Reasonable people can, and do, disagree about the wisdom of AT&T’s acquisitions of DirecTV and Time Warner. In fact, it is likely easier to find opponents than supporters of each move.

Many argue AT&T should be more like Verizon, and stick to mobile, or connectivity services. That’s a reasonable argument, but some would argue Verizon has different legacy assets, and therefore can pursue different revenue strategies than AT&T.

For starters, the fixed network no longer drives growth for anybody.

Verizon simply cannot grow very much in its fixed network business, so one might argue the emphasis on mobile makes sense. On the other hand, Verizon cannot grow that much in mobility, either, given market maturity.

AT&T also cannot grow very much in mobility, competing against Verizon as the leader, and T-Mobile and Sprint as the challengers.

Both Verizon and AT&T must find revenue growth, though, to fund their dividend payments. And that is where the issue of strategy becomes so perplexing. Verizon has managed its debt better than AT&T by restricting its ambitions.

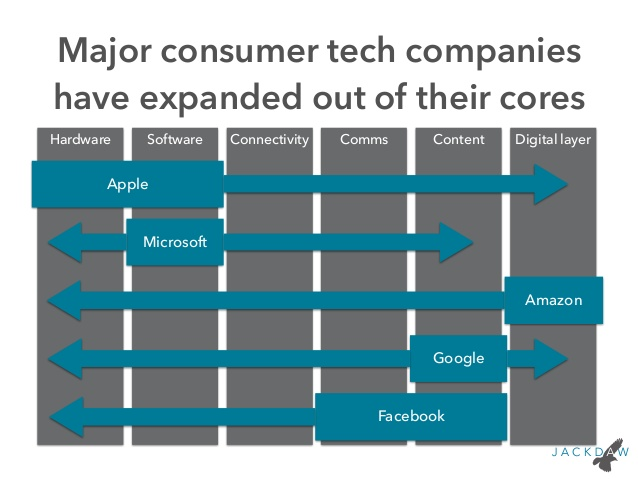

AT&T has chosen to grow into new parts of the ecosystem, at the cost of high debt positions.

In the near term, financial analysts tend to prefer Verizon’s approach, and many think AT&T should retrench.

Being someone who believes the long-term trends are for connectivity prices to continue to dip towards zero, and with competition impinging on legacy revenue models, I do not believe a “stick to your connectivity knitting” approach is workable, long term.

Organic growth will be extremely difficult to maintain, and that, to me, means acquisitions will be necessary. The issue is what sorts of acquisitions are possible.

For a substantial amount of time, both AT&T and Verizon got a majority of their growth from acquisitions. In fact, the additional scale also played a meaningful part in organic growth.

Recently, Verizon has tried to grow organically, while AT&T has made acquisitions to reshape the company’s revenue streams outside connectivity.

Many do not like AT&T’s moves.

But we might ask a simple long term question: how is it safe for “connectivity services” providers to entrench in that sole role when the whole rest of the ecosystem is moving across it? It is not easy. It will be dangerous. But what is more dangerous than staying in one silo whose revenue is not growing, when profit margins continuously drop, and when competitors from other parts of the ecosystem are moving to displace the pure connectivity role.

Among the other issues is the declining financial return from each next-generation mobile platform, at least in terms of the number of years of useful life obtained from each platform. Simply, return on assets has been falling, in part because each network has a shorter useful life.

And if we know anything about the modern telecom business, it is that organic growth, while still important, does not tend, over time, to drive total revenue growth. To me, that means acquisitions are necessary.

We may disagree about which acquisitions make sense (horizontal, vertical, internationally or domestic). It seems much less contentious to argue that future acquisitions will be necessary.

As far as the wisdon of the DirecTV and Time Warner acquisitions, I have yet to see any clear evidence--from those who think AT&T should not have made one or both of those buys--that some other deployment of capital, or not spending, for that matter, would have had a better outcome for AT&T in the revenue and free cash flow areas, near term.