Global telecom service revenue declined four percent year-over-year in 2015 and likely will grow about one percent in 2016, according to Stéphane Téral, IHS Markit senior research director, mobile infrastructure and carrier economics. The good news is that revenue growth and capex are roughly in balance, at least on an aggregate global level.

Total global revenue of US$1.93 trillion will be drive by the Asia Pacific region, the world’s single biggest region, followed by North America, he says. Earnings (EBITDA) for smaller telcos often are less than one percent. For tier one telcos, EBITDA can reach 15 percent. Applying the higher 15 percent level produces global EBITDA of something less than $300 billion, compared to capex of about $340 billion.

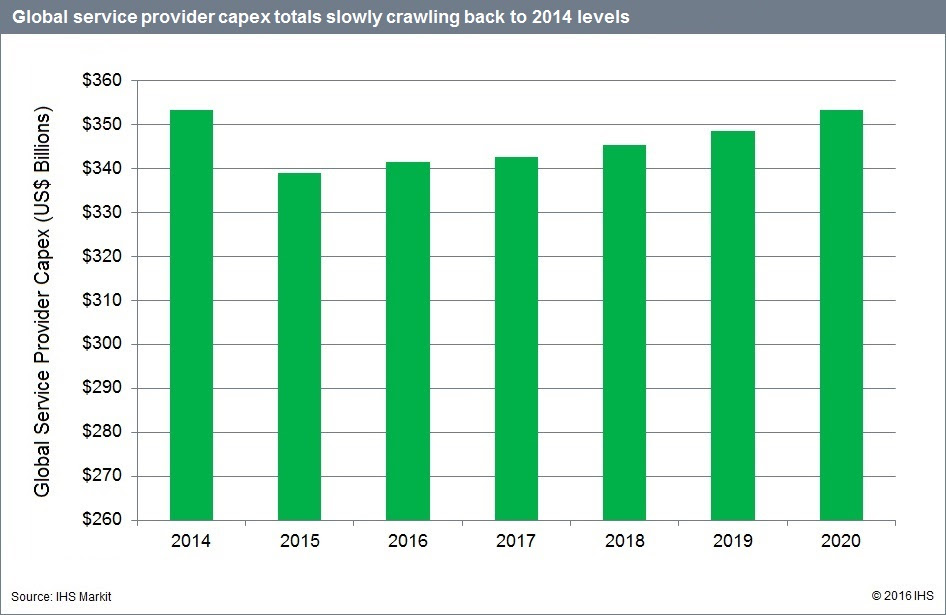

Global telecom capital investment will be mostly flat in 2016, with significant regional differences.

Low-digit growth in North America, Europe, the Middle East and Africa (EMEA) and the Caribbean and Latin America (CALA) will have been offset by a China-driven decline in the Asia Pacific region.

Asia Pacific, though, has become the world’s largest telecom spender and revenue contributor, says Téral.

Asia Pacific will drive 42 percent of global spending, while North America stays roughly even, followed by EMEA and CALA.

Global service provider capex will grow 0.7 percent to US$341 billion in 2016, with a significant boost in European fixed network investment.

Spending on every type of hardware equipment except wireless and time-division multiplexing (TDM) voice will grow in 2016. Software, on the other hand, will expand in double digits.