One unanswered question about the current U.S. mobile market wars has been whether, when and how Verizon might respond.

It looks like Verizon has been forced into the fray. Reportedly, "Share Everything" plans will become "More Everything" plans, with lower prices, higher usage caps and unlimited messaging to anywhere in the world from the United States.

Wednesday, February 12, 2014

Verizon Wireless Seems Forced to Respond to Mobile Market Wars

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

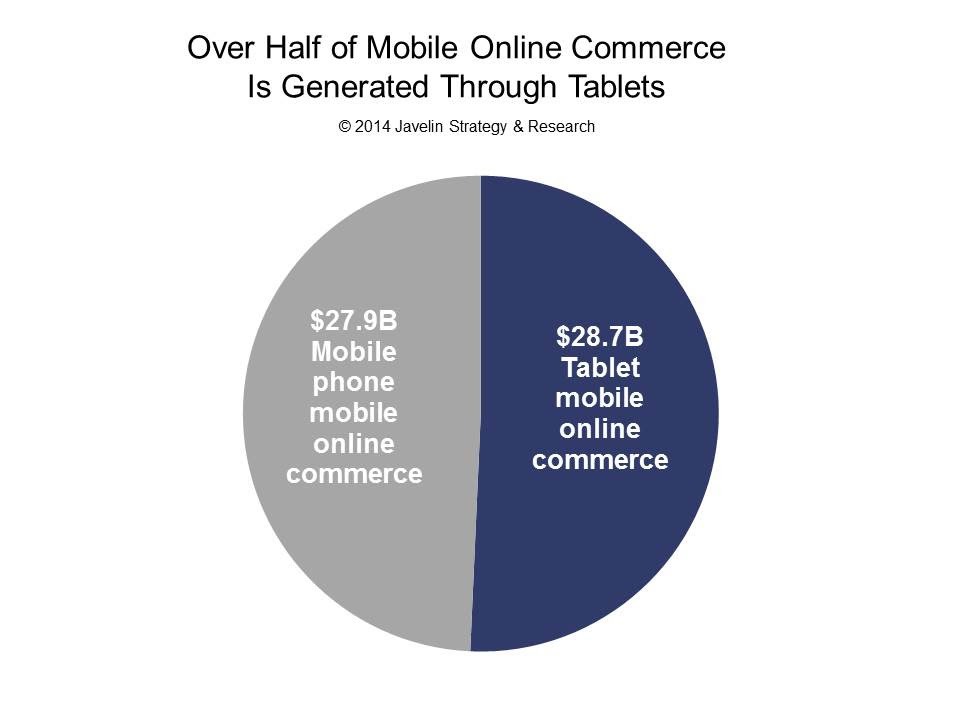

Tablets Drove Half of Mobile Commerce in 2013

2013 marked an important mobile payment's “first,” with tablet payments comprising almost half of all mobile commerce, according to Javelin Strategy & Research.

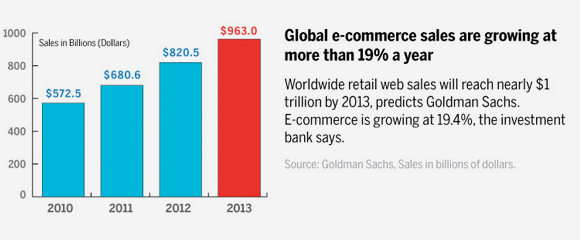

Of course, all forms of mobile commerce continue to lag e-commerce as a whole, representing perhaps $960 billion to more than $1 trillion in annual sales in 2013.

In 2013, tablets accounted for $28.7 billion in mobile online commerce, or over half of the entire mobile online payments space, up from the 2012 level of $5.1 billion.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

In 2013, tablets accounted for $28.7 billion in mobile online commerce, or over half of the entire mobile online payments space, up from the 2012 level of $5.1 billion.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Hard to Say Whether Typical Internet Access Prices Have Climbed or Dropped

Relatively minor changes in broadband access pricing are not uncommon. A price hike for Clear service provides an example.

Relatively minor changes in broadband access pricing are not uncommon. A price hike for Clear service provides an example.

But assessing changes in Internet access pricing is difficult, since the typical pattern is for the actual product to change over time.

Consumers might once have paid $20 to $22 a month for a dial-up connection operating at 56 kbps to 128 kbps. Consumers now pay about $40 a month for a 15 Mbps connection. So absolute prices have increased, but prices per megabit have declined.

Also, the types of products have changed over time. Where once consumers had only one choice--dial-up access or no access--they now can buy service at varying speeds, with the faster services costing more each month.

That obviously skews spending patterns. If more people choose to buy faster access, “average” spending also rises. Something like that likely happened in 2009, as more people chose to upgrade to faster levels of service.

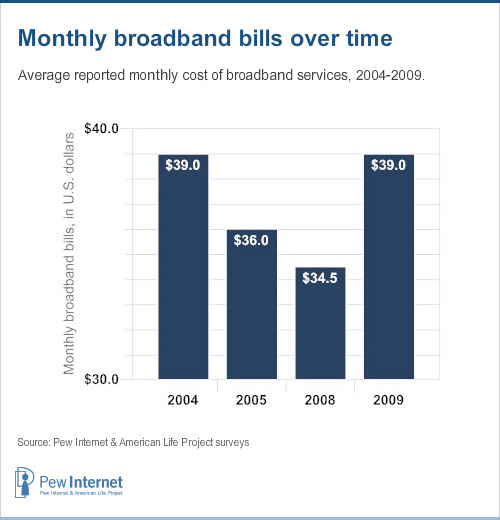

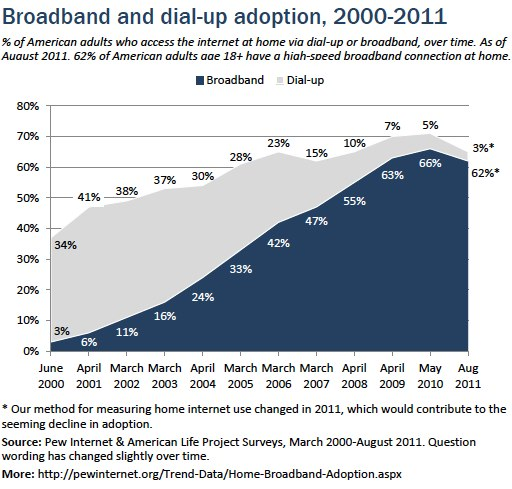

The increase in what people pay for broadband is evident in prices for basic and premium services, according to the Pew Research Center's Internet & American Life Project.

For subscribers to basic services, the average monthly bill was $32.80 in 2008, a figure which rose to $37.10 in 2009.

For premium subscribers, those thirsty for faster home broadband speeds paid about $38.10 per month in 2008 and roughly $44.60 in 2009.

For premium subscribers, those thirsty for faster home broadband speeds paid about $38.10 per month in 2008 and roughly $44.60 in 2009.

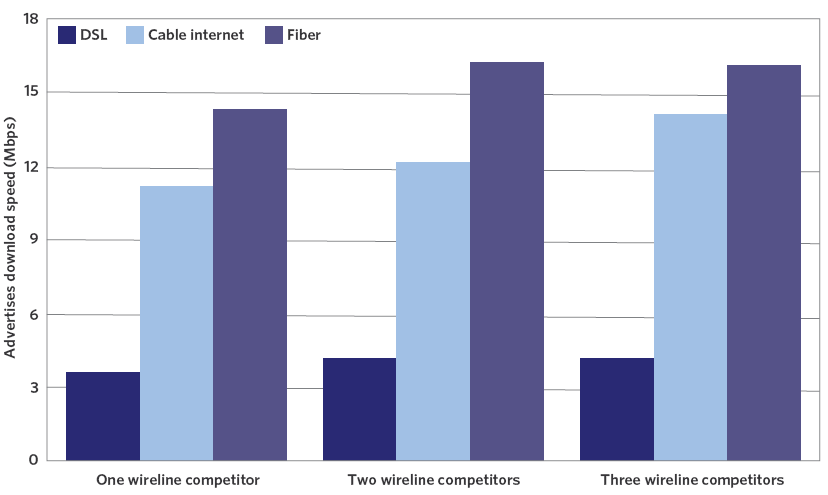

Across different service types, broadband subscribers reported higher prices for cable modem service than DSL by a $43.20 to $33.70 margin. This compares with 2008 figures of $37.50 for cable modem subscribers and $31.50 for DSL users.

That shift in demand--from DSL to cable modem, for example--also affects average pricing, as cable offers tend to be faster, on balance.

The point is that the actual product consumers are buying has differentiated over time, and appears to be in the process of segmenting further, as top end services start to stretch an order of magnitude.

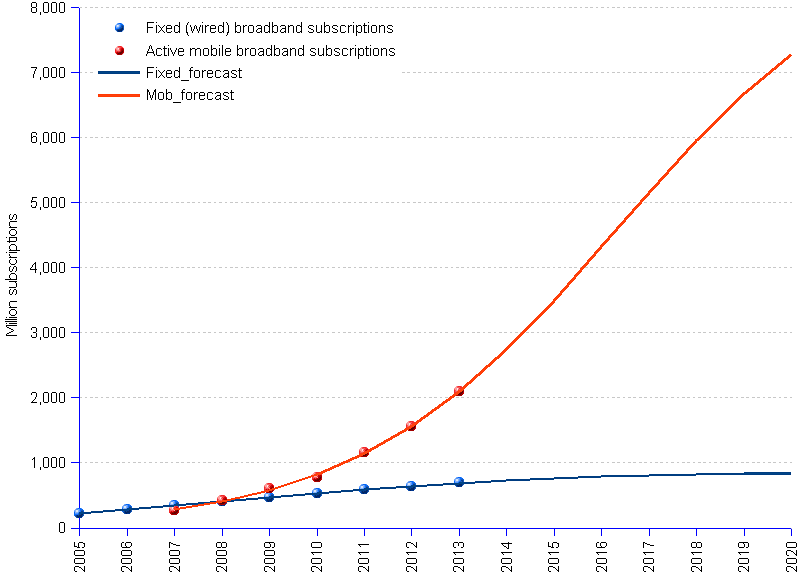

The other important change is the rise of mobile Internet access as a material factor in the market. By about 2020, about 10 percent of all broadband connections will be supplied by fixed lines, the overwhelming majority of connections being supplied by mobile networks.

The other important change is the rise of mobile Internet access as a material factor in the market. By about 2020, about 10 percent of all broadband connections will be supplied by fixed lines, the overwhelming majority of connections being supplied by mobile networks.

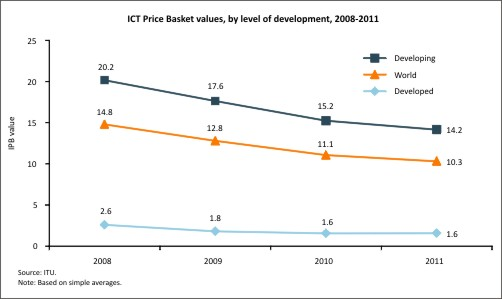

On a percentage of household income basis, Internet access prices have been dropping globally, with the biggest changes in developing markets. Though prices have dipped in developed nations, the changes are relatively slight.

Average Top Advertised Speed

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Tuesday, February 11, 2014

Will TV Delivery Go Non-Linear?

Though communications service providers might prefer growth, they probably would not be too perturbed about a service whose take rates or adoption was declining less than 0.7 percent annually, especially when average revenue per unit was growing about four to five percent annually.

But that is about the industry-wide dip in subscriber numbers in the U.S. market, it appears, according to Forrester Research. With the important caveat that most trends in technology, media or communications have adoption rates that vary tremendously over time, if the slow decay of traditional video subscriptions continues at present rates, change will be graceful, for content providers, video distributors and others in the ecosystem.

Of course, when new products displace older products, there tends to be a longish period when nothing too dramatic seems to happen. And then there is the inflection point, and change becomes non-linear.

So as logical as it might seem to base actions on the theory that "tomorrow will pretty much be like today," that will prove a dangerous notion if change goes non-linear. And big changes that affect "most people" often have a non-linear adoption pattern, in the end.

If that is the case, we might not be able to infer very much from current trends in subscription TV.

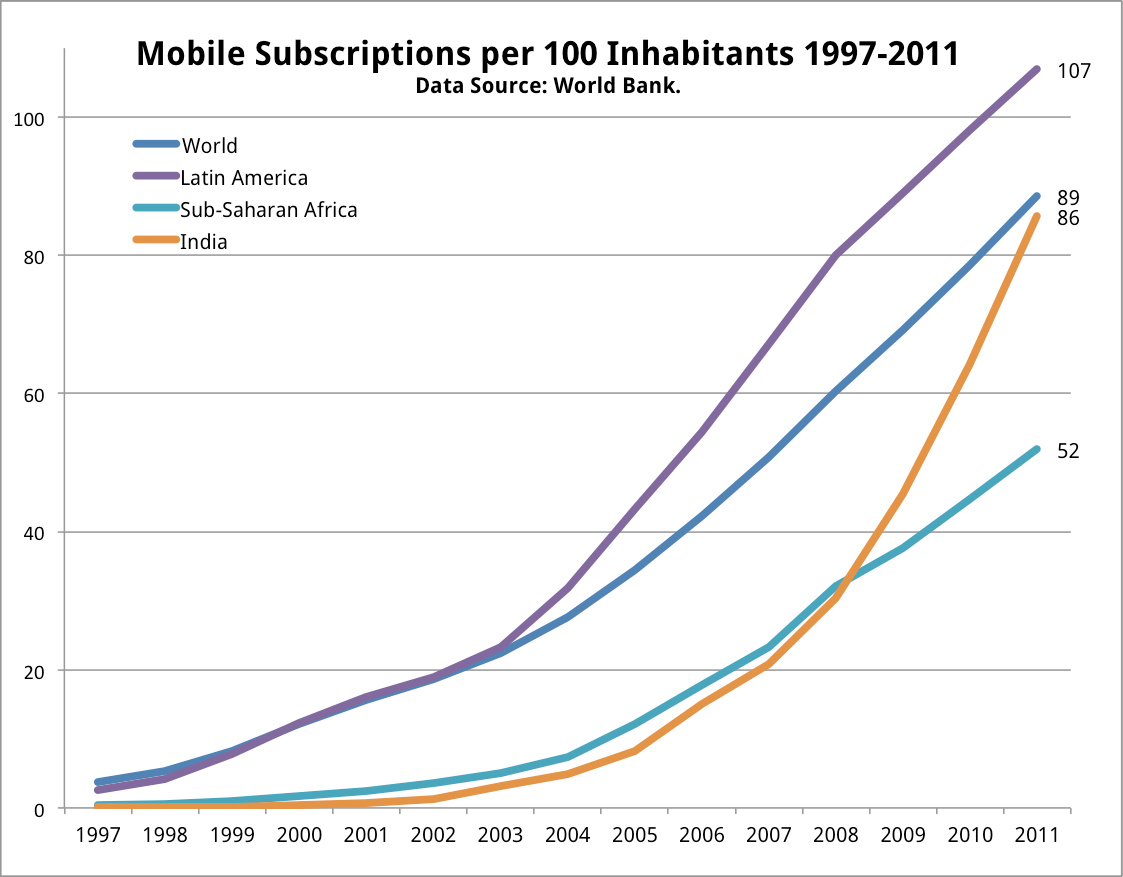

Mobile adoption, for example, shows the non-linear adoption pattern. Adoption patterns, especially in India and sub-Saharan Africa illustrate the difference between pre-inflection point growth and post-inflection point growth.

The same is likely to happen to subscription TV, if online delivery really develops as a substitute product.

But that is about the industry-wide dip in subscriber numbers in the U.S. market, it appears, according to Forrester Research. With the important caveat that most trends in technology, media or communications have adoption rates that vary tremendously over time, if the slow decay of traditional video subscriptions continues at present rates, change will be graceful, for content providers, video distributors and others in the ecosystem.

Of course, when new products displace older products, there tends to be a longish period when nothing too dramatic seems to happen. And then there is the inflection point, and change becomes non-linear.

So as logical as it might seem to base actions on the theory that "tomorrow will pretty much be like today," that will prove a dangerous notion if change goes non-linear. And big changes that affect "most people" often have a non-linear adoption pattern, in the end.

If that is the case, we might not be able to infer very much from current trends in subscription TV.

Mobile adoption, for example, shows the non-linear adoption pattern. Adoption patterns, especially in India and sub-Saharan Africa illustrate the difference between pre-inflection point growth and post-inflection point growth.

The same is likely to happen to subscription TV, if online delivery really develops as a substitute product.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Public Wi-Fi Does Not Have to "Compete" with Mobile to Provide High Value

Some questions never go completely away. Whether Wi-Fi can compete with mobile networks seems a perennial question. It was asked of 3G networks and now is asked about 4G networks.

Some mobile service providers, including Scratch Wireless and Republic Wireless , actually build their mobile services on primary use of Wi-Fi connections, automatically defaulting to Wi-Fi for voice and Internet access whenever possible, and then switching to 3G only when Wi-Fi connections are not available.

As newer blocks of spectrum (5 GHz, 60 GHZ) are opened up for commercial use, the questions--and the potential--are likely to grow. But the questions will be asked in a new context.

Wi-Fi is a low-power application, compared to mobile service, which is a high-power application. Over time, the predominant use of a mobile device--especially a smartphone--has shifted from apps where high power is required (on the go calling, texting or Internet access) to application scenarios are well suited to low power.

That puts the older question--can Wi-Fi compete with mobile--into a new context. Originally, the question might have been whether public Wi-Fi could approximate the connectivity of a mobile network for purposes of making phone calls.

The original value proposition for mobile phones was “calling on the go.” So the potential use of public Wi-Fi was to create a viable network to support calling. These days, smart phones are multi-function devices, used for calling, texting, messaging and content consumption.

And the use venues are different as well. These days, perhaps only 10 percent to 20 percent of total mobile device usage, for all apps and purposes, actually happens when people are “on the go.” all the rest of the usage is in untethered mode at locations where there is Wi-Fi access.

In other words, content consumption now is a major mobile device activity, and most of that consumption does not happen in mobile mode. In other words, the new pattern for content access is primarily untethered, not mobile.

And one might argue that future needs for network capacity increasingly will focus on low-power, localized access, not high-power mobile access. That is why one hears so much about small cells and carrier Wi-Fi, as well as Wi-Fi offload, these days.

That casts the question of whether public Wi-Fi can compete with mobile networks in a new light. End user requirements and device usage have changed.

The crucial need is not so much the usefulness of public Wi-Fi to support voice, but its usefulness in supporting content consumption. Public Wi-Fi might have some value for occasional offload of voice, but it has high value for offload of content consumption, in large part because content consumption does not typically require handing off sessions from one macrocell to another.

The big change to the way we interact with WiFi will only be seen as the HotSpot2.0 standard gains wider adoption. This initiative is based largely on the 802.11u standard and will genuinely transform the industry.

The Hotspot 2.0 standard should improve the utility of public Wi-Fi further, allowing an easier authentication experience, especially for users of public Wi-Fi hotspot services.

So the new question is not so much whether public Wi-Fi can compete with mobile networks, but whether public Wi-Fi will be useful for smart phone content consumption, to say nothing of providing meaningful primary access for devices that also can default to mobile networks when required.

That is a different question than we used to ask. And the point is that the usefulness of public Wi-Fi networks will be dramatically higher as more device communications is supplanted by device media and content consumption.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Grande Communications Launches Gigabit Service in Austin, Texas in February 2014

Grande Communications plans to launch gigabit access service in parts of Austin, Texas by Feb. 18, 2014, beating both Google Fiber and AT&T in launching 1 Gbps services in Austin.

Longer term, one has to expect a resetting of price and value expectations for all the slower-speed services, even if there is no wholesale resetting of prices in the near term.

Grande will sell gigabit service for $64.99 per month, undercutting. AT&T’s “GigaPower” service for $70, as well as Google Fiber, also selling for $70 a month.

Grande says its service will have no contracts or bandwidth usage caps, and initially will be available in west Austin neighborhoods, representing about 25 percent of Grande’s addressable market in Austin.

If take rates are as high as Grande expects, the gigabit service will be rolled out to other Grande-served neighborhoods as well.

What isn’t immediately clear is what impact the gigabit offer will have on take rates for other Grande offers in Austin.

Grande has launched faster speeds offers in Austin, Corpus Christi, Dallas, Midland, Odessa, San Antonio, San Marcos and Waco. Though markets outside Austin will not be affected directly, demand in west Austin clearly will be affected.

The new Internet speed options begin at 15 megabits per second for $35 a month and include other offers at 50 Mbps ($45 a month) for 75 Mbps ($55 a month) and 110 Mbps ($65 a month).

In the west Austin neighborhoods where gigabit service is available, the 110 Mbps service obviously will be cannibalized by the gigabit service, which costs the same. But the other issue is how many customers will determine that a gigabit service for $65 is preferable to a 75 Mbps service for $55 a month.

Longer term, one has to expect a resetting of price and value expectations for all the slower-speed services, even if there is no wholesale resetting of prices in the near term.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

8 ISPS Respond to Gigabit Network RFI

With the caveat that "interest" might not actually represent "intent to provide," eight Internet service providers have responded to a request for intormation on gigabit Internet access networks issued by the Louisville-Jefferson County Metro Government.

The request sought information about how a gigabit-capable network could be provided across the city or in targeted commercial corridors and in residential areas and how gigabit service could be delivered at prices comparable to other gigabit fiber communities across the nation.

City officials hope to lure a vendor who will provide commercial gigabit Internet service at symmetrical speeds, up and down. Time Warner Cable and AT&T are said to be among the firms that responded to the request for information.

City officials apparently are willing to entice would-be providers by allowing access to city rights of way, including waterlines, sewer lines and alleys.

In some ways, the RFI illustrates new thinking about ways municipalities can offer inducements to ISPs interested in creating new gigabit access networks. Municipal officials in this case do not seem to envision a full public-private partnership, but instead simply easier and presumably low-cost access to rights of way and conduit that would allow ISPs to cut the cost of building any such new networks.

What will be interesting is whether municipal officials are willing to allow partial builds only in parts of the metro area, instead of mandating 100-percent coverage, which might not be feasible.

In essence, that would mimic the way competitive local exchange carriers have tended to create new networks, building only where there is clear customer demand. In the case of CLECs focused on business customers, that has meant focusing on business districts and office parks, for example.

In a consumer context, the same approach might allow ISPs to build only in residential neighborhoods where customer demand was high enough to promise a potential financial return.

Though the concept clashes with historic notions about universal access, such approaches have proven effective at stimulating new network capacity.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...