Countries across South Asia and Southeast Asia need to make big investments in fixed network infrastructure, a new report by the International Telecommunications Union suggests.

In fact, the white paper suggests, it now is time to put the emphasis on fixed access networks, not the mobile networks that have, to this point, brought voice and moderate-speed internet access to people across much of the region.

To be sure, the paper tends to focus on backbone and “fiber to cell tower” investment, less clearly on ubiquitous fiber to the home. “The overall growth in broadband use (both mobile and fixed) significantly increases the requirements for backbone and backhaul bandwidth,” the report says.

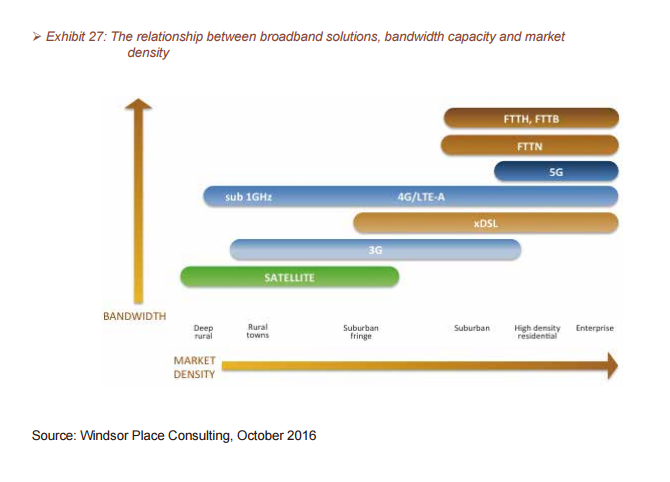

But the report also hedges, one chart suggesting that fiber to the home, fiber to the node and 5G all serve the same segments of the market. Some of us also would argue that some other obvious platforms are not mentioned in the report. Hybrid fiber coax and fixed wireless, for example, are absent.

The report suggests that the APAC8 nations (Bangladesh, Cambodia, Laos, Myanmar, Sri Lanka, Thailand and Vietnam) that are the focus of the white paper may benefit from a “leap to fiber” platforms. One presumes that means more than optical backbones and fiber to the cell tower.

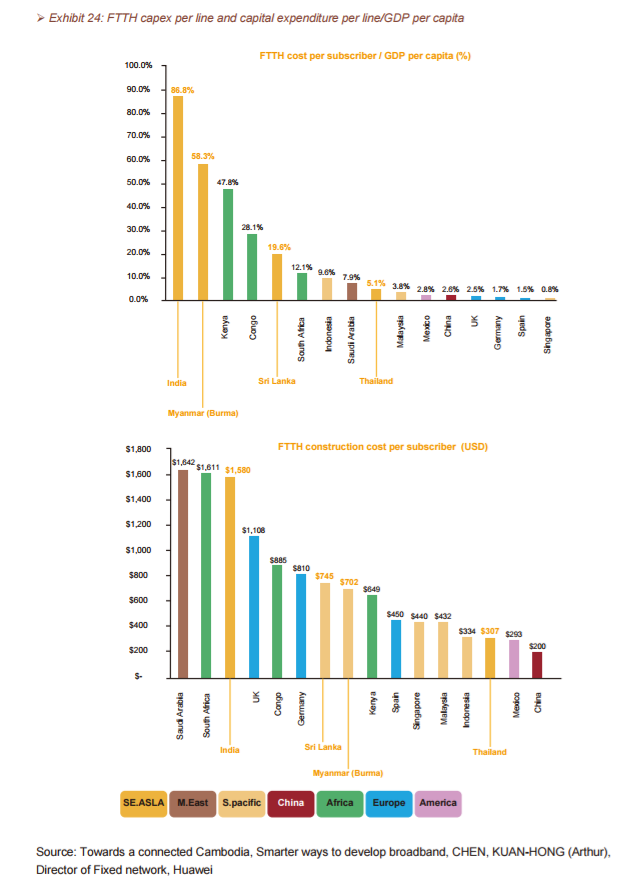

That might, in some ways, be a curious conclusion, given the high cost of fiber to home networks, in the South Asia and Southeast Asia markets, as well as elsewhere. Perhaps the ITU has various forms of platform sharing and wholesale in mind, for it does not seem as though facilities-based competition in the fixed network segment of the market will prove financially viable.

Much could ultimately depend on the adoption of 5G platforms. It is at least conceivable that multiple facilities-based mobile platforms, able to operate as fixed wireless platforms as well, will close a market opportunity for fixed networks, for much of the potential access market.