As the old adage implies, people are “entitled to their own opinions, but not their own facts.”

So it is that historical evidence for consumer internet access “price gouging” is virtually impossible to find in the U.S. market, over the past two decades, when internet service providers have--for all but three years--been able to charge whatever the markets would bear.

In fact, improvements in product quality (bandwidth, for example) have been made almost at Moore’s Law rates. And prices broadly have dropped, in absolute terms as well as relative terms, without considering inflation adjusted prices or product changes.

Impressionistically, recall only that some of us who were buying “broadband” internet access before the turn of the century were paying hundreds of dollars a month for 756 kbps service. Today we are able to buy 100-Mbps service for $50 to $70 a month, on a standalone basis.

In fact, because the internet access actually is part of a bundle, the imputed cost of 100-Mbps fixed network internet access might be less than $50 a month.

And since many of us buy mobile bundles as well, the cost of 15 Gbytes of monthly usage, per device, might be about $30 a month, per device. That is less money than we used to spend, for smaller usage buckets.

People with shorter experience of internet access prices might not understand the price declines.

Consumers who do not consider the changes in volume or the actual discounts on the products they actually buy might not be so aware of the price changes.

But assume one argues typical posted retail prices have climbed over the last decade or so. Ignore for the moment the fact that the “product” itself has changed, climbing from less than 1 Mbps to 100 Mbps to 300 Mbps for standard products.

Even there, one can argue that the increase in retail prices has been less than the overall level of consumer prices. In other words, internet access posted retail prices have increased less than the general level of prices.

The argument that ISPs are oligopolists whose behavior “harms” consumers because prices are higher than they ought to be, and service quality lower than it ought to be, is not borne out by the historical record.

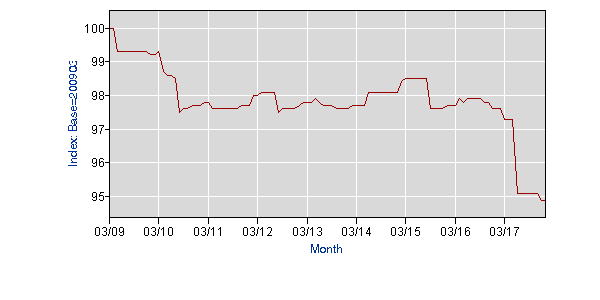

According to the U.S. Bureau of Labor Statistics, for example, between 2009 and 2017, the producer price index (PPI) for “telecommunication, cable, and internet access services” shows that prices actually dropped, and dropped fastest in 2017.

What makes this data even more noteworthy is that it includes “cable TV” subscription services, which everyone agrees climb every year, at rates above the background rate of inflation generally.

So if cable TV prices rise every year, the only explanation for declining prices for the whole basket (telecom, internet access and video) is that telecom and internet access prices dropped even more than cable TV prices rose.

Producer Price Index

Telecom, Cable TV, Internet Access

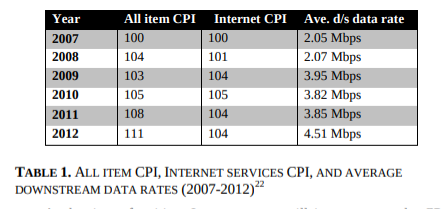

Likewise, as consumer prices have increased (from 2007 to 2012, for example), the cost of internet access increased less than the overall CPI, even as product quality (measured in terms of speed) increased.

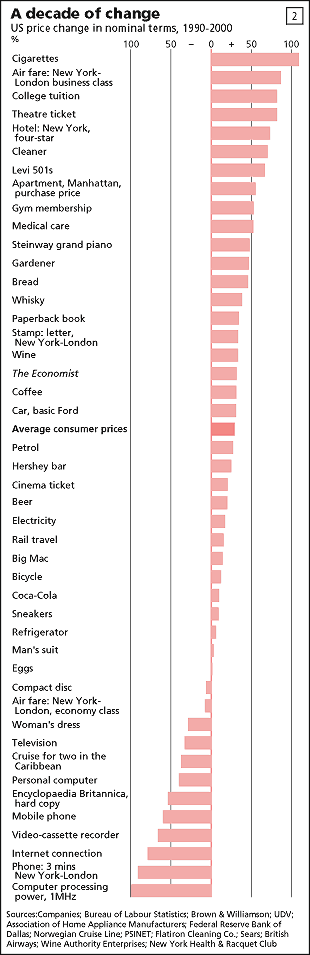

In earlier periods, such as 2000 to 2009, we see the same trend: U.S. internet access prices dropped about 80 percent, according to the Economist.

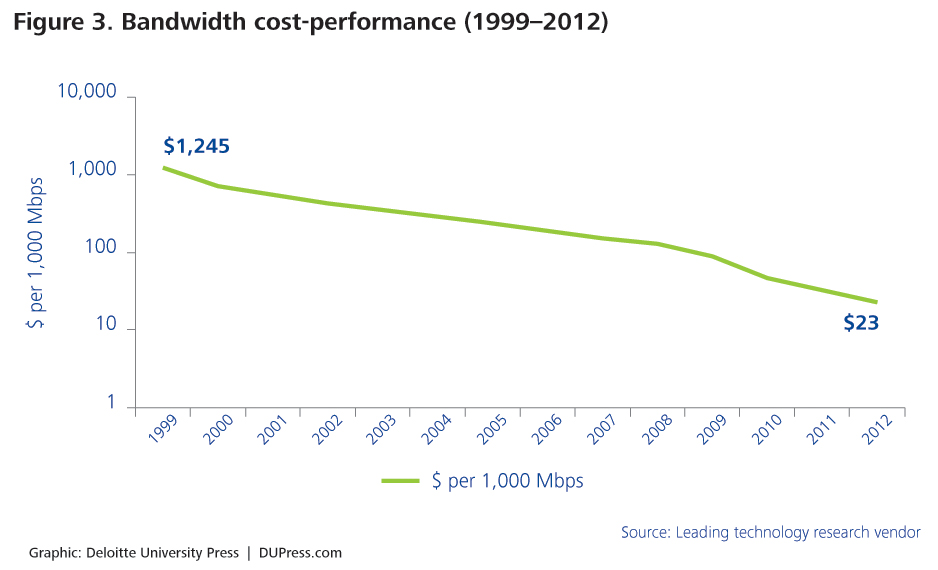

Looking at cost per bit, since 1999, cost has dropped by two orders of magnitude (100 fold).

Historically speaking, U.S. retail internet access prices have dropped, not risen, over the past two decades, on a cost-per-bit basis; compared to the consumer price index or other inflation-adjusted terms.

Some of the price declines are hidden, as consumers have shifted to bundled products, not standalone products, where prices are effectively discounted, even if standalone retail prices grow.

Finally, the product itself has changed. We now routinely buy services that are two orders of magnitude better, at prices four to six times cheaper.