Not every machine-to-machine or "Internet of Things" requires lots of bandwidth, or continual connection. But the connected car market likely includes a wide enough range of app requirements that Long Term Evolution, the highest-capacity mobile network, will lead growth.

Not every machine-to-machine or "Internet of Things" requires lots of bandwidth, or continual connection. But the connected car market likely includes a wide enough range of app requirements that Long Term Evolution, the highest-capacity mobile network, will lead growth.

“LTE will be the fastest-growing cellular technology in cars, expanding 135 percent annually between 2014 and 2018,” says Godfrey Chua, directing analyst for M2M and The Internet of Things at Infonetics Research. “A major boon will come from AT&T’s agreement with GM to deploy LTE for the OnStar service.”

Some service providers are seeing as much as 90 percent of their machine-to-machine (M2M) revenue generated from the connected car segment, Chua notes, and much of that opportuntity is, at present, centered in the United States.

North America accounted for 37 percent of global connected car service revenue in 2013.

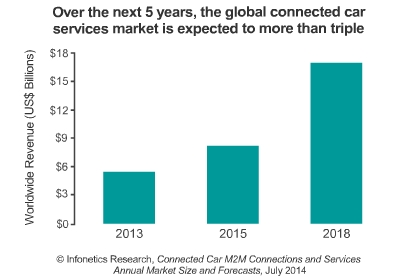

Infonetics also expects revenue derived by service providers for the connectivity and other basic value-added services they provide to the automotive, transport, and logistics segment to more than triple from 2013 to 2018, to $16.9 billion worldwide.

The connected car services market additionally is growing at a compound annual growth rate of 25 percent, nearly 21 times the growth rate expected for traditional mobile voice and data services between 2013 and 2018.

Whatever one believes about the size of the connected car market, and how big revenue opportunities might be for app providers, automakers and connectivity providers, it is clear that not every “Internet of Things” application and market segment has the same requirements for bandwidth.

Energy meters, for example, generally do not require persistent connections, and feature small uploads quite reasonably handled by 2G networks.

Video surveillance apps, on the other hand, generally require higher bandwidth.

Bandwidth required to support connected car apps will vary. Some diagnostic apps might well only require episodic, bursty, low-bandwidth connectivity. In-vehicle content apps, on the other hand, might well be required to support video, which means Long Term Evolution 4G is almost mandatory.

Real-time navigation apps might do fine with 3G access. Over time, of course, 2G networks will be phased out of service, so all apps ultimately will be available only on 3G or 4G networks.

For the moment, though, the differential app requirements mean “just about any communications service provider, whether they have 2G, 3G, 4G, LTE or a combination of technologies, can find a niche in the connected car space,” says Godfrey Chua,

Of course, since lower-bandwidth apps easily are handled by higher-bandwidth networks, LTE is likely to be a big winner.