In the third and fourth quarters of 2014, perhaps 40 percent of cable TV network ratings declines were caused by consumers who watched over the topp subscription video services instead of the linear channels, according to the Cabletelevision Advertising Bureau.

Total TV viewing fell 10 percent year over year in the third quarter and nine percent, year over year, in the fourth quarter, according to Todd Juenger, Sanford C. Bernstein analyst.

In the first quarter (through February), linear video network viewing was down about 12 percent.

“We believe the U.S. television industry is entering a period of prolonged structural decline,” said Juenger.

Should those rates of decline continue, at least some channels will face pressure to reconsider their business models. That will be a tough challenge. Linear distribution has one huge advantage: it creates huge potential audiences for advertising.

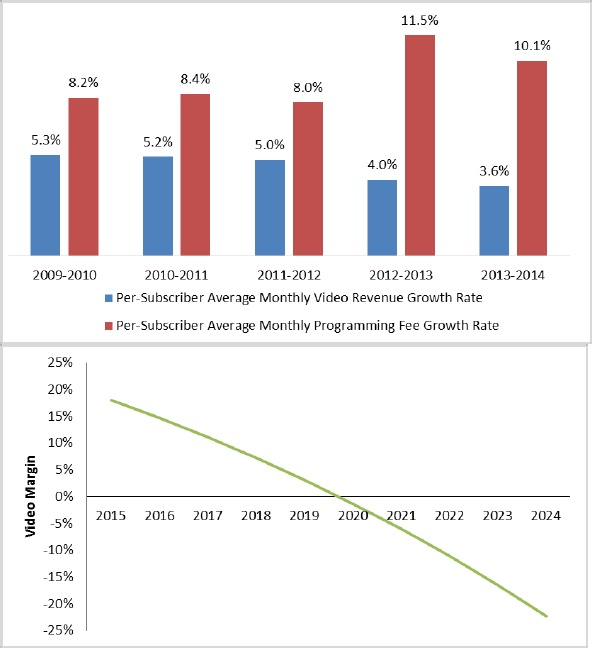

A la carte distribution will not carry such premiums. Most networks will find they simply cannot replace lost advertising revenues, in any switch to over the top distribution, by substitute subscriber fees.

The rough comparison is earnings of five cents to seven cents per viewer rather than 30 cents, on a much-smaller base of units, for the network.

The cumulative revenue shift would be catastrophic for most programming networks. Unbundling Analysts at Needham and Company have estimated that half of U.S. linear video ecosystem revenue would evaporate in any full shift to completely unbundled content access.

In other words, $70 billion in revenue would disappear. As a direct result, fewer than 20 channels would survive in an a la carte world where consumers are required to bear 100 percent of the cost of the content in the form of subscription or other fees, and advertising essentially disappears.

In 2012, the TV ecosystem generated total revenue of approximately $150 billion, about

$77 billion from advertising and $74 billion from subscription fees

paid to cable, telco and satellite distributors.

TBS, which historically was the second cable channel to be created, and the first ad-supported cable channel, generates about $1.5 billion of revenue from subscription fees plus $2 billion from advertising revenue, according to Needham.

Needham estimates that TBS charges distributors about $1.20 a month. Consumers might theoretically pay about $1.60 at retail, in a bundle. Nobody knows what TBS might cost as a stand-alone streamed channel, but something in the range of $5 to $10 is probable.

The reason is that TBS distribution costs would need to be covered, at the same time TBS loses much of its advertising and distributor revenue.

In a full a la carte regime, where channels are purchased as part of over the top Internet subscriptions, both revenue streams would be severely disrupted.

Networks would lose most of their subscribers and most of their ad revenue. The present TV ecosystem generally splits revenue 50-50 between content and distribution partners. The content provider generally earns 80 percent of all advertising revenue.

“Consumption of network and cable content is taking place in ways that allow viewers to circumvent high monthly cable bills, avoid watching commercials, or both. Every single one of

these changes represents a move to a revenue model that is less profitable than the one currently enjoyed by TV networks,” said analyst Gary Brode. “It is only a matter of time before the revenue and profitability of the networks begins to fall.”