Product substitution has been a big trend in the global communications business, for decades. As customers have deserted fixed voice for mobile voice; over the top video for linear video, OTT messaging for carrier messaging, they might increase substitution of mobile internet access for fixed access.

Eventually, in business markets, large app and content providers might largely rely on their own networks for bit transport across wide area networks.

That is a bit ironic. Logically, cloud computing, which presupposes wide area communications, should underpin communications service demand. That arguably has been the case, historically.

What also is clear is that consumption of data only partially results in revenue benefits for access service providers. What is even more unclear is the eventual role of service providers in the long haul data business.

In the access realm, much of that consumption flows over Wi-Fi connections that generate no direct incremental revenue for access providers. In the transport realm, only some of the increase accrues to transport service providers, as the major content providers increasingly move most of their own traffic over their own global backbones.

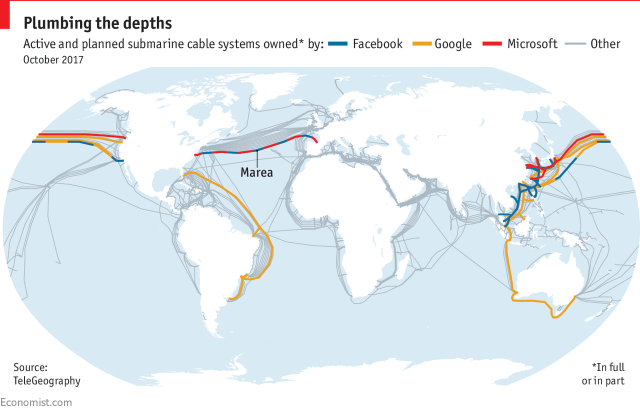

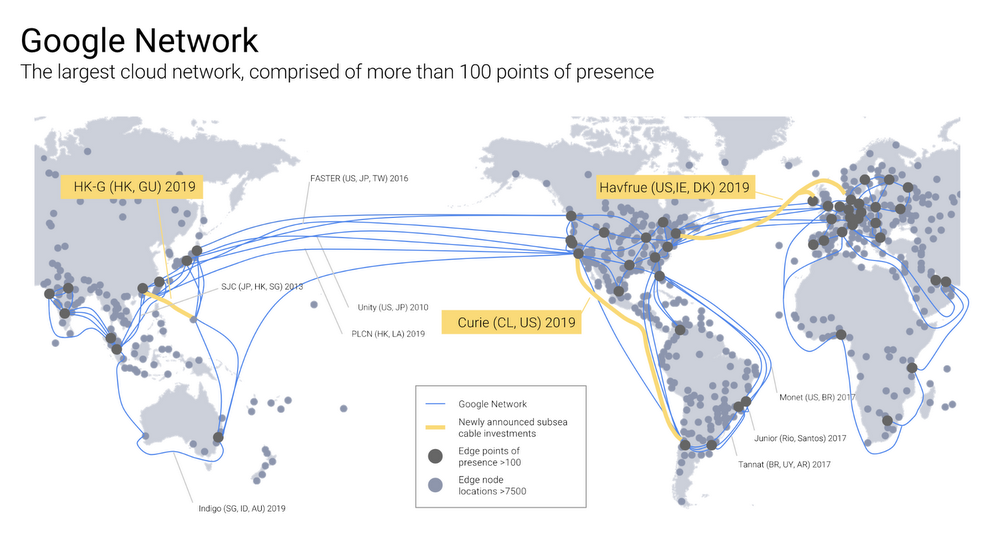

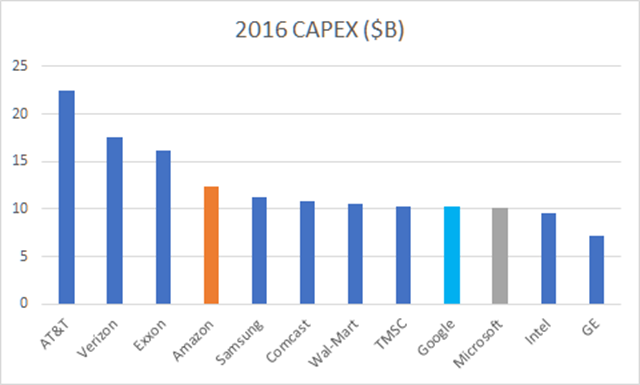

Google, for example, will build three new trans-oceanic optical cables in 2019. By some estimates, Google alone moves about a quarter of all global internet traffic across its own networks.

“Within the next 20 years,the whole concept of the telecom carrier as the provider of the network is going to disappear,” ” says consultant Julian Rawle. In other words, large app providers will replace telecom carriers as the leading suppliers of wide area network data transport.

Those trends should slow enterprise spending on telecom services, to the extent that the largest app providers now are the very firms driving global data transmission demand.

Worldwide IT spending is projected to total $3.7 trillion in 2018, an increase of 4.5 percent from 2017, according to Gartner. Notably, communications spending is predicted to grow 2.4 percent.That, however, is half the rate at which other information technology spending will increase.

Worldwide IT Spending Forecast (Billions of U.S. Dollars)

| ||||||

2017

|

2017

Growth (%)

|

2018

|

2018

Growth (%)

|

2019

|

2019

Growth (%)

| |

Data Center Systems

|

178

|

4.4

|

179

|

0.6

|

179

|

-0.2

|

Enterprise Software

|

355

|

8.9

|

389

|

9.5

|

421

|

8.4

|

Devices

|

667

|

5.7

|

704

|

5.6

|

710

|

0.9

|

IT Services

|

933

|

4.3

|

985

|

5.5

|

1,030

|

4.6

|

Communications Services

|

1,393

|

1.3

|

1,427

|

2.4

|

1,443

|

1.1

|

Overall IT

|

3,527

|

3.8

|

3,683

|

4.5

|

3,784

|

2.7

|

Source: Gartner (January 2018)

| ||||||

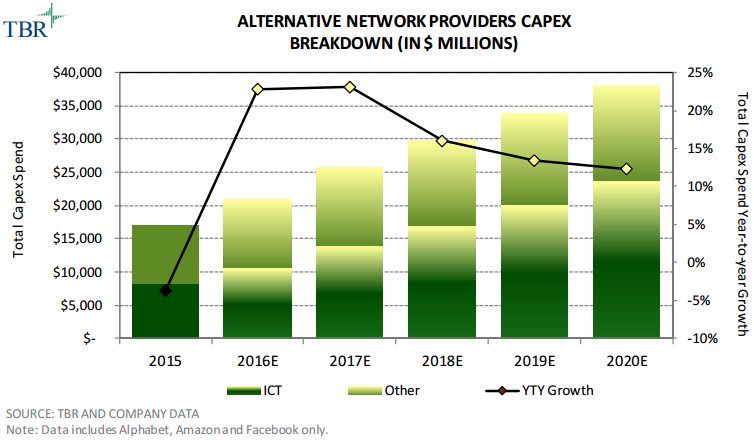

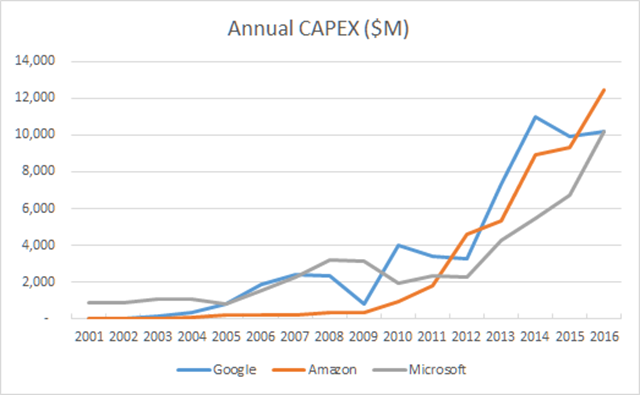

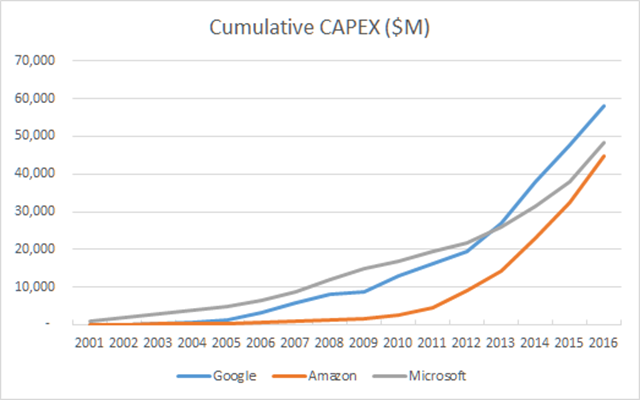

On the other hand, other trends are at work. Major app and content providers now build and own their own facilities. Google, for example, has invested at least $30 billion in its own infrastructure, including its own undersea networks. So, yes, cloud computing increases the role of communications.

Between 2015 and 2020, tier-one app providers are likely to double their spending on owned undersea facilities, for example.

Between 2015 and 2020, tier-one app providers are likely to double their spending on owned undersea facilities, for example.

On the other hand, large app providers now can justify the business case for building and owning their own transport networks.

Total telecom revenue in the 60 biggest markets to fall by two percent in U.S. dollar terms, to US$1.2 trillion in 2018, according to the Economist Information Unit.

Projects in digital business, blockchain, Internet of Things (IoT), and progression from big data to algorithms to machine learning to artificial intelligence (AI) will continue to be main drivers of growth, Gartner predicts.

Enterprise software continues to exhibit strong growth, with worldwide software spending projected to grow 9.5 percent in 2018, and it will grow another 8.4 percent in 2019 to total $421 billion.

The devices segment is expected to grow 5.6 percent in 2018.