Jajah, one of the early over the top VoIP services, is shutting down on January 31, 2014. Founded in 2005, jajah was acquired in 2009 by Telefonica for $207 million, as part of a strategy to create a telco-owned over the top service.

But Telefonica has been pursuing other ways of using VoIP to pick up more users, namely with mobile apps like Tu Go. In essense, Tu Go now will do what jajah once was seen as doing.

Tuesday, December 3, 2013

It's not Easy to Run a Carrier-Owned Over the Top VoIP Service

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Monday, December 2, 2013

BlackBerry Says It Isn't Dead

BlackBerry says it is "very much alive," and that "reports of our death are greatly exaggerated," in an open letter by BlackBerry to enterprise customers.

It's an odd statement, in some ways, but seems to validate thinking in many quarters that BlackBerry will pin its future hopes on remaining an enterprise-oriented mobile communications services company, and not a consumer devices company.

It's an odd statement, in some ways, but seems to validate thinking in many quarters that BlackBerry will pin its future hopes on remaining an enterprise-oriented mobile communications services company, and not a consumer devices company.

Interim BlackBerry Ltd. chief executive John Chen issued the open letter in an apparent attempt to reassure enterprise customers about the firm's commitment to remain a viable provider of range of services for large organizations, including the managing and securing of multiple devices using the BlackBerry Enterprise Service.

In the letter, Mr. Chen says that some consumers are hearing from companies that sell MDM (mobile device management) software that BlackBerry’s BES (BlackBerry Enterprise Service) might not be supported, a typical competitive tactic in such cases.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Amazon Prime Air Will Need Approval from Federal Aviation Administration!

Still, the idea that Amazon might be able to use drones to deliver parcels (up to five pounds, at the moment) to locations within 10 miles of an Amazon warehouse would open up affordable, same-day delivery options for perhaps 80 percent of everything Amazon now sells.

IF the Federal Aviation Administration Administration approves, of course. Watch for a whale of opposition from place-based retailers.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Most Additional Mobile Spectrum Has to Come from Existing Licensees

Though better air interfaces, offloading, small cells and possibly retail pricing policies will help mobile service providers cope with growing mobile data demand, there actually is very little unused spectrum to allocate for additional mobile use.

That means reallocating existing spectrum is what has to happen, according to the Phoenix Center for Advanced Legal and Economic Policy Studies.

The U.S. federal government itself controls about half (1,687 MHz) of the spectrum

between 225 MHz and 3.7 GHz most useful for mobile or fixed communications.

And one problem is that government agencies do not have incentives to use spectrum efficiently.

“The PCAST Report, for example, states plainly, ‘Federal users currently have no incentives to improve the efficiency with which they use their own spectrum allocation.’”

The European Commission’s WIK-Consult Report notes that “public sector agencies may

not face sufficient incentives to make maximally economically efficient use of

their spectrum assignments (e.g. through sharing with other compatible uses), or

to give spectrum back to the spectrum management authority if they no longer need it.”

As we see it, it is the inefficiency of spectrum management, not spectrum use, which is most problematic, the Phoenix Center says. The fact that the Pentagon pays $750 for a hammer does not mean a consumer can’t purchase one for $10 at the local hardware store.

In contrast, if the government is an inefficient manager of spectrum, then the consequences of the inefficiency are realized across the entire spectrum ecosystem.

The issue then is one of creating a licensing regime that maximizes efficiency. The analysis suggests it is preferable for the Government to sell spectrum rather than lease it.

Where spectrum is shared, it likewise would be better for the management process to be conducted by the private market rather than a government entity.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Up to This Point, "New Services Revenue" Has Come from Legacy Sources

Despite the emphasis on creation of “new services” to drive the next waves of revenue growth in the local access business, the actual revenue gains so far have been driven mostly by market share shifts among mobile, fixed network telco, cable TV and satellite TV firms.

That is not to discount share shifts to independent providers of all sorts, including competitive local exchange carriers, independent ISPs and resellers. But most of the measurable volume of U.S. market share change occurs in just two segments: fixed network telco and cable TV.

You know the story: telcos are taking video market share, and ceding voice market share to cable TV. Cable TV companies are losing video share, but have gained voice services share.

Most would say cable companies retain an edge in high-speed Internet access.

In the business customer segment, fixed network telcos have been slowly losing share to cable TV operators, but also blunting inroads of the independent and competitive providers. The exception is a few independent fixed network telcos that have moved agressively into the small business services segment (Windstream and Frontier Communications being the salient examples).

Insight Research Corporation predicts U.S. cable companies in 2013 will reach $8.8 billion in annual revenues providing telecommunications services to small and medium-size businesses.

U.S. fixed network telcos probably have about $6 billion iin video subscription revenues, based on an attribution of video at $50 a month, on a base of about 10.4 million subscribers.

Next to mobility, business services are the second largest segment in the $500 billion U.S. telecommunications business.

According to Insight Research, cable companies already have about 10 percent of the business market for voice and data services. At $8.8 billion, the addressable market is $89 billion annually.

There is huge logic to the cable push. Most tier-one telcos consider small businessto be part of the “mass markets” operation. Given the historic consumer orientation of cable TV companies, selling voice and Internet to small businesses is not a huge shift.

Of course, cable operators also sell to enterprises, especially for high-capacity private networks and mobile backhaul connections.

In the future, cable operators probably also will get a share of the backhaul market for small cells.

The point is that, so far, the "new" revenue streams for cable TV operators and fixed network telcos have come from legacy services, albeit legacy revenues taken from existing providers.

At some point, that trend will run its course and "truly new" services (sensor connections for machine-to-machine or Internet of Things applications), automobile communications, home automation and other revenue sources will have to be created.

For some time to come, market share shifts will continue to drive the significant portion of service provider "new services" growth.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Cable, Telco, ISPs Generally Score Very Low on Customer Service: Why?

Many would not agree that it is simply a huge volume of customer interactions that causes most cable TV companies, fixed network telcos or ISPs to get very-low scores for customer service.

Comcast CEO Brian Roberts does. "What unfortunately happens is we have about … 350 million interactions with consumers a year, between phone calls and truck calls. It may be over 400 million and that doesn't count any online interactions which I think is over a billion. You get one-tenth of one-percent bad experience, that's a lot of people."

Others might think there are other impediments. Installs require that someone be home. That often means a person has to take time off from work to activate service. That is a real cost, bound to increase irritation.

To be sure, most service providers work at getting better, and most arguably have done so over the past decade. But the need to take time off work to initiate service is bound to be an irritant.

Install windows also have gotten measurably better, in some cases. Comcast now promises install windows of only two hours duration, where it once was standard for windows to be essentially four hours long (morning, 8 am to noon, or afternoon, noon to 4 pm).

Recurring service bills can be horrendous, hard to understand and complex. That probably doesn't help, as it causes customer service representative interactions, with the chance that a consumer will be kept waiting "on hold." Online chat helps. Email queries arguably do not help very much, as the latency of a response is too high.

Communications and entertainment monthly bills also are likely an issue. Consumers are reminded every month just how much their service costs, and many likely are irritated by the many above the line or below the line taxes, fees, assessments that are part of most bills in the communications and video entertainment business.

It is hard to measure, but consumers might express frustration with customer service because they already are dissatisfied with the value and price relationship of the underlying service.

ISPs get terrible reviews, for example, but the reasons might lie more with unhappiness about the service than the customer service.

Fixed network phone service customer satisfaction increased 5.7 percent to 74. The paradox is that since unhappy customers are abandoning fixed network voice service, the remaining customers are those who value the service more, leading to higher scores.

Comcast CEO Brian Roberts does. "What unfortunately happens is we have about … 350 million interactions with consumers a year, between phone calls and truck calls. It may be over 400 million and that doesn't count any online interactions which I think is over a billion. You get one-tenth of one-percent bad experience, that's a lot of people."

Others might think there are other impediments. Installs require that someone be home. That often means a person has to take time off from work to activate service. That is a real cost, bound to increase irritation.

To be sure, most service providers work at getting better, and most arguably have done so over the past decade. But the need to take time off work to initiate service is bound to be an irritant.

Install windows also have gotten measurably better, in some cases. Comcast now promises install windows of only two hours duration, where it once was standard for windows to be essentially four hours long (morning, 8 am to noon, or afternoon, noon to 4 pm).

Recurring service bills can be horrendous, hard to understand and complex. That probably doesn't help, as it causes customer service representative interactions, with the chance that a consumer will be kept waiting "on hold." Online chat helps. Email queries arguably do not help very much, as the latency of a response is too high.

Communications and entertainment monthly bills also are likely an issue. Consumers are reminded every month just how much their service costs, and many likely are irritated by the many above the line or below the line taxes, fees, assessments that are part of most bills in the communications and video entertainment business.

It is hard to measure, but consumers might express frustration with customer service because they already are dissatisfied with the value and price relationship of the underlying service.

ISPs get terrible reviews, for example, but the reasons might lie more with unhappiness about the service than the customer service.

However, the 2013 Information Sector report from the American Customer Satisfaction Index shows that customers are happier with telecommunication services and technologies than they were a year ago.

The Information sector benchmark—the combined aggregate score for wireless telephone service, Internet service providers, subscription television service, cellular telephones, fixed-line telephone service and computer software—climbed 0.6 percent to 72.3 on a 0 to 100 scale.

“High monthly bills combined with problems across a broad spectrum of customer experience benchmarks—such as service reliability, data transfer speed and video-streaming quality—leaves customers less than satisfied with their ISP service,” the ACSI indicates.

Subscription television service ended a three-year run of stagnating customer satisfaction with a three percent gain to an ACSI benchmark of 68. While the boost is good news for cable, satellite and fiber-optic television providers, the industry remains the third worst of the 43 industries covered in the ACSI.

Among TV service providers, those offering service via fiber optics or satellite earn the best marks for customer satisfaction.

On average, fiber-optic/satellite service received an ACSI score of 72 compared with 63 for cable service.

While most cable providers did better in 2013, all remained below the national ACSI average.

ACSI director David VanAmburg noted that “the industry’s pattern of yearly price increases, coupled with sporadic reliability, keeps customer satisfaction low relative to other household services and vulnerable to new technologies that enter the market.”

ISPs earned a customer satisfaction benchmark of 65, the lowest score among 43 ACSI industries.

“High monthly bills combined with problems across a broad spectrum of customer experience benchmarks—such as service reliability, data transfer speed and video-streaming quality—leaves customers less than satisfied with their ISP service,” said Fornell.

Only Verizon’s FiOS and the aggregate of all other smaller ISPs break out of the 60s with identical ACSI scores of 71.

The mobile phone industry reversed a two-year trend of declining customer satisfaction with a 2.9 percent gain to an ACSI benchmark of 72. Despite matching its 10-year high, wireless service remains well below the national ACSI average.

“Barriers to switching, including contracts with cancellation fees, make the wireless industry less competitive,” said VanAmburg. “ACSI research shows that customer satisfaction is almost always lower when consumers have less choice and more headaches when it comes to switching to another seller.”

Fixed network phone service customer satisfaction increased 5.7 percent to 74. The paradox is that since unhappy customers are abandoning fixed network voice service, the remaining customers are those who value the service more, leading to higher scores.

The point is that unhappiness with the product tends to lead to unhappiness with opinions about customer service, even when providers are working to improve that element of the experience.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Oddly Enough, it is Nearly Inpossible to Tell Whether A La Carte Video is "Better" for Consumers and Distributors

Just what will happen to the economics of the video subscription business if Canada moves to complete unbundling of video subscription channels is unclear. It is virtually certain that programming networks will suffer.

In the U.S. market, for example, about 35 channels represent about 66 percent of all programs watched, on all channels. In a universe of hundreds of channels, that suggests most channels would either fail, or be forced to raise end user prices to compensate for lost advertising and affiliate fees (fees paid to distributors based on the number of subscribers).

In the case of advertising potential, lightly-viewed channels would retain a small fraction of their current “viewership potential.” Since advertising is sold on the basis of potential viewers, that would devastate ad revenue streams.

Also, since affiliate payments to networks by distributors also are based on the potential number of viewers, the affiliate revenue stream also would diminish.

What is unclear is the impact on service provider distributors. On one hand, a full a la carte environment would lead some subscribers to downgrade to much-smaller menus. In other words, viewers really wanting only a few channels would be able to pay less, reducing service provider revenues.

On the other hand, distributors face a growing threat of product abandonment, so some downgrading, while generating less revenue per account, would still be better than losing customers outright.

Much would depend on how any unbundling rules were promulgated. If current versions of retail packages still could be allowed, but customers also had the option of buying their channels one at a time, the revenue losses would be contained.

In other words, heavy users, watching a dozen or more channels, would still be better off buying the standard packages, so revenue from a substantial percentage of video subscribers might be largely unaffected.

Users who really only want a few channels would pay less, and distributors would lose some revenue in such cases. In between, some users would find an a la carte menu of channels costs about the same as the standard packages. In such cases, it would still make sense to buy a standard video bundle.

Almost without question, programmer affiliate payments would have to increase substantially, as networks raised prices to offset lower ad revenue. In addition, marketing costs would grow substantially, as networks suddenly would find themselves compelled to market themselves more intensively.

Some have suggested the revenue losses to service providers and networks would be quite substantial.

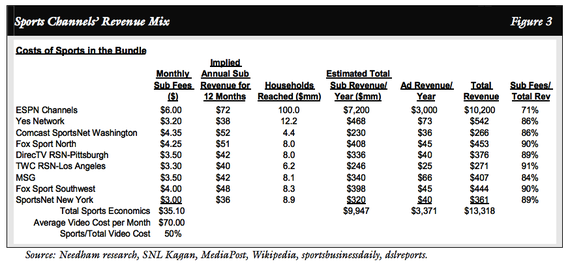

According to a study of the U.S. market conducted by Needham Insights, half the industry’s revenue—about $70 billion—would disappear if people didn’t have to pay for bundled television.

A bit less than half of that loss would probably be borne by distributions, and more than half by the networks. Needham Insights thinks only 20 U.S. networks would survive, Needham believes.

Whether that would be the case is, of course, unclear. Only after consumers were faced with real choices, and actually figured out what it might cost to go a la carte, would we see how consumer behavior might change.

Some studies suggest most consumers would not save much. It all depends on how many channels an account holder wanted to purchase.

ESPN, for example, costs U.S. cable TV providers about $5.15 per customer each month. In an a la carte regime, ESPN might have to raise its prices to distributors to $13 per month to make the same amount of money, according to Nielsen.

But wholesale costs could be much higher. It is impossible to estimate, at the moment. Some estimate subscribing to the ESPN family of channels alone could cost as much as $30 a month.

The issue is reach. ESPN advertising and affiliate fees rates are set on a base of 100 million U.S. homes. In an a la carte world, if subscribing households dropped to 20 percent of that amount, affiliate fees would rise commensurately, to about $6 times five, or $30.

All of that ignores the other changes that would happen, though. ESPN would look for ways to reduce its costs. And that would ripple back through the value chain, likely reducing the fees ESPN was willing to pay for sports rights.

The point is that one change--the shift to a la carte--would set off a series of other changes, of unknown magnitude. And much would hinge on whether traditional bundles remained available.

At least some service provider executives think distributors could win in an a la carte environment. That could be the case if distributors were able to keep customers they otherwise would lose, by offering more-affordable packages, with rights fees commensurately reduced.

At least some distributor executives might also believe that the only way to halt the spiral of annual price increases is for the government to intervene, by mandating a la carte wholesale offers for distributors, who then could offer a la carte to customers.

That presumably would reduce leverage held by content companies, often able to require that distributors pay to carry lightly-viewed channels in order to gain rights to "must have" networks.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...

{kind=link}