Smartphone adoption in the Philippines is nascent. Of that nation's 97 million people, smartphone penetration is about 15 percent, though mobile penetration is about 101 percent, and Internet penetration is about 39 percent.

In Malaysia, smartphone adoption is 80 percent, in Singapore 87 percent, in Thailand 49 percent. In Indonesia, adoption is at 23 percent.

But that is expected to change over the next several years as low-cost smartphones costing between $50 and $250 are made available in all markets.

Today's mobile Internet users are young, under 34 years of age. About 35 percent of mobile Internet users are between 25 and 34. Fully 53 percent are 16 to 24, according to On Device Research.

And mobility already is a big trend in computing. Some 30 percent of respondents to a survey own tablets, for example, compared to 23 percent ownership of desktop PCs. About 25 percent of respondents own notebooks or laptops.

About 44 percent of mobile Internet users spend less than $12 a month on their data plans. About 32 percent of mobile Internet users spend between $12 and $41 a month on their data plans.

About half of all respondents say they have unlimited data access plans. About 17 percent have 10-Gbyte plans. Some 12 percent have 3-Gbyte plans. About seven percent have plans of 700 Mbytes or less.

About 40 percent of respondents report spending at least five hours a day on their devices, and about 42 percent of total "screen time" is spent with social media. Over half of respondents say they stream music on their devices.

About 70 percent of respondents who say they use Spotify, for example, are on a mobile data plan sold by GoSURF that bundles free access to Spotify as part of the mobile data plan.

That is an example of the power of app bundling, even if such preferred access violates notions of "no application favoritism" that network neutrality supporters say they support.

Mobile banking should emerge as an important value for smartphone users, as 73 percent of the population does not have a bank account, while credit card use is about three percent.

Wednesday, July 9, 2014

Low-Cost Smartphones, App Bundling Will Drive Philippines Mobile Internet Adoption

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, July 8, 2014

Netflix's Problem Is Its Transit Network

Netflix has been arguing that some major Internet service providers are responsible for performance issues.

But an engineer says the transit network is responsible, not the ISP access networks.

Simply, Netflix has insufficient middle-mile bandwidth, sourced from IP transit companies, argues Peter Sevcik, president of engineering consultant NetForecast.

But an engineer says the transit network is responsible, not the ISP access networks.

Simply, Netflix has insufficient middle-mile bandwidth, sourced from IP transit companies, argues Peter Sevcik, president of engineering consultant NetForecast.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Sprint Tests Consumer Shared Data Plans

Sprint is said to be testing shared data plans for consumer accounts. If that seems unremarkable, consider Sprint’s earlier statements on such plans.

In 2012, Sprint argued that sharing data is inferior to unlimited data. T-Mobile US likewise argued that unlimited data was the preferable approach.

In other words, shared data plans seem to resonate with many consumers.

That sort of reaction--downplaying an innovation by competitors--is not unexpected in the mobile business. On the other hand, neither do such protestations last too long if it turns out the innovations resonate with consumers.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Uber Only Faces the "If it Looks Like a Duck, It's a Duck" Problem; Capacity Markets Face Margin Compression, Shrinking Markets

Uber is finding out that in regulated markets, even when new technology and business models are pioneered, regulators use a simple test, not much more complicated than captured by the phrase “If it looks like a duck, swims like a duck, and quacks like a duck, it’s a duck.”

|

| source: TeleGeography |

Aereo found itself facing the same problem when courts ruled that Aereo essentially is a cable TV business, and must pay licensing fees to redistribute off-air TV signals.

VoIP providers found that to be true after they started to take significant market share from legacy providers.

In other words, even new technology and clever business models will long survive regulatory scrutiny and compliance when the new approaches are applied in competition with legacy businesses.

So now Uber is slowly conceding to demands that its drivers and services be subject to the same rules as apply to licensed taxicab firms, Aereo has been ruled illegal and connected VoIP services pay the same taxes and fees as do legacy voice services.

Sometimes the Internet has other impact on legacy businesses, especially when applied to non-regulated industries.

Publishing and music already have seen a profound change in industry revenue potential, as well as changes in the way content is created, presented and distributed to consumers and customers.

In other cases, the Internet can transform an industry by making the market smaller.

In other words, it has now become a fact of business life that the Internet not only brings efficiencies to any market it touches, but actually can destroy legacy markets.

And that might be the fate of the wide area network capacity business. In 2003, the global private line business generated about $36 billion in annual revenue. By about 2016, private line revenue might hit $42 billion.

But there is an unmistakable trend: legacy voice and capacity revenues are declining, at least in in developed markets.

Between 1997 and 2007, for example, long distance, which represented nearly half of all U.S. telecommunications revenue, was displaced by mobile voice services.

The point is that such revenue declines put unrelenting pressure on the capacity business, as wholesale services are sold to customers who must not only attack their own operating and capital costs, but also can build and operate their own facilities in an effort to do so, creating the opportunity for converting transit payments into network infrastructure investments, instead.

That has the effect of putting pressure on transit revenue opportunities and capacity sales, as service providers build their own captive networks.

For example, consider that the IP transit market generated $2.1 billion in revenues in 2013. Sales of circuits connecting customers to Internet hubs contributed an additional $2.5 billion, for a total of $4.6 billion in revenues, according to TeleGeography.

But consider that other new segments, such as content delivery networks , already by 2013 had grown to be a business generating perhaps $2.5 billion in global revenues, headed for perhaps $4.5 billion by 2017.

By way of comparison, U.S. local access revenues generated from business segment Ethernet access services passed $4 billion worth of revenue in 2011, and is projected to reach $11 billion by 2016.

And though global wholesale revenues might total $142 billion in 2019, that is driven largely by mobile service wholesale, not wide area network transport.

The point is that, all revenue sources considered, the long-haul capacity markets continually face the reality of customers building their own long-haul networks, trading operating expense for capital investment.

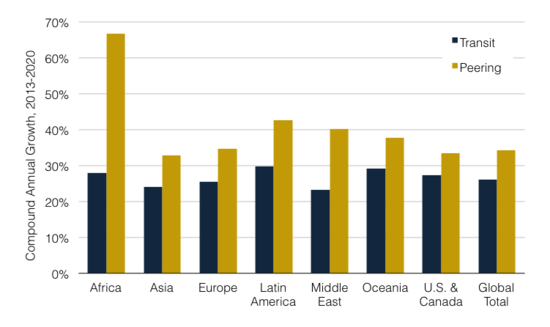

TeleGeography analysts say that the fate of the IP transit business rests on the growth of peering relationships that obviate the need for IP transit purchases.

“As Internet service providers worldwide have gradually migrated from purchasing transit to establishing mostly free peering arrangements, the share of global Internet traffic connected via transit agreements declined from 47 percent in 2010 to 41 percent in 2014,” TeleGrography says.

|

| source: TeleGeography |

In other words, undersea and long haul capacity, which once was a significant revenue stream, is gradually becoming a matter of private networks interconnecting without charge.

As long as this relative decline of transit continues, TeleGeography forecasts that IP transit-related revenues will fall from $4.6 billion in 2013 to $4.1 billion in 2020. If the ratios of traffic routed via transit and peering were to stabilize at current levels, IP transit revenues would increase to $5.5 billion by 2020.

So far, you might argue the effects have been somewhat subtle. While African Internet traffic is forecast to grow 36 percent annually over the next seven years, transit volumes will increase by only 28 percent compounded annually, while peering volumes will grow 67 percent—driving down the share of traffic routed via transit from 90 percent in 2014 to 61 percent in 2020, TeleGeography says.

Ignore for the moment the tendency of capacity services to decline in price every year. At least for the moment, peering economics seem to be strong enough to make investment in one’s own infrastructure a reasonable alternative to transit services.

Might that change in the future? TeleGeography says that could happen, if transit prices were to fall low enough.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, July 7, 2014

A Very Odd, but Wise, Instance of Telecom Rebranding

Of all the company "rebranding" efforts many of us have seen in the telecommunications business, the most unusual is the decision by the owners of the mobile payment service owned by AT&T, Verizon and T-Mobile US to adopt a new name.

The move is being taken because the acronym ISIS of course is associated with an unsavory group much in the news of late.

Isis apparently has not yet decided on a new name, but hasn't announced what the new name will be.

It's a wise move, if unprecedented, in my experience.

The move is being taken because the acronym ISIS of course is associated with an unsavory group much in the news of late.

Isis apparently has not yet decided on a new name, but hasn't announced what the new name will be.

It's a wise move, if unprecedented, in my experience.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

A Very Odd, but Wise, Instance of Telecom Rebranding

Of all the company "rebranding" efforts many of us have seen in the telecommunications business, the most unusual is the decision by the owners of the mobile payment service owned by AT&T, Verizon and T-Mobile US to adopt a new name.

The move is being taken because the acronym ISIS of course is associated with an unsavory group much in the news of late.

Isis apparently has not yet decided on a new name, but hasn't announced what the new name will be.

It's a wise move, if unprecedented, in my experience.

The move is being taken because the acronym ISIS of course is associated with an unsavory group much in the news of late.

Isis apparently has not yet decided on a new name, but hasn't announced what the new name will be.

It's a wise move, if unprecedented, in my experience.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Mobile ISP Role in M2M Will Largely be the Same Role as in Mobile Phone Business, Despite All Efforts

If the "machine to machine" (M2M) or "Internet of Things" market consists of “hundreds of micro-markets,” not a single industry, as a new Vodafone report suggests, then the logical conclusion also is that the role of mobile service providers in M2M or IoT markets will substantially replicate the industry's role in the mobile phone business.

In other words, the mobile service provider role largely will involve communications connectivity, not application-layer functions. Those who worry about "dumb pipe" roles can start worrying now.

If applications are highly fragmented and discrete markets are individually small, then it will make sense for mobile service providers to focus on the general purpose communications role, not a possible role as application suppliers.

That means mobile service providers--like it or not--will be "pipe suppliers," earning nearly all their M2M or IoT revenue from access services.

There are 4.4 billion machines or devices now connected to each other or to servers, growing 10.3 billion by 2018, a study sponsored by Vodafone predicts.

Still, since definitions of “machine-to-machine” or “Internet of Things” vary, it is hard to separate connected appliances such as televisions or game consoles from industrial sensors and monitors.

Within three years, most firms will be embedding M2M into the actual products and services sold to customers.

That likely has implications for the role of the mobile service provider in the ecosystem. If the application settings are highly fragmented, the easiest role for an access provider to adopt is “horizontal,” not “vertical.”

In other words, mobile service providers supply the communications function, not primarily vertical applications, much as the primarily value provided to business or consumer customers is mobile access (for phones, other personal devices and sensors), with a couple of general purpose applications (text messaging and voice).

About 22 percent of 600 executives involved in machine-to-machine strategy say they already have at least one active M2M deployment in operation, up about 80 percent in 2014, compared to 2013, according to a new study sponsored by Vodafone and conducted by Circle Research.

The three leading industries, in terms of deployment, are the consumer electronics, energy and utilities, and automotive industries, each with a minimum of 30 percent adoption by respondent firms.

By 2016, the percentage of respondents with at least one M2M deployment will be 74 percent, the study predicts, based at least part on the embedding of M2M features into products such as thermostats and kitchen appliances.

Energy and utility respondents will have boosted M2M deployment to about 62 percent by 2016, based on smart meters and grid monitoring programs.

Use of M2M in the transportation and logistics verticals will be 57 percent in 2016, based largely on fleet logistics applications, and adoption in the healthcare and life sciences industry will be identical, the Vodafone survey found.

Automotive segment adoption will reach 53 percent, while retail deployment reaches 51 percent. M2M deployment in manufacturing will be at least 43 percent, though self reporting might be underestimating the actual state of deployment, given the widespread use of automation in manufacturing. Some respondents might not call what they already are doing an instance of M2M deployment.

Safety and security applications are the leading uses of M2M in automotive settings, partly because in many regions they are being driven by regulation, such as the eCall programme in the European Union.

Consumer electronics is at present the leading adopter of M2M, with the highest adoption

of external-facing strategies, at 71 percent.

Those applications primarily include tracking mobile assets including shipping containers. But

20 percent of all company executives surveyed in the consumer electronics segment already are selling connected devices directly to consumers.

Asset tracking is expected to be important in the energy and utility segment, monitoring in health care, connected car services in the auto industry, monitoring in manufacturing and connected cabinets or asset tracking being lead apps.

Early adopters tend to say productivity and cost savings are the deployment drivers, with projects tending to be in the internal processes areas, rather than external operations visible to customers.

At the moment, adoption of at least one active deployment is highest in the “Africa, Asia, Middle East” region, a rather broad category of limited analytical usefulness, one might argue. But 27 percent of executives surveyed in that region had projects underway.

The study included respondents from Australia, Brazil, China, Germany, India, Italy, Japan, the Netherlands, South Africa, South Korea, Spain, Turkey, the United Kingdom, and the United States.

In Europe, 21 percent of respondents reported they had at least one M2M project in action. In the Americas, 17 percent of executives said they had at least one project in progress.

But Vodafone expects that, by 2016, deployment profiles will be quite similar, with more than half of all respondents supervising actual deployments.

As predicted in last year’s Vodafone M2M Adoption Barometer report, the US has been overtaken by the Asia Pacific region as the geography with the widest adoption of M2M. This year’s report suggests that by 2016 the gap will be negligible with all regions close to a 55% average for adoption.

The survey, carried out by Circle Research, captured the views of more than 600 executives involved in setting M2M strategy in seven key industries across 14 countries.

Three sectors have emerged as front runners in M2M with nearly 30 percent adoption rates: automotive, consumer electronics, and energy and utilities.

Automotive is the most mature of the sectors where M2M is now seen as an enabler for additional services such as remote maintenance and infotainment. M2M adoption in energy and utilities is also growing rapidly as ‘smart’ home and office services such as intelligent heating and connected security gain popularity.

This uptake is being fuelled by the use of M2M in connected devices such as smart televisions and games consoles. The research shows that nearly three quarters of consumer electronics companies will have adopted some form of M2M by 2016, whether for new products, logistics or production.

Similarly, the report anticipates that 57 percent of healthcare and life sciences companies will have adopted M2M technologies by 2016.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...