The most important numbers in most mobile service provider markets are “three” and “four.”

Three tends to be the number many believe provides both competition and sustainability, while four is the number policy advocates and government regulators prefer, primarily because four contestants are believed to provide more robust levels of competition.

The Shaw Communications acquisition of Wind Mobile Corp., despite Wind’s small market share (about three percent) means there will be four national wireless carriers, all backed by four big national telecom conglomerates, instead of just three.

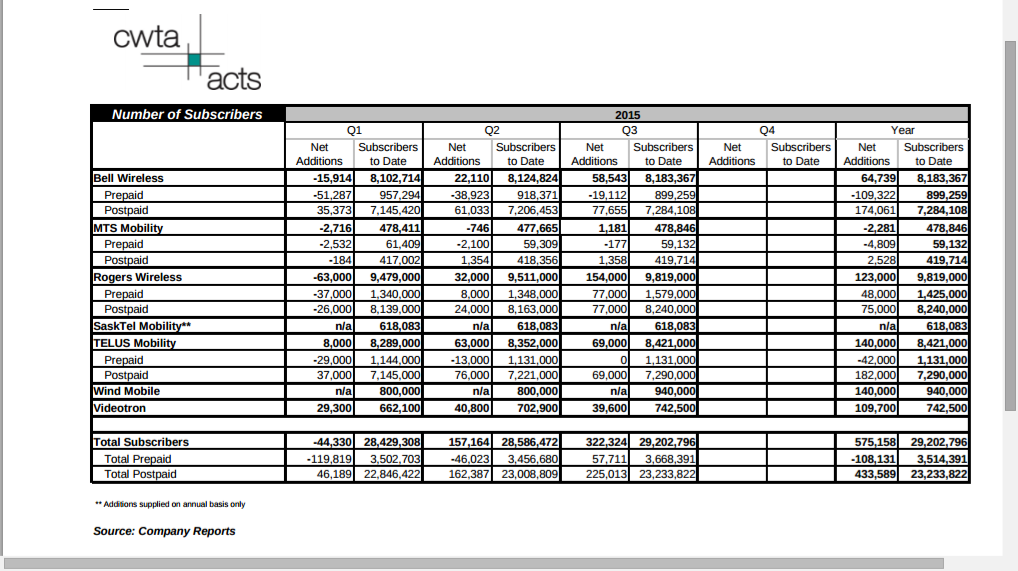

Wind says it is Canada's largest non-incumbent wireless services provider, serving approximately 940,000 subscribers across Ontario, British Columbia and Alberta with 50MHz of spectrum in each of these regions.

Wind has yet to begin building a fourth generation Long Term Evolution (LTE) network, so that undoubtedly will be on the agenda, as Shaw prepares to step up competition with the leading mobile providers in Canada.

Though Canadian regulators recently had used a familiar tactic--creating spectrum reserves for new and upstart providers--some would argue that no meaningful change happened.

In March 2015, Wind Mobile Corp., Videotron Ltd. and Eastlink Wireless won significant blocks of AWS-3 (advanced wireless services) spectrum covering most of the country for a combined total of less than $100 million, while Telus Corp. and BCE together will spent about $2-billion for the licenses they won.

The new entrants paid an average of 11 cents per megahertz per person (MHz-Pop)

Telus paid $3.02 per MHz/Pop and BCE paid $2.96 per MHz/Pop.