Perhaps there are instances where government policies can both stimulate competition and investment. That arguably was the case when the Telecommunications Act of 1996 was first passed, for example, legalizing competition in U.S. local access markets that had been sanctioned local monopolies until that point.

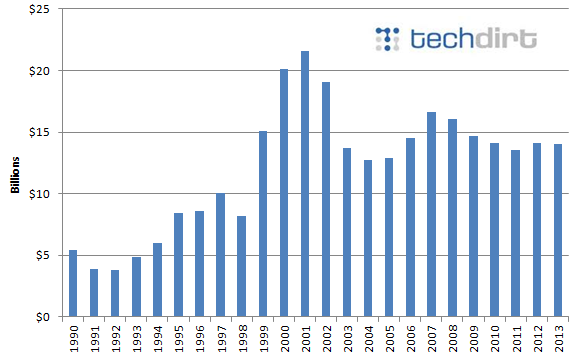

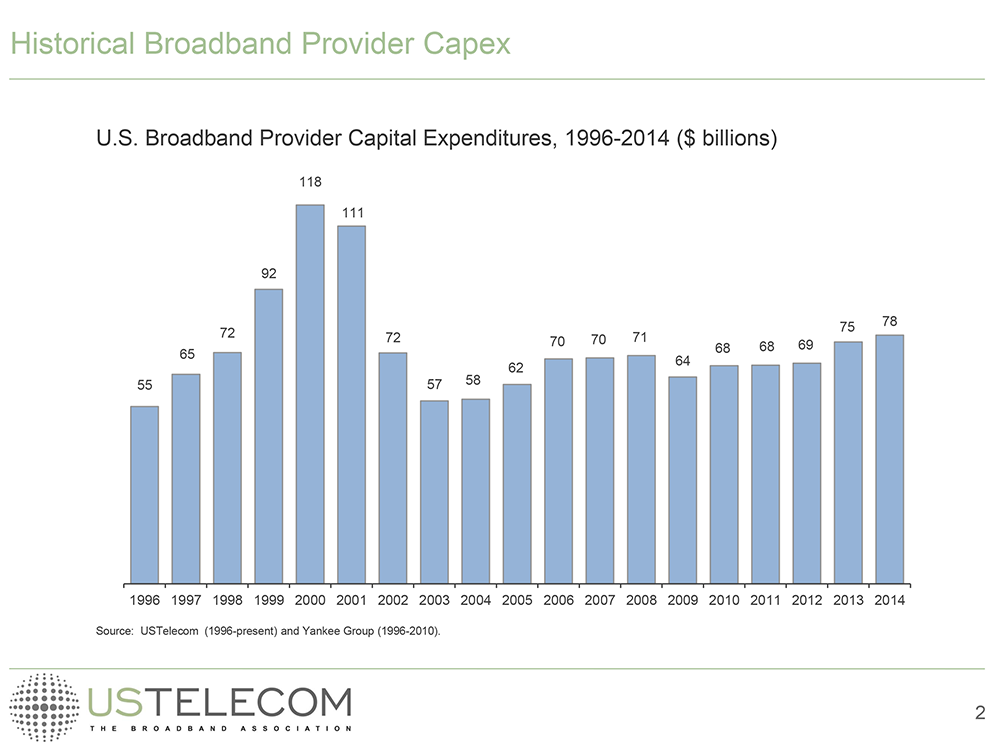

As a historical matter, investment climbed at the same time as competition bloomed. Looking at cable TV capital investment, there was a huge run-up in investment after the Act was passed allowing cable TV companies to create new roles as the most-significant new providers of consumer voice and Internet access services.

After reaching a peak, investment later declined to levels that are generally higher than previously had been made. In that sense, an argument can be made that both competition and investment were enhanced, over the medium to long term.

On the other hand, one might also argue that the higher levels of investment have little to nothing to do with legacy services, and everything to do with new services that might, or might not, have been dependent on the Telecom Act.

It is plausible, perhaps even certain, that investment levels were hiked to support new revenue streams based on the Internet, and had nothing to do with the deregulation of voice services.

In other instances, policymakers often face tougher choices. Policies that promote competition might increase investment in the short term, but also might depress investment in the long term, if investments in a specific industry consistently lag investments elsewhere.

In other words, whatever the near term impact of any policy decision, long term investment will flow to where firms believe returns are higher, and decrease in any areas where companies believe returns will fall, or are slim and in danger of reaching zero.

Something along those lines seems to be happening in India, where the Department of Telecom (DoT), to preserve competition, has decided to maintain existing rules about the maximum amount of spectrum any single provider can use.

Those rules will prevent several of the larger mobile service providers from rationalizing their spectrum holdings in ways that lead to lower costs.

The DoT decision means larger telcos will not be able to share spectrum, or trade spectrum.

Under the existing rules, a telecom operator cannot hold more than 25 per cent of total spectrum assigned to all companies in a circle and over 50 per cent of total spectrum assigned in a particular frequency band.

To be sure, the ultimate impact on investment is not entirely clear. Service providers always have multiple tools for increasing capacity, and one way to do so is to build more cells, with smaller coverage radius.

Prevented from adding more spectrum by trading or sharing, service providers might well be forced to invest in additional cell sites. On the other hand, service providers might conclude the faster route is to buy out competitors, thus adding their networks and spectrum. That might mean less investment in new facilities, but also less competition.