“What drives revenue after mobile Internet access?” is a question mobile service providers and telcos have been asking themselves, and working on, for some time. Of the myriad potential opportunities, machine-to-machine (M2M) revenue seems to be percolating to the top of every list of potential sizable medium-term revenue growth.

“What drives revenue after mobile Internet access?” is a question mobile service providers and telcos have been asking themselves, and working on, for some time. Of the myriad potential opportunities, machine-to-machine (M2M) revenue seems to be percolating to the top of every list of potential sizable medium-term revenue growth.

With the caveat that people differ on what M2M services and apps include (some prefer the term “Internet of Things,” which in some cases seems to include use of mobile networks by tablets; others tend to define M2M as sensor apps operating without a direct human end user actively involved), there is a good reason for the optimism.

The easiest path forward for any business is a simple line extension that builds off existing competencies. And use of mobile networks for sensor operations and applications simply builds off communications capabilities originally designed to connect people.

The number of cellular M2M connections will more than triple by the end of 2017, according to IHS, growing to 375 million in 2017, up from 116 million in 2012.

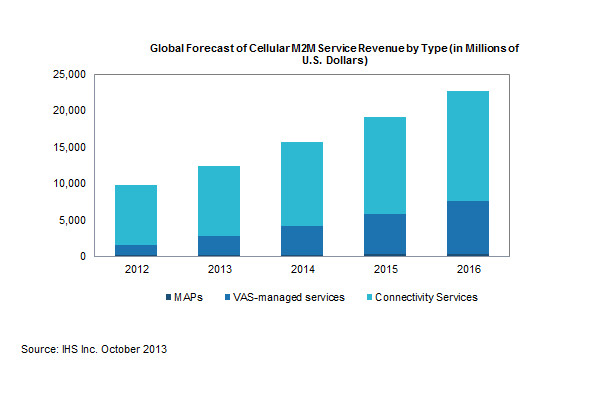

As a result, revenue generated by mobile M2M services will grow to $22.4 billion in 2016, up from $9.6 billion in 2012. Those are significant amounts, if you assume a tier-one carrier generally is interested in new revenue sources capable of driving at least $1 billion in new annual revenues.

Mobile service providers of course benefit from providing access services. But much of the M2M business involves a mix of horizontal (access, security) and vertical (line of business) industry segment expertise.

In many cases, that means service providers will partner with industry specialists with domain expertise in a particular industry vertical. Generally, mobile service providers also will be looking to create M2M platforms such partners can use.

Volume will be key for the new business. Consumer smart phone accounts might generate $80 a month revenue. Sensor connections will be a fraction of that amount, perhaps $5 a month.

Operating costs might also be a key operating cost input, since sensors, unlike smart phones, might need to be repaired or replaced in the field.

People tend to bring their failed devices to a retail store for repair or exchange, so there is no need for a truck roll.

And where phones get replaced every couple of years, on average, sensors might be in place for considerably longer periods of time, necessitating a longer-term view of device capabilities and end user business objectives.

Mistakes will be costly. So the emphasis will be on deploying network sensor elements that can be provisioned remotely, by the customer, and monitored remotely, using simple application programming interfaces.