It always has been difficult to offer the same types and levels of communications and some other services in rural and isolated locations, anywhere around the globe.

The reason mobile networks “solved” the problem of “people not being able to make phone calls” happened because we found a network platform that was less expensive than the fixed networks that were for many decades the only option.

Such platform economics explain why most observers believe mobile will be the platform that finally connects “most people” around the world to the Internet.

But we sometimes are reminded that even in developed countries, rural business cases remain very difficult. That, in fact, is why governments generally subsidize communications services in rural areas.

|

| source: techneconomyblog.com |

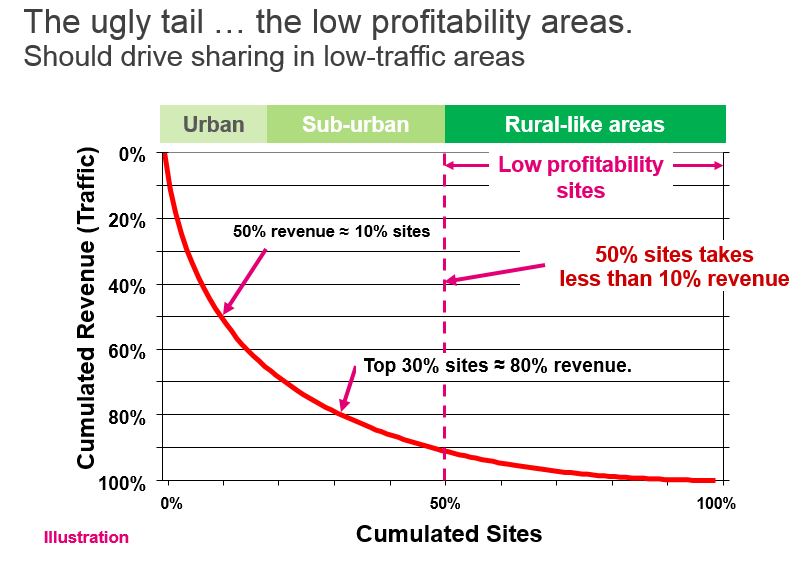

Less often do we think about the fact that even mobile networks have clear divergences in profitability from place to place. And even a mobile operator does not expect to actually recover costs--much less make an actual profit--from those cells that serve customers in very-rural and isolated areas.

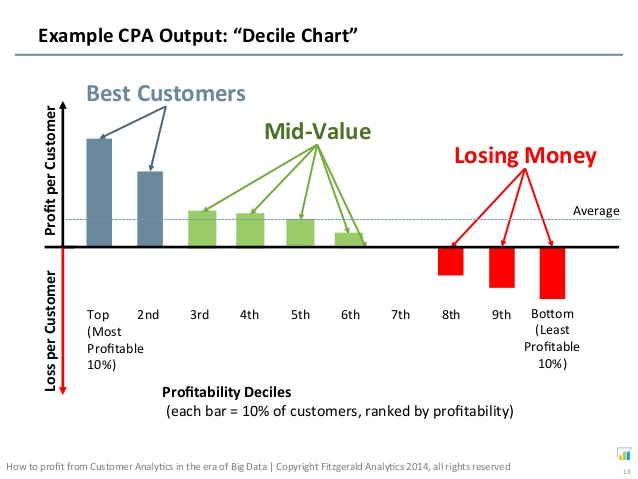

As likely is true in most industries, a disproportionate share of firm profits are generated by a relatively small number of customers, with likely losses among some customer groups.

That is one reason why new developments in access technology and platforms are so important: to sustain high-quality services and build new networks, we constantly must grapple with the likelihood that perhaps as much as half of locations actually are “money losers.”

That poses a key sustainability challenge for any operation that actually has to recover its costs and make enough profits to stay in business. In the mobile business, that “half the network doesn’t make much--if any--money” is a reality.

So if you think about it, that is a key problem for service providers and policymakers who actually want everyone to have Internet access. It might literally be true that most such networks, operating in rural areas with low population density, “will never actually make money.”

|

| Fitzgerald Analytics |

If so, only subsidies of one sort or another are going to enable universal Internet access, no matter how good our platforms are improving.

In other words, there might simply not enough demand in many rural areas to support new high-quality Internet access networks. There might not be enough people, willing to pay enough, to actually earn a return on rural access networks.

That doesn’t mean the networks will not be built. It simply means they will be operated at a loss, with subsidies coming from somewhere else. Government support programs likely will play a role. But profits earned in other parts of the ISP’s business are going to be equally--if not more--important.

That is why the business model for Internet access always is a key focus of the Spectrum Futures conference. Here’s a fact sheet and Spectrum Futures schedule.