Where facilities-based fixed communication networks compete, business models always are contingent on market share. Where just two equally-skilled and financially-endowed contestants face each other, it is reasonable for each competitor to expect take rates of 50 percent, on a network that passes every location.

That strands half the invested capital in the access network. In practice, since adoption is never 100 percent, the addressable market theoretically is less than 50 percent for each supplier.

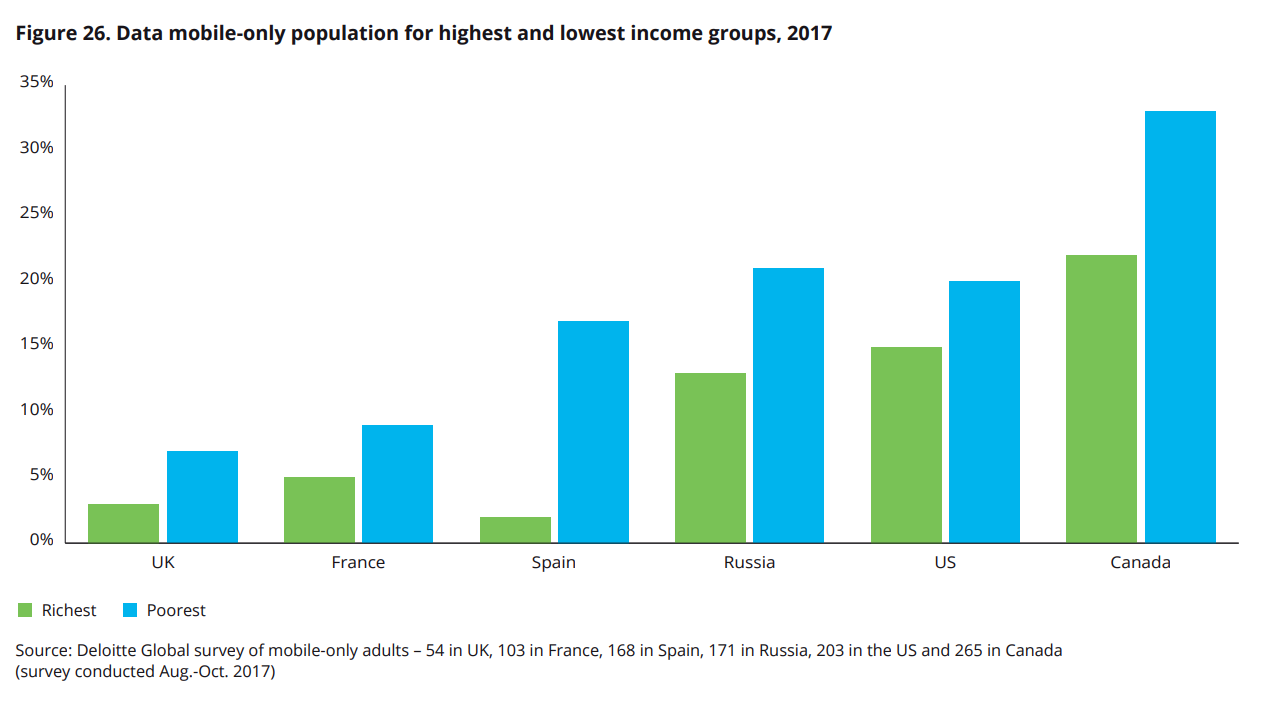

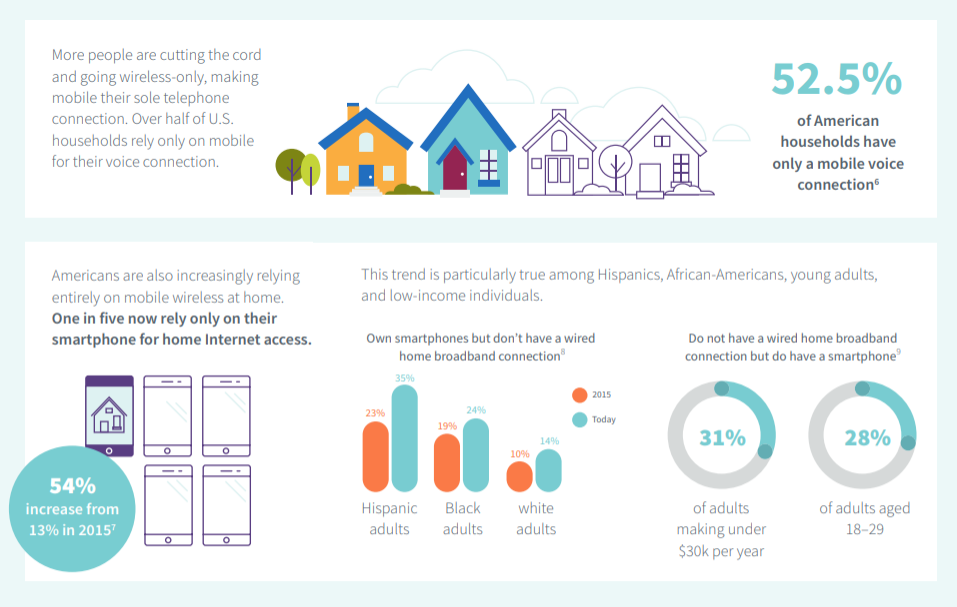

Additional competition reduces the potential market share yet further. In the U.S. market, some 20 to 30 percent of households already are mobile-only for internet access, reducing the potential share for two competitors to no more than 40 percent each.

Mobile substitution also will, in the 5G era, vastly complicate the fixed network business model. “The distinction between fixed networks and mobile networks is increasingly being eroded,” the report says. “In some places 5G could provide a more cost effective way of providing ultra-fast connectivity to homes and businesses.”

Such substitution already has happened for consumer voice, and consumer internet access and subscription video are the next big areas of potential shift.

That poses further threats to the fixed network business model, as potential market share will will even further in the direction of mobile platforms.

Wholesale customers on the Openreach network include Sky (24 percent share), TalkTalk (12 percent) and smaller providers. There also are some facilities-based providers operating on a localized basis.

Virgin Media is the primary facilities-based competitor and has 20 percent market share, while passing a bit more than half of U.K. households. It might not be unreasonable to argue that Virgin will be the first operator to offer gigabit internet access at scale, as a disproportionate share of UK. customers with faster speeds are on the Virgin network.

Housing density is the other key variable. About a third of U.K. households are in areas dense enough that as many as three competing gigabit networks can be built. That logically includes the Openreach, Virgin Media and one additional competitor on a local basis.

Perhaps half of U.K. households might be in areas dense enough that two gigabit network providers can survive.

About 20 percent of homes are in low-density areas where only a single network is likely to be possible (subsidized or not).

So the study sees three basic deployment scenarios. In areas representing 80 percent of U.K. homes, two or more gigabit-capable networks are possible. That includes larger cities and towns.

Other, less dense areas might support only a single network. That might include about 10 percent of all U.K. homes.

Very rural areas, representing about 10 percent of homes, will need subsidies to support building of a single new network.

The big unknown is the degree of mobile substitution, which will make the business case for fixed networks tougher.

![Honolulu: A Novel by [Brennert, Alan]](https://images-na.ssl-images-amazon.com/images/I/51nR2MVno1L.jpg)