It always is difficult to predict the likely growth of the mobile payments business.

In part, that is because there are different mobile payment segments; mobile payment revenue for providers is distinct from transaction volume, the number of suppliers is quite fragmented and the actual revenue for payment system suppliers is quite variable.

Aside from all that, even successful innovations in the financial services business can take quite some time to get traction. In the case of mobile proximity payments, the issues range from the base of active devices able to support specific mobile payment systems to retailer adoption of the services and terminal deployments.

|

| source: the financial brand |

All of that adds up to a huge challenge for the various payment system contestants.

Nor is it clear what transactions will make most sense, for most people, based on which services are supported at the venues they frequent, and the types of purchases where using proximity payments makes the most sense.

According to the latest proximity mobile payments forecast from eMarketer, the total value of mobile payment transactions in the US will grow 210 percent in 2016.

In 2015, mobile payments transactions will total $8.71 billion in the United States, with users spending an average of nearly $376 annually using their mobile phone as a payment method.

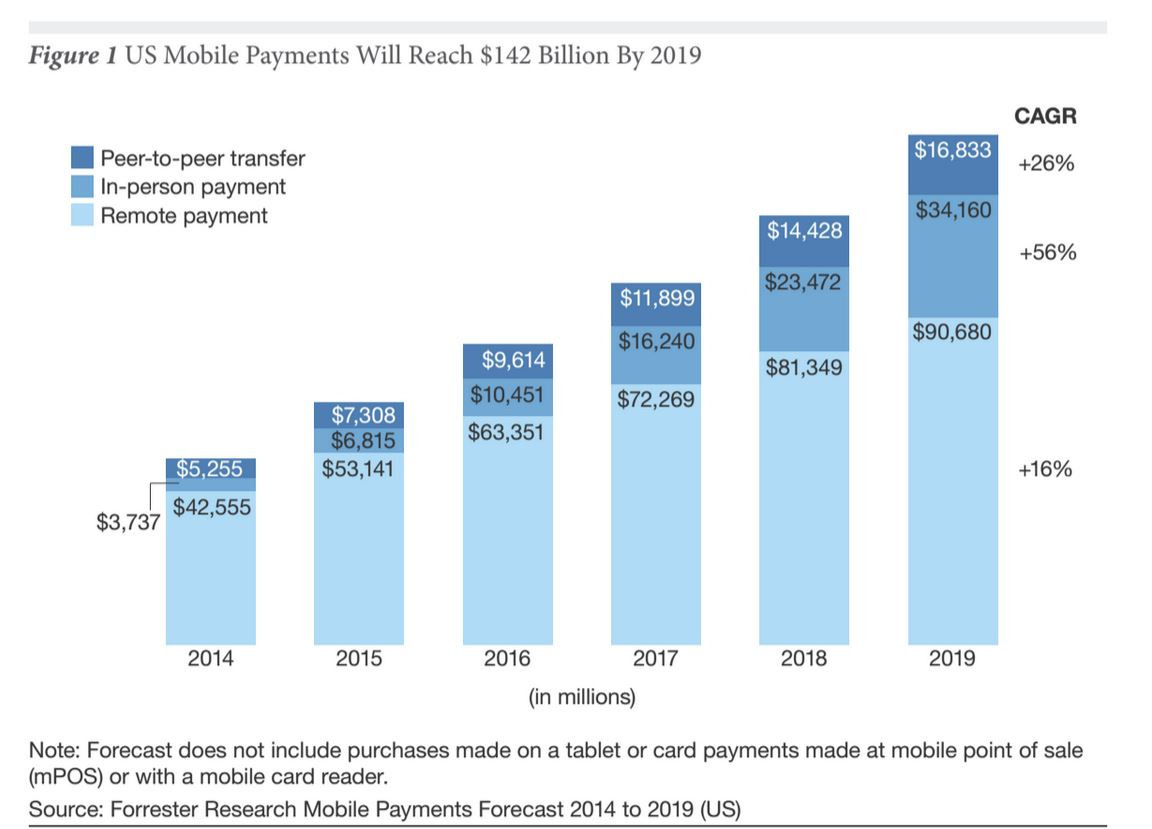

By way of comparison, other forms of mobile payment or mobile banking represent far larger transaction volumes. In 2015, for example, more than $53 billion in remote mobile payments will be made.

By 2016, total mobile payment transactions at retail locations are estimated by eMarketer to reach $27.05 billion, with users spending an average of $721.47 annually. By 2016, according to Forrester Research, about $63.4 billion in remote mobile payments will occur.

There will be 23.2 million people in the United States using proximity mobile payments in 2015, eMarketer expects. By 2016, that will grow to 37.5 million.

There will be 23.2 million people in the United States using proximity mobile payments in 2015, eMarketer expects. By 2016, that will grow to 37.5 million.

“Mobile wallets like Apple Pay, Android Pay and Samsung Pay will become a standard feature on new smartphones,” said eMarketer analyst Bryan Yeager. “Also, more merchants will adopt point-of-sale systems that can accept mobile payments, and incentives like promotions and loyalty programs will be integrated to attract new users.”

eMarketer defines proximity mobile payments as point-of-sale transactions that use mobile phones as a payment method, via tapping, waving and similar functionality.