One rather frequently hears assertions that U.S. Internet access prices are “too high,” or “the highest in the world,” or “among the highest in the world.”

As often is the case with statistics, “truth” and “facts” diverge. The problems start with price levels across countries. It would be easy to make a case that prices for virtually any product or service are “high” in the most-developed countries, compared to prices for those same products in a developing country.

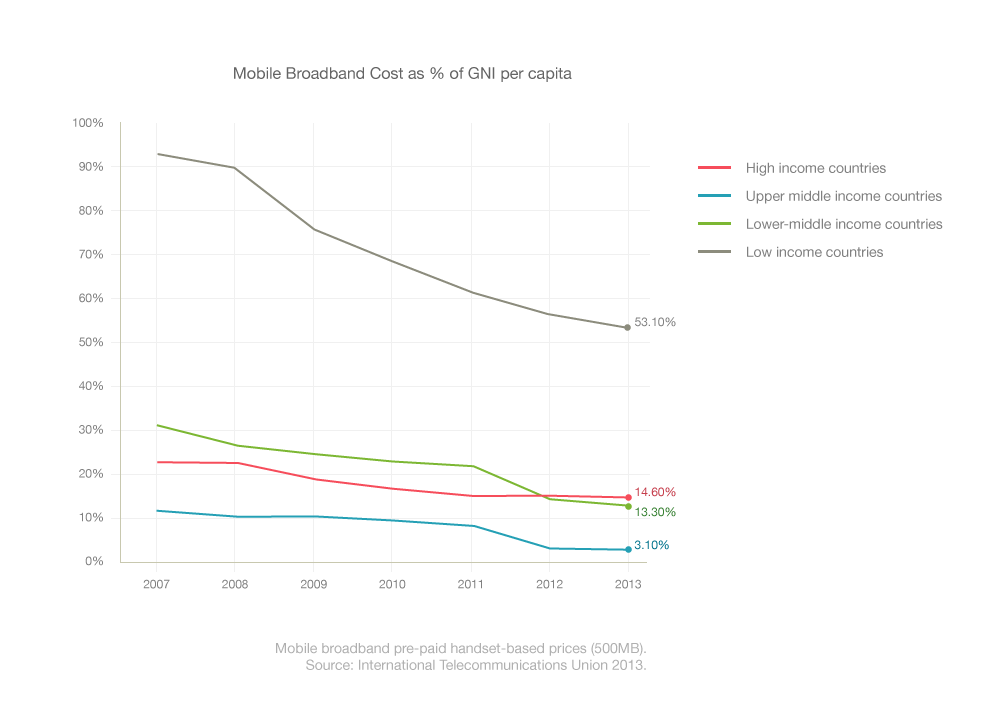

That is why global comparisons require normalizing prices.

There are a couple of standard ways of doing so. “Purchasing power parity” is one such technique. Expressing the “price” of any product in relation to household income, or per capita income, is another way of doing so.

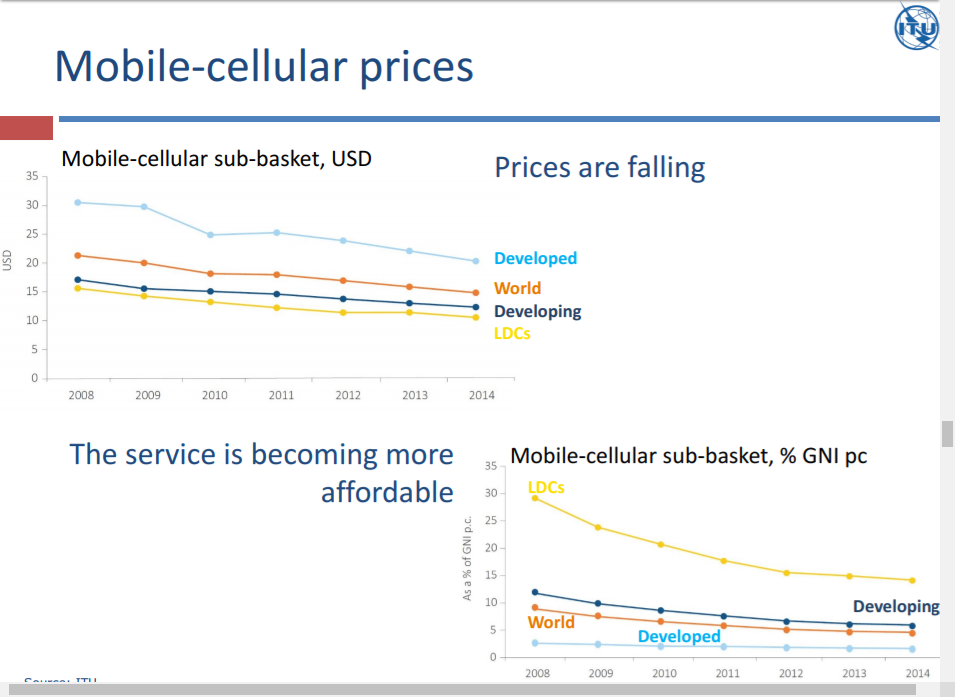

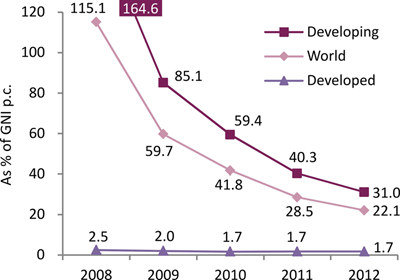

Using such mechanisms, it is clear that prices can be “high” in developed countries even if “cost” is low, in terms of the percentage of income required to buy a product.

In other words, the “cost” to buy mobile or Internet services in developed countries actually is quite low.

There is a further complication when assessing price and cost as a function of “people” rather than household income, since households vary in size, from place to place.

In other words, price per person can vary with the number of persons per household, the number of people using a product, or the degree of sharing possible with any product. “Price” or “cost” also can vary based on the ways people buy those products (which plans are most often purchased, for example), as there are any number of ways a “bulk discount” can be applied, such family plans.

The point is that although retail prices in developed nations can be “high,” the actual cost, as a function of overall price levels and compared to income, typically is quite low, where it comes to either mobile or Internet access services.

Nor do such metrics always include a “quality” dimension. Value is determined not only by retail price, or price as a function of income, but also by the speeds and other attributes of usage plans. Price per megabit, in other words, also matters.

Paradoxically, "price" can be high, while "cost" is quite low.