existing suppliers are some of the themes one might point to.

Another apparently non-related item, namely Cisco's most recently quarterly report, points to another broad theme, namely a shift in global technology leadership from broadly diversified firms to specialists.

Nobody yet is suggesting Cisco is going the way of Nortel Networks, one of a handful of firms that once lead global telecom infrastructure sales by supplying a broad range of products, but went bankrupt.

Still, these days, being a supplier of lots of infrastructure products, with a coherent fit between thenm, is a much-tougher feat.

In today's market, most firms have found it much easier to focus on a segment: mobile, fixed network only, switches and routers, radios or optical transmission.

Sooner or later, Cisco might have to respond to critics who say it operates in too wide a range of businesses. And that will mean a smaller Cisco, one might argue.

In China, Lenovo is now the second largest smart phone company, the company says.

One might point to several elements of that story. The rise of computing devices other than PCs, the shift of technology supply in the direction of Chinese suppliers and a concomitant retail pricing pressure on existing suppliers are some of the themes one might point to.

Another apparently non-related item, namely Cisco's most recently quarterly report, points to another broad theme, namely a shift in global technology leadership from broadly diversified firms to specialists.

Nobody yet is suggesting Cisco is going the way of Nortel Networks, one of a handful of firms that once lead global telecom infrastructure sales by supplying a broad range of products, but went bankrupt.

Still, these days, being a supplier of lots of infrastructure products, with a coherent fit between thenm, is a much-tougher feat.

In today's market, most firms have found it much easier to focus on a segment: mobile, fixed network only, switches and routers, radios or optical transmission.

Sooner or later, Cisco might have to respond to critics who say it operates in too wide a range of businesses. And that will mean a smaller Cisco, one might argue.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, August 14, 2013

DoJ Opposition to US Airways, American Airlines Merger has Telecom Implications

The unexpected lawsuit by the Department of Justice to block the proposed US Airways merger with American Airlines reminds some of us of merger strategy in the U.S. telecommunications business.

In the past, when a merger wave is about to break out, it has been better to be the first such combination, not the last. The reason is that, for all the oversight issues, it has been easier to be the first to move, rather than the last to move.

After clearing a number of other similar transactions, DoJ now seems to have concluded that the merger wave has gone far enough. In 2008 DoJ had approved the merger of Delta and Northwest Airlines. In 2010 it approved the merger of United and Continental.

In terms of share of domestic seats sold in September 2013, Delta Air Lines has 22 percent, Southweset Airlines has 21 percent, United Airlines has 17 percent, US Airways has 12 percent while American Airlines has 13 percent.

Granted, the profit is in the overseas routes, but those earlier mergers, which dramatically reduced competition, seem to be bumping against an analogy to the "rule of four" that many telecom regulators apply to mobile competition.

And that rule is that four competitors are required. In the airline industry, it appears DoJ deems four to be insufficiently competitive.

In the past, when a merger wave is about to break out, it has been better to be the first such combination, not the last. The reason is that, for all the oversight issues, it has been easier to be the first to move, rather than the last to move.

After clearing a number of other similar transactions, DoJ now seems to have concluded that the merger wave has gone far enough. In 2008 DoJ had approved the merger of Delta and Northwest Airlines. In 2010 it approved the merger of United and Continental.

In terms of share of domestic seats sold in September 2013, Delta Air Lines has 22 percent, Southweset Airlines has 21 percent, United Airlines has 17 percent, US Airways has 12 percent while American Airlines has 13 percent.

Granted, the profit is in the overseas routes, but those earlier mergers, which dramatically reduced competition, seem to be bumping against an analogy to the "rule of four" that many telecom regulators apply to mobile competition.

And that rule is that four competitors are required. In the airline industry, it appears DoJ deems four to be insufficiently competitive.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

1 Regulator or 28? Competition or Investment? Are the Questions are Connected?

Should the European Union have only a single telecommunications regulator, or keep 28 national regulators? That appears to be a live question now that rival “proposals” are floating around the EU.

Neelie Kroes, the EU telecommunications commissioner, has proposed an arrangement that some would think is more policitically feasible, namely keeping the 28 national regulators in place, while nevertheless removing restrictions that hinder cross-border operation, cooperation and ultimately mergers.

However, in a document obtained by the Financial Times, Joaquín Almunia, EU antitrust executive, called for a more-radical plan of abolishing the separate national authorities and replacing them with a single EU telecommunications office.

Fair-minded observers might say each plan has merit. Many service provider executives might agree that a single, continent-wide market would be more efficient, easier to navigate, at less cost.

But observers might also say there will be much more political opposition to the one-regulator plan, than to plans to harmonize and liberalize cross-border operations, while keeping the national regulators in place.

So the Kroes plan might arguably have the advantage of faster implementation. It might be hard to envision national governments potentially giving up the revenues national spectrum auctions might raise, nor the ability to customize national universal service plans between their own urban and rural areas, for example.

On the other hand, policymakers still appear “conflicted.” They still seem to want to promote competition by maintaining low-cost wholesale access to dominant carrier networks.

On the other hand, policymakers also want those dominant carriers to make huge new investments in next generation networks that will subject to the same low-profit, competition-enhancing arrangements that make those investments risky to stupid.

It isn’t so obvious that one regulator or 28 cooperating authorities is necessarily the better plan. Simplicity is good. But so is speed of implementation. And both sets of proposals seem to have the same objective, namely rationalizing operating environments and paving the way for mergers and consolidations that will produce fewer, but stronger, providers.

Under any set of circumstances, service provider executives and policymakers might well agree that current scale of operations for most service providers is not optimal. They need to get bigger.

Most EU policymakers also must address the risk and high costs of building next generation fixed networks, without addressing investing firm ability to capture adequate financial returns.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

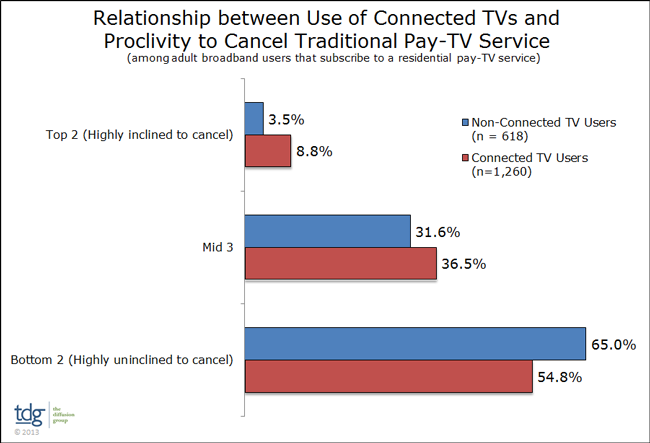

Nobody Knows What Will Happen to Service Provider Revenue Once Major Video Cord Cutting Happens, Really

Adult broadband users with an Internet-connected TV are twice as likely as those with non-net-connected TVs to be “highly inclined” to cancel their current subscription video service, according to a new report from The Diffusion Group (TDG Research).

Those findings likely would not come as a surprise to anybody who normally watches developments in the video entertainment business. It is a trusim that a person cannot become a user or customer of any product unless that person is physically able to purchase or use.

So it should not be a great surprise that when able to view Internet-delivered TV on a big screen TV, some users might decide they can do without a video subscription. Without the ability to view Internet-delivered video, a person has no option to consider whether that experience is a reasonably workable substitute for a video subscription.

To be sure, most people probably would simply augment what they already do, and add some Internet sourced TV to their broadcast TV or video subscription or other home video sources such as Blu-ray players.

But perhaps seven percent of consumers, at any given time, might be interested in abandoning their video subscriptions for some sort of over the top or broadcast TV alternative, TDG Research suggests.

Some 8.8 percent of connected TV users say they are highly inclined to cancel their current subscription TV service in the next six months, compared with only 3.5 percent of non-net-connected TV users, TDG Research says.

Virtually no executives whose firms are major providers of subscription video services would argue it makes no difference to their revenues were widespread abandonment of subscription TV to be replaced by widespread viewing of over the top alternatives.

On the other hand, assuming they are not forced to offer low-cost “unlimited” service where there is no matching of usage to retail price, watching more over the top television is going to create demand for orders of magnitude more bandwidth.

So yes, service providers will lost a big chunk of video revenue. But they will gain a big chunk of Internet access revenue. Or so the logic might suggest.

The stumbling block, and it is a serious problem, is a shift of rival major competitors to something like Google Fiber’s pricing and usage plans: unlimited usage of a 1 Gbps symmetrical Internet access service, for $70 a month.

That would wreck most tier-one service provider revenue models, in the event of a major drop in video subscriptions, and an equally big shift to over the top services using Internet delivery.

There is one more huge issue as well. In addition to spending more for Internet access, consumers will still be paying for the TV programs or channels they want. When all the costs are added up, it is not entirely clear that the total cost of ownership will be dramatically less than what they already pay.

The conventional wisdom is that cable companies and telcos will be savaged on the revenue front when a widespread shift to over the top delivery begins. That isn’t necessarily the case.

Much depends on consumer demand. Heavier video entertainment users might find it costs less to keep buying linear TV services. Moderate users might find net costs roughly the same. Lighter users, though, probably would be best positioned to achieve savings.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Smart Phones Surpass Basic Phone Sales for First Time Globally

Some trends are so long in coming that the actual event seems anticlimactic. That seems to be true for smart phone sales, which according to analysts at Gartner have surpassed sales of feature or basic phones for the first ever in the second quarter of 2013.

To be sure there will be a market for basic devices for quite some time. But, sooner or later, when nearly every device is “smart,” the term will have lost its meaning, and smart phones will simply be phones.

Global mobile phone sales to end users totaled 435 million units in the second quarter of 2013, an increase of 3.6 percent from the same period last year, according to Gartner, Inc.

Worldwide smart phone sales to end users reached 225 million units, up 46.5 percent from the second quarter of 2012.

Sales of feature phones to end users totaled 210 million units and declined 21 percent year-over-year.

Asia/Pacific, Latin America and Eastern Europe exhibited the highest smart phone growth rates of 74.1 percent, 55.7 percent and 31.6 percent respectively, as smart phone sales grew in all regions.

Samsung had the highest global market share of the smart phone market, at 31.7 percent, up from 29.7 percent in the second quarter of 2012.

Apple’s smart phone sales reached 32 million units in the second quarter of 2013, up 10.2 percent from the same quarter of 2012.

Worldwide Smartphone Sales to End Users by Vendor in 2Q13 (Thousands of Units)

Company

|

2Q13

Units

|

2Q13 Market Share (%)

|

2Q12

Units

|

2Q12 Market Share (%)

|

Samsung

|

71,380.9

|

31.7

|

45,603.8

|

29.7

|

Apple

|

31,899.7

|

14.2

|

28,935.0

|

18.8

|

LG Electronics

|

11,473.0

|

5.1

|

5,827.8

|

3.8

|

Lenovo

|

10,671.4

|

4.7

|

4,370.9

|

2.8

|

ZTE

|

9,687.6

|

4.3

|

6,331.4

|

4.1

|

Others

|

90,213.6

|

40.0

|

62,704.0

|

40.8

|

Total

|

225,326.2

|

100.0

|

153,772.9

|

100.0

|

Source: Gartner (August 2013)

The news that BlackBerry is exploring “strategic alternatives” (financial speak for “we are for sale”) can be interpreted in light of Gartner’s operating system market share figures as well.

In the smart phone operating system (OS) market, Microsoft took over BlackBerry for the first time, taking the third spot with 3.3 percent market share in the second quarter of 2013.

For a firm that once lead the smart phone market, that continued slippage is a clear sign that BlackBerry rapidly is losing the ability to succeed as an independent company.

Global Smart Phone Sales, by Operating System in 2Q13 (Thousands of Units)

Operating System

|

2Q13

Units

|

2Q13 Market Share (%)

|

2Q12

Units

|

2Q12 Market Share (%)

|

Android

|

177,898.2

|

79.0

|

98,664.0

|

64.2

|

iOS

|

31,899.7

|

14.2

|

28,935.0

|

18.8

|

Microsoft

|

7,407.6

|

3.3

|

4,039.1

|

2.6

|

BlackBerry

|

6,180.0

|

2.7

|

7,991.2

|

5.2

|

Bada

|

838.2

|

0.4

|

4,208.8

|

2.7

|

Symbian

|

630.8

|

0.3

|

9,071.5

|

5.9

|

Others

|

471.7

|

0.2

|

863.3

|

0.6

|

Total

|

225,326.2

|

100.0

|

153,772.9

|

100.0

|

Source: Gartner (August 2013)

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

When Was the Last Time 40% of all Humans Shared Something, Together?

I miss these sorts of huge global events where 40 percent of living humans share a chance to build something for others.

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

Financial analysts typically express concern when any firm’s customer base is too concentrated. Consider that, In 2024, CoreWeave’s top two ...