What happens to the retail rates of lower-speed broadband access if the market standard winds up being a gigabit for $70 a month, or a gigabit for $80 a month, or perhaps less? At $80 per month, a gigabit service implies a per-gigabit price of eight cents per megabit.

So the retail price of a 5 Mbps service “should be” 40 cents per month, or, in other words, nearly at the level of Google Fiber’s “free for seven years” 5 Mbps access service.

The caveat is that lower speed services always cost more, per megabit of service speed, than higher speed services, on a cost per megabit basis.

Still, even with that caveat, experienced practitioners from the network access business quickly will say that a fixed network cannot be built, under conditions where Internet access is the financial underpinning, when per-user revenue is just 40 cents a month, even when other current and projected revenue sources are available.

So the hope, or expectation, would have to be that almost nobody wants Internet access service at 5 Mbps, making the demand for such service virtually nil.

If that is the case, and most people want to buy services closer to the $50 to $70 a month level, revenue per user is not the problem, especially when other services can be sold in significant quantities.

The business model problem then shifts to costs, both capital investment and operating cost.

In fact, based on current levels of revenue “per user” generated by the largest Internet app providers, it seems fairly obvious that the whole idea behind “free access for seven years” is that, within 10 years, nobody will want such a service.

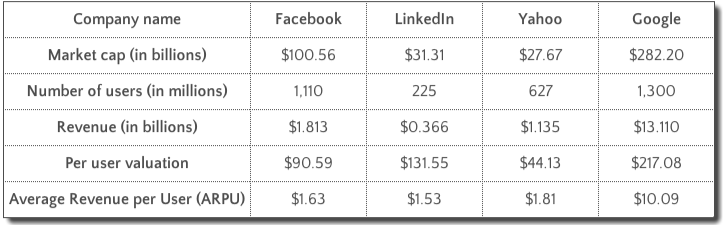

Some calculate that Facebook presently earns about $1.63 per user, per year, while Google earns $10.09 per user, per year.

At such levels, no rational ISP would expect to cover the cost of building gigabit networks based solely on advertising and other revenue generated by advertising and commerce transactions.

Still, the essential point is that if gigabit access, for $70 or $80 a month becomes anything close to a market-dictated reality, the cost of slow-speed Internet access (5 Mbps, at the moment, higher numbers in the future) might in fact be something very close to “free,” with ISPs expecting to earn higher revenues from sales of additional services of various types.

It might be reasonable to expect an ISP to charge for installation or use of required access equipment after the first outlet, as Google Fiber does. But the possibility remains that in a world where gigabit service is fairly standard, it might make sense to offer low-speed access essentially for free.

For starters, almost nobody would want such service. For the few that do, there likely will be other incremental revenue streams an ISP might be able to create, once that Internet connection is in place.