Of total 2014 Comcast revenue of $68.8 billion, $44.1 billion, or 64 percent, was generated by the cable communications business. Operating cash flow contribution from the cable communications segment was about six percent.

About 37 percent of revenue was generated by the NBCUniversal segment, which grew about 7.5 percent, overall. Operating cash flow from NBCUniversal was about 18 percent.

The main point is that gross revenue and operating cash flow from cable communications is tough, from a growth standpoint.

The consumer part of the cable communications business (triple play services) is growing primarily because of high speed access.

Video revenue for 2014 was up about one percent. Voice revenue was static at about 0.4 percent growth. High speed access was where the gains primarily were made, with growth of 9.5 percent.

Business services contribute about nine percent of cable communications segment volume, at about $4 billion in 2014. But business services grew at a 22 percent rate in 2014. In fact, it might be correct to say the newest product segments in the cable communications segment (business services in general, and mid-market services in particular) have the highest growth rates.

Comcast estimates it has reached about 25 percent penetration of the small business addressable market, but only about five percent of the addressable mid-market opportunity, according to Neil Smit Comcast Cable president and CEO.

So mid-market revenue “is growing at a increasing rate relative to SMB,” said Smit.

In 2013, Comcast “had literally zero penetration in the mid sized sector,” said Michael Angelakis, Comcast vice chairman and CFO.

The point is that Comcast has seen the fastest growth rates for successive new products.

That suggests the possible upside from Comcast adding a whole new product line in mobile services, especially if Comcast can position the service first as a way for Comcast customers to view their content, but then secondarily as a way to use voice, messaging and mobile Internet access.

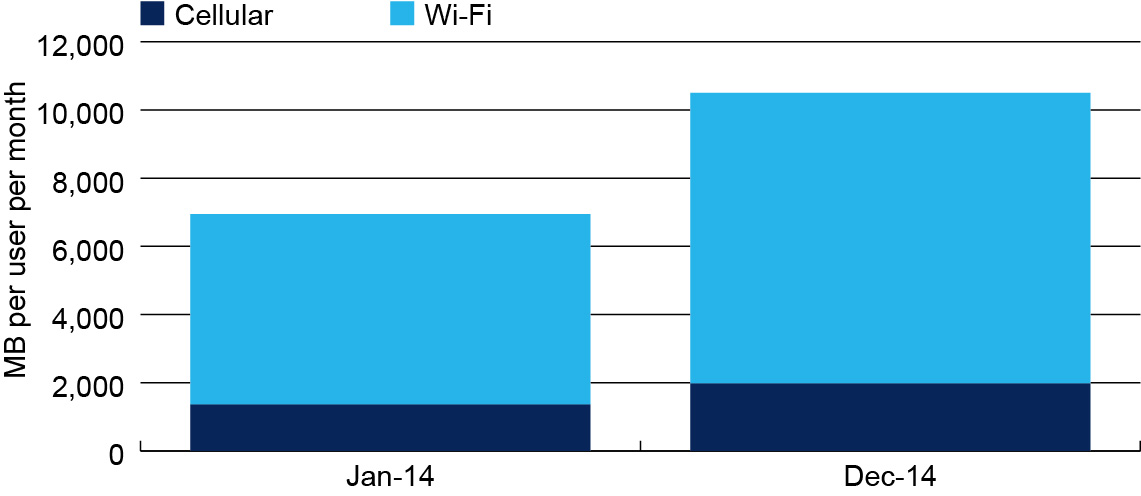

Commenting on capital investments Comcast has made in Wi-Fi infrastructure, the emphasis has been on support for the video business.

“The real goal has been that our customers can access their video any time anywhere whether in the home or outside the home,” said Michael Angelakis, Comcast vice chairman and CFO. “If Wi-Fi can also develop into a different type of service then that’s an added benefit to the Wi-Fi investment.”

But Comcast’s Wi-Fi network now includes 8.3 million hotspots, said Brian Roberts, Comcast Chairman and CEO. “We think we are working on how we monetize that asset and bring it to market.”

“As you know we have MVNO relationships with Sprint and Verizon,” Roberts said, hinting at ways mobile service could be offered, but with much traffic offloaded to the Comcast fixed Wi-Fi network.

Adding mobile service would not only allow Comcast to offer a full quadruple play, but also would add a brand new product line with proven customer demand, but allow use of the new Wi-Fi hotspot network to lower costs.