|

| source: techneconomy blog |

Whether you look at revenue, profit or traffic, mobile network cells are not “equal.” Basically, a Pareto distribution typically holds: perhaps 80 percent of traffic is generated by 20 percent of total tower sites.

Looking at usage on a given day, by any single user, perhaps 80 percent of traffic is carried by just three towers. About half of traffic is carried by one tower. The remaining 20 percent of traffic is carried by 28 additional cell sites.

The implications are that some towers are highly profitable, others are self-supporting and some towers probably lose money.

|

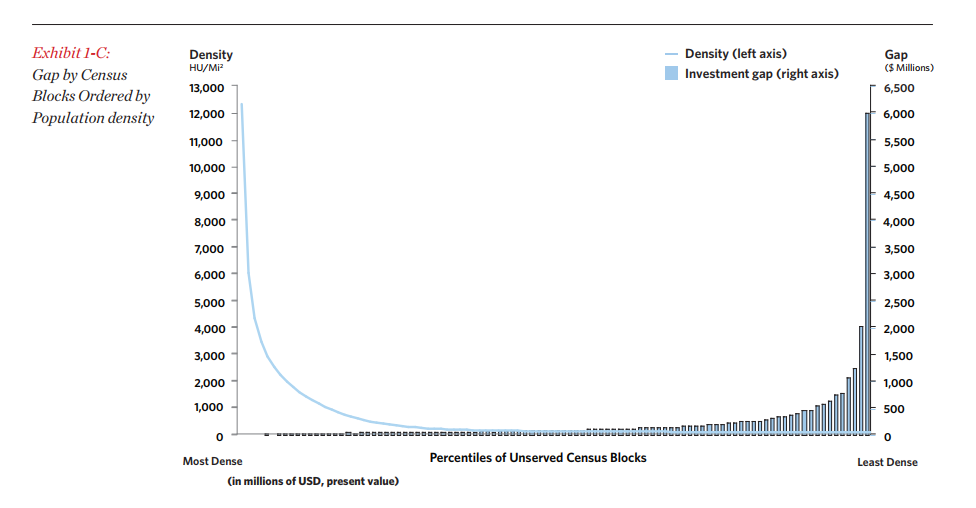

| source: FCC |

The traditional rule of thumb for revenue and profit for fixed networks in the U.S. market is that service providers make money in urban areas, break even in suburban areas and lose money in rural areas.

|

| source: techeconomy blog |

One way of illustrating the pattern is to note that population density and network cost are inversely related. An analysis by the Federal Communications Commission shows that the cost of networks, per location, grow dramatically as density falls.

Without subsidies of some types (governmental or internal subsidies by the service provider), rural area services likely are not possible.

Other studies of 3G network traffic in Western Europe suggest that 20 percent of the towers carry 60 percent of the 3G data traffic.