|

| source: Quartz |

The medium-term implications of a $1 a month price increase for Netflix streaming plans are not yet clear, as existing streaming customers will continue to pay the older prices for two years. So churn should not be material, in the near term.

The real issue is whether the price increase will slow net additions, and if so, for how long.

Some now wonder whether an Amazon Prime subscription price increase from $80 annually to $100 annually, or a $1 a month increase for new Netflix consumers will slow the growth of online video market. At the margin, temporarily, one would guess the answer has to be “yes.”

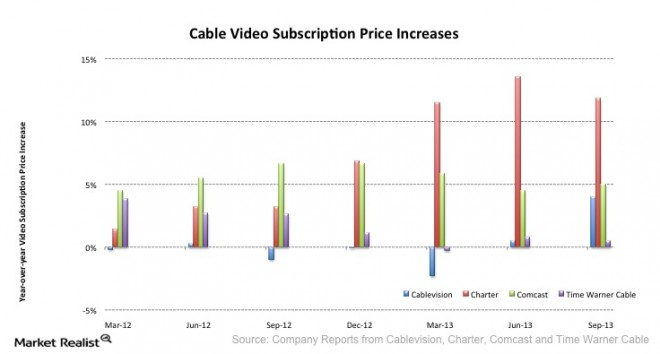

A slightly higher price for the most-popular Netflix streaming package will cause some consumers to think a little harder. Still, an increase from $8 to $9 a month is relatively slight, in absolute terms, and far less than the $4 to $6 monthly increases linear video subscribers see every year.

For most new consumers, and in two years the base of current customers, the decision context is not the $1 a month price increase. The decision to buy a streaming video service will be evaluated against the cost of broadcast TV, linear video subscriptions, the cost of rival streaming alternatives, and the value each option represents, as well.

|

| source: FCC |

And the “value” of a Netflix subscription, or Amazon Prime, will grow over time as both firms invest in original programming.

A growing preference for on-demand viewing across almost every demographic also will have impact on the “value” of such subscriptions, increasingly over time.

Absolute demand for for television, as a product, also seems lower in younger households.

We are likely to see a test of the value-price proposition later in 2013, if Dish Network succeeds in launching a lower-price streaming service featuring linear TV channels. That offer, presumably priced at $20 to $30 a month, for a smaller package of linear channels, could surface demand for linear video among resisters, or latent demand for such a product by existing customers.

Should that effort succeed, and should other major suppliers launch similar offers, demand for the new linear video packages might be significant, indeed, as linear video subscription price elasticity seems to be growing negative, if it is not already negative.

In other words, a one percent increase in retail price should lead to more than a one percent decrease in buying. That does not seem to have happened, in the linear video entertainment business.

The reason is the emergence of triple-play packages that effectively discount the value of constituent services. So while stand-alone video subscriptions might indicate the magnitude of price increases, it increasingly is the case that most buyers do not pay those prices.

|

| source: Market Realist |

Though it is presently a reasonable assumption that some Netflix or video streaming customers have chosen to buy Netflix in place of a linear subscription service, most Netflix subscribers seem to be buying Netflix as an incremental addition to their video entertainment service.

What does seem to be true is that many Netflix subscribers are substituting Netflix for a premium channel such as HBO. And Netflix and other streaming services such as Amazon Prime and Hulu are driving growth of the over the top and linear video service offerings of subscription video on demand services as well.

In the first quarter of 2013, for example, the number of viewers watching television shows using SVOD services increased 34 percent, compared to the same quarter of 2012, NPD Group reports.

In fact, streaming video subscriptions grew four percent in 2012 and 2013, while premium TV channels declined six percent. At the beginning of 2014, 32 percent of U.S. households subscribed to a premium channel, while 27 percent subscribed to a streaming video service.

Some 7.6 million Internet-owning Americans can be classified as “cord-cutters” who don’t subscribe to cable TV, according to Experian Marketing Services, representing perhaps 6.5 percent of households.

Still, since at least 27 percent of U.S. households buy Netflix or some other video streaming service, most are supplementing a traditional video subscription. More than 80 percent of Netflix and Hulu subscribers, for example, say they buy both a linear video subscription and a streaming video subscription.

The point is that neither Netflix nor the other streaming services are “mostly” a substitute for linear video subscriptions. Instead, Netflix supplements purchasing of video entertainment.

Nor is the relationship between product price and buy rates so clear. A cable TV, satellite TV or telco TV subscription can cost more than 10 times what Netflix does. Nor have virtually annual price increases for linear video products significantly increased overall linear video churn. Instead, most of the Netflix-only behavior seems to be anchored in some households, namely Millennial and younger households (18 to 34).

U.S. video subscribers grew every year, until flattening in early 2013. For all of 2013, the linear video market lost about 105,000 total subscribers, on a base of 105 million subscribers.

Is price an issue? Yes. So is “perceived value.”

Availability of reasonable partial substitutes also is an issue for the first time. It wasn’t until widespread availability of satellite alternatives that significant numbers of consumers switched providers. But that did not slow the growth of the whole market; it just shifted market share while overall market growth continued.