Historically, the reason telecom and information technology providers have used indirect distribution (channel partners) is because they cannot afford to sell direct, using internal sales forces.

The reason major service providers use mass media and retail channels to reach consumers has the same business drivers. Service providers cannot afford to sell direct to the mass market, and cannot actually rely on channel partners, either, as there is not enough revenue per account.

Retail stores, on the other hand, which generally are a form of direct sales--and more importantly a fulfillment mechanism--are necessary because few customers are completely comfortable buying devices “sight unseen.”

But as tier-one service providers continue to face a need to reduce costs, it is possible that reliance on channel partners for an increasing portion of overall sales efforts is possible.

The reason is drop-dead simple: as profitability becomes tougher, and aggregate sales volumes decline, “cost of sales” also must drop. Reliance on channel partners is one way to do so.

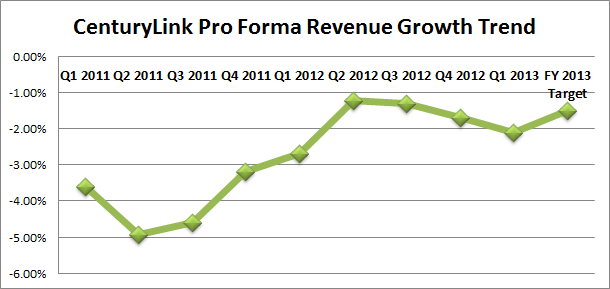

Consider recent developments at CenturyLink, which plans to lay off seven percent to eight percent of its fixed network workforce by the end of 2016.

CenturyLink revenue fell 0.7 percent in 2015 to $17.9 billion. Analysts project revenue will decline two percent in 2016, according to Bloomberg. So revenue is shrinking.

So CenturyLink--like any other business--has to match costs to expected revenue. “We all understand the pressure caused by the decline in our legacy revenues; it creates a $600 million negative impact on our business each year,” said Glen Post, CenturyLink CEO.

“While we continue to see positive growth in our strategic products, the profit margins of these strategic products and services are considerably lower than those associated with the legacy revenue we are losing,” Post added.

CenturyLink faces some of the same issues Frontier Communications an Windstream face. All are former rural fixed network telcos that grew and repositioned, in major ways, as business specialists.

But all three firms are fixed network only operators, in a market where mobile drives revenue growth in the broader market. None of the three firms own mobile revenue streams.

AT&T has become one of the biggest linear video providers in the U.S. market by virtue of its acquisition of DirecTV, and many believe the company will deemphasize fixed network linear video services in favor of satellite delivery.

So the big challenges include how to restructure their businesses for potentially-smaller gross revenues and lower profit margins in the mass market portions of their businesses.

Stranded asset issues are going to grow, as well, as fewer customers deliver revenue to support fixed costs.

So it is not a surprise that CenturyLink is trying to reduce its operating costs. It has to do so. A shift to greater reliance on channel partners would not be surprising, eventually.