By 2020, mobile will account for more than half of all of Internet access revenue in more than 75 percent of countries, researchers at PwC now predict.

By 2020, mobile will account for more than half of all of Internet access revenue in more than 75 percent of countries, researchers at PwC now predict.

Total global Internet access revenue will increase at a 6.8 percent compound annual growth rate, reaching global levels of about US$634.8bn in 2020.

Between 2015 and 2020, 13 countries, mostly emerging markets, will see double-digit revenue growth rates.

In sum, more than 1.3 billion people will start paying for mobile Internet access for the first time, bringing the total number of global subscribers to 3.8 billion.

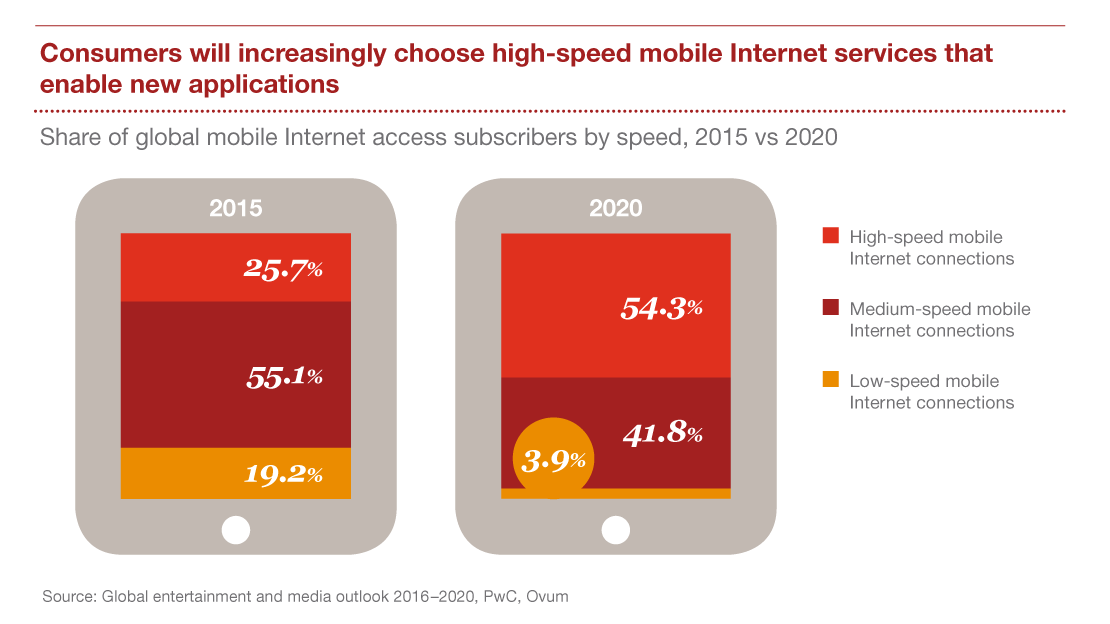

Just as important, by 2020, 54 percent of mobile Internet connections globally will be high-speed (delivering 30 Mbps or higher), while a further 42 percent will be capable of medium-speed service between 4 and 30 Mbps.

Also, note the on-going changes: Anything below 4 Mbps is “low speed.” Once upon a time, the classic definition of “broadband” was any access speed of at least 1.5 Mbps.

In some markets, such as the United States, 25 Mbps now is the minimum functional definition of “broadband,” where the Federal Communications Commission is concerned.

Be clear, the PwC forecast now predicts that 54 percent of mobile connections will operate at 30 Mbps or faster, by 2020.

Consumer behavior is likely to change quite substantially, as a result.

Mobile in the past has been speed challenged, limiting consumer experience. Higher speeds will mean that watching online videos, streaming high-quality music and making video calls on the move are more pleasant and reasonable operations.

As speeds increase, new applications like ultra-high definition video will gain traction, and operators will seek to retain customers by upgrading them for free or at low cost, PwC predicts.

So consumers will increasingly choose high-speed mobile Internet services that enable new applications. That point is among the most significant for “access providers.” Consumers always buy connections because they want to use apps.

That means networks must be built to support popular, high value apps that people and businesses want to use. In addition to requiring ever-higher speed requirements, the ability to “tune” networks to support popular apps will matter, one might argue.