It is quite fair to note that the 5G business case is a work in progress. That is to say, nobody can be quite sure how well suppliers of 5G services will be able to generate significant incremental revenue, beyond “more bandwidth.”

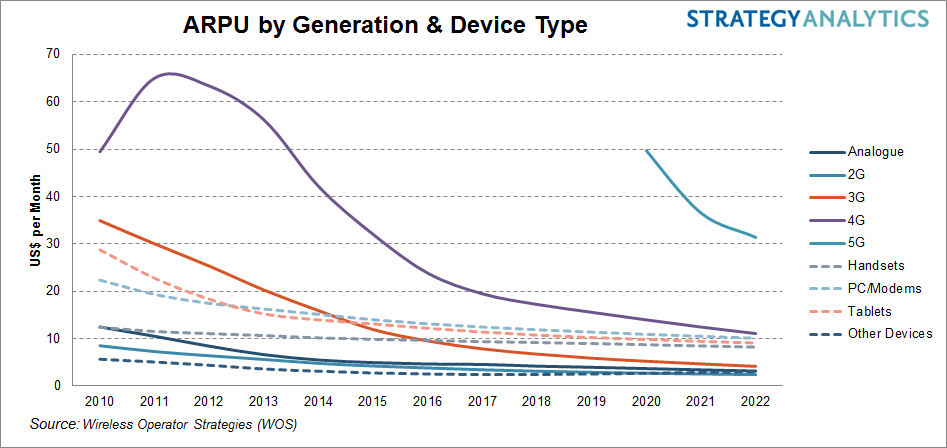

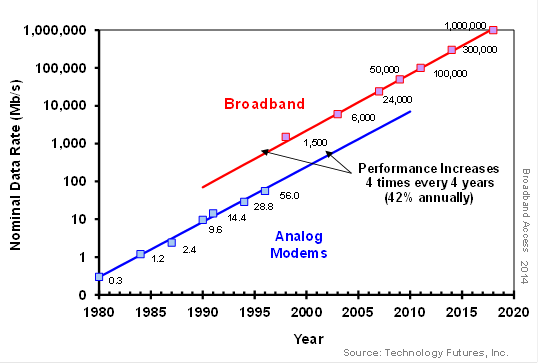

It is true that end users consume more bandwidth every year, and every decade, and that supply (typical consumer network internet access speed) increases about 42 percent every year.

The question is whether internet service providers can monetize that usage, since capacity increases grow faster than incremental revenue. “New technologies mean declining prices, even as capacity grows,” notes Armand Musey, Summit Ridge Group founder.

In other words, if supplying 10 times more bandwidth means 10 times more capex, is there a business model, Musey asks. Beyond that, with use of new untethered and wireless access using unlicensed spectrum, especially indoors, is it at all clear that mobile operators are even the eventual suppliers of most of that bandwidth, asks consultant Bob Horton.

On the other hand, notes Zayo Technologies CTO Jack Waters, technology costs have dropped by orders of magnitude over past decades, so capex requirements per new unit of capacity are not linear.

Still, notes Kalpak Gude, Dynamic Spectrum Alliance president, who pays? In other words, what is the business model for any of the coming next generation networks? “Much of 5G sounds like internet of things, and IoT is mostly going to use fixed access,” Gude argues. “Where’s the value?”

But 5G arguably is different in several ways. It will be the first mobile network generation where incremental revenue will come from non-human customers. And though some remain skeptical, 5G is viewed at AT&T as a replacement or substitute for the fixed network.

In fact, the 5G use case Randall Stephenson, AT&T CEO is “most excited about is the opportunity to have nearly, a nationwide broadband footprint and it could be a fixed line replacement.”

Of those attributes, it is the nationwide, gigabit everywhere angle that is most strategic. Up to this point, though mobile operators have had nationwide coverage, no provider of fixed network services has been able to reach more than a fraction of U.S. households and business locations.

For the first time, 5G means firms will have the ability to reach most customer locations with gigabit internet access speeds, on networks that will take only a few years to build, not decades. Also, regulatory barriers have prevented any fixed network firm from trying to reach nearly 100 percent coverage of consumer locations.

“The capacity is there, the performance is there, there's going to be full gigabit throughput,” Stephenson says.

As you would expect, given the lack of 5G handsets, fixed or nomadic applications and internet access are going to be the earliest-possible opportunities, as was the case for early 4G.