The phrase has to be understood in context. It actually means a particular provider, with a particular cost structure and business model, cannot do something. A given retailer might not be able to compete with Amazon, in some product lines. A given airline might not be able to compete with another airline at a specific airport location.

But it is not true that what one firm cannot do means that all other firms are similarly unable to do so.

In fact, some have argued, for some time, that U.S. cable TV companies eventually would emerge as the dominant fixed line suppliers of communication services for consumers, as telcos--with higher fixed and operating costs--simply could not compete.

In many ways, that already has happened: telcos no longer are dominant providers of fixed network services for consumers.

At the end of 2012, incumbent local exchange carriers (telcos) had 34 percent share of the consumer voice market, 14 percent of the high speed access market and 10 percent of the video subscription market.

In fact, some might argue that cable TV operators are destined to dominate consumer high speed access. Others might argue a long-term duopoly, nationally, will exist, with Comcast and AT&T having dominant market share in different markets.

Some might argue that AT&T and Verizon have cost structure issues that will continue to hamper their fixed network operations. That is one good reason why effort and investment have shifted to mobile operations.

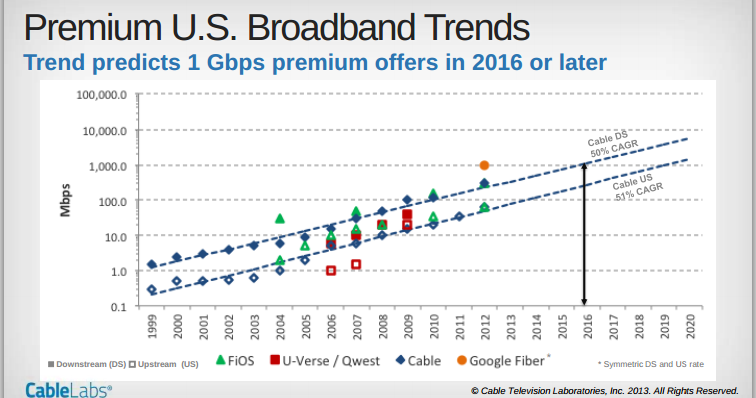

Telcos might not be able to match Comcast’s 2 Gbps high speed access offer easily, as they will find 1 Gbps challenging on a sustainable basis. The issue is the business model, not the technology. In competitive markets, the low-cost provider tends to win Telcos are almost never the low-cost providers.

There are obvious regulatory and business implications, almost certain to be jarring and unpleasant.

There will come a time when it makes no sense to put handcuffs on formerly dominant telcos. There will come a time when telco cost structures will have to be slashed even more than at present.

Telco fixed network investment returns will be difficult to impossible to obtain.