No telco executive with profit and loss responsibilities is unmindful about the urgency of addressing the twin challenges of revenue and cost in the business.

Precisely how to change, and how much benefit can be obtained by making changes, is the issue.

And though it is easy to conclude that access providers simply are not very good at creating new revenue streams while attacking cost elements of the business, that common perception--however correct--trivializes the “really hard problem” being faced.

Consider one obvious problem, namely the impact of rapidly-growing video bandwidth consumption.

The biggest problem--and the issue arguably affects mobile access providers at about two orders of magnitude more than a fixed network access provider--is that dramatically higher demands for Internet bandwidth on the part of customers does not automatically translate into “revenues” for the access provider.

Instead, such demand creates a requirement for continual investment in facilities, without directly providing incremental revenues to match. As the conundrum often is described by Norman Fekrat, Lemko Corporation chief strategy officer, mobile service provider Internet data costs are “$10 a gigabyte when they need to be 15 cents a gigabyte.”

Some will immediately be tempted to quibble about those figures of merit, but the larger point is the two orders of magnitude gap between mobile and fixed network costs per gigabyte of delivered data.

As a working hypothesis, assume that a $10 per gigabyte retail price, with a 40 percent margin, means the network-related cost is about $6 per gigabyte in the mobile realm, and something more like $1 per gigabyte in the fixed network realm.

The “problem” with Internet access is that it represents about 15 percent of revenue but 85 percent of utilization of network resources, one study estimates.

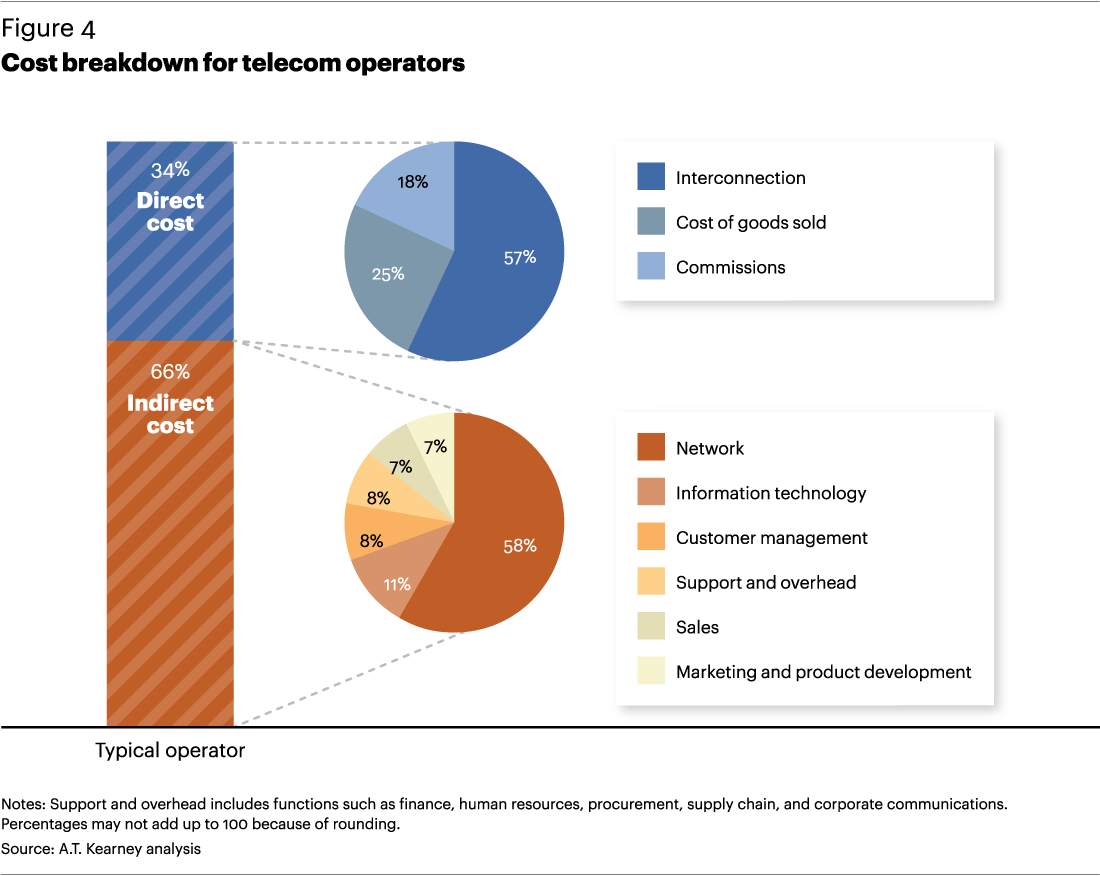

We are talking about “costs” that substantially involve allocated charges, so keep in mind the total actual cost of any service involves not only direct “network” costs, but also some allocated portion of all the other marketing, depreciation, interest expense, legal and regulatory fees, pension plan and other necessary expenditures as well.

In fact, indirect costs that must be allocated represent as much as 66 percent of total costs, by some estimates. “Interconnection,” largely to support voice and messaging services, could represent 19 percent of direct costs, for example.

Network operating costs could represent 38 percent of total operating expense, including personnel costs.

Marketing and sales overhead might amount to nine percent of revenue, excluding direct sales commissions.

Some see “transit costs” and assume that is the actual underlying cost of providing Internet access, but that really represents only a portion of total costs. Even looking only at the physical cost of delivering useful bandwidth, transit is part of cost (across the backbone), not including “access,” which, traditional rules of thumb suggest, are about 80 percent of end-to-end cost.

The larger point is that to reduce “cost per gigabyte” by two orders of magnitude, while retaining the advantages of mobility, an access provider necessarily must attack costs across a range of essential activities.

Simply reducing “transit” or wide area network transport, between points of presence, will not, by itself, achieve the required change in cost profile, especially if the dominant network-related costs are in access.

Then there is the rest of the cost profile. If one assumes capital investment of about 12 percent to 15 percent of revenues on a sustainable basis (newer networks spend more; fixed networks spend less; mobile networks sometimes more), some part of that represents costs that possibly could be avoided.

Dividend-paying telcos have other huge requirements, though, such as dividend payments that can represent 50 percent of free cash flow.

Pension liabilities might represent a claim on five percent of revenue. Information technology might represent up to five percent of revenue.

In other words, there are many cost drivers. Still, reducing network capital requirements, as well as network operating costs, across all supported revenue-generating services, could be quite significant, the biggest potential savings coming from reducing overhead associated with operating the network, rather than the cost of capital investment in facilities.

The point is that dramatic changes, likely across a range of functional activities, probably is required to reduce the cost of supplying mobile gigabytes to end users from $6 a gigabyte to the fixed network level of perhaps $1 a gigabyte.

Right now, offload of mobile data is the most useful way of achieving that aim, for a mobile service provider. The issue is whether there are other ways of doing so in the core or access networks.

Access providers who own spectrum have one set of options. Access providers who own fixed access assets likely have a different set of options. Non-facilities-based providers have a third set of options.

Large, dividend-paying firms face substantially harder tasks. How one handles the packet core, and the access network are key. But even vast improvements in those areas only address a fraction of total direct and indirect costs.

If it were easy to bring about dramatic cost reductions, service providers already would have done so.