It is unusually difficult to predict how proposed mergers such as Sprint with T-Mobile US in the U.S. mobile market actually will affect innovation, competition, investment or profits, as other significant providers are entering the market, while the market itself is changing.

Sprint and T-Mobile US will argue that combining Sprint with T-Mobile US will make for a stronger competitor more able to press attacks on AT&T and Verizon. Others think less competition (price, features, value) will be the result.

Either could happen. An argument can be made that either Sprint or T-Mobile US, or both, lack the scale to compete effectively in the coming market. If so, sustainable competition by three firms is better than a duopoly. Empirically, some will argue, recent T-Mobile US suggests robust competition might even be sustainable, long term, in the absence of any mergers.

Some might also note that market entry by Comcast and Charter Communications is going to add more competition, no matter what else happens, so any consolidation among the biggest four firms will not eliminate future competition from emerging, though the immediate scale of such market entry is likely to be slight.

Also unknown is how competitor advantages might change, or be harmed, as market growth shifts to non-human users. It is at least conceivable that this shift provides a chance for one or more contestants to reshape the market.

That noted, “too much competition” is the problem that particular merger between Sprint and T-Mobile US is supposed to help fix. In other words, both those operators, and perhaps most observers, believe that such a merger will reduce price pressure and strengthen profits.

In other words, competition will lessen, not increase. In oligopoly markets there always is pressure to collude as much as compete. In the former scenario, firms really do not try to upset the market by launching price or value attacks to gain significant share, for example.

And oligopoly might be the ultimate fate of all telecom markets, fixed or mobile. That noted, competition still can happen.

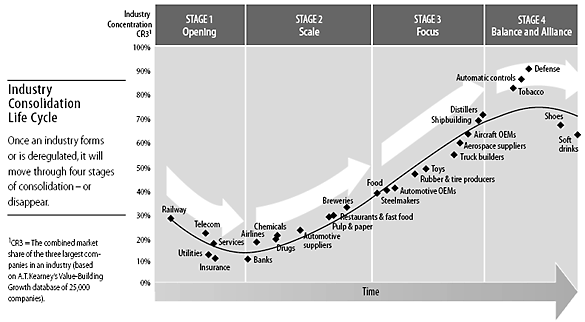

Still, the whole point of industry consolidation is to eliminate competitors, gain scale and boost profits, in part because ruinous price wars are avoided.

Though perhaps not the best example of an oligopoly, the U.S. airline industry now has consolidated to the point where profits actually are generated more consistently than in the past. Of course, that also means fewer flights, fewer seats and higher prices.

Firms still compete, but arguably less aggressively than had been the case. Still, even oligopolistic markets can be disrupted if consumer demand changes dramatically, or if sources of value shift dramatically.

There already is new evidence that re-emergence of unlimited usage mobile internet plans is affecting supplier profits.

The US mobile data services revenue had seen quarter over quarter growth for 17 straight years until the first quarter of 2017, for example, when growth went negative, notes analyst Chetan Sharma.

Cowen and Company Equity Research analyst Colby Synesael therefore notes that "new avenues of growth such as Mexico, content, media, IoT and 5G...can’t come soon enough."

Mike McCormack, Jefferies analyst, likewise notes that “the resurgence of unlimited plans...diminishes the ability to monetize growing data usage, removing an important lever of growth.”

Similar concerns are reasons why virtually all equity analysts favor mobile market consolidation. It is expected to reduce competitive pressures and allow price increases. The point is that equity analysts do not believe mobile market consolidation will, in fact, lead to more competition.