There are many reasons why communications networks--especially those serving consumer customers--must constantly drive capital investment and operating costs down. But data consumption and ability to pay are the two biggest reasons. The former is unlimited; the latter sharply limited.

Data consumption simply keeps growing, Cisco Visual Networking Index always shows.

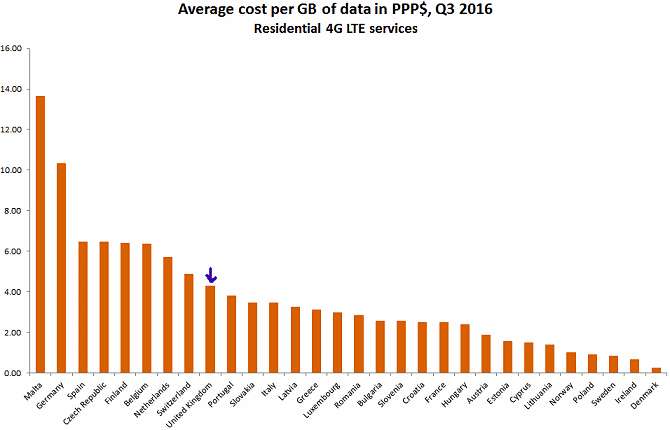

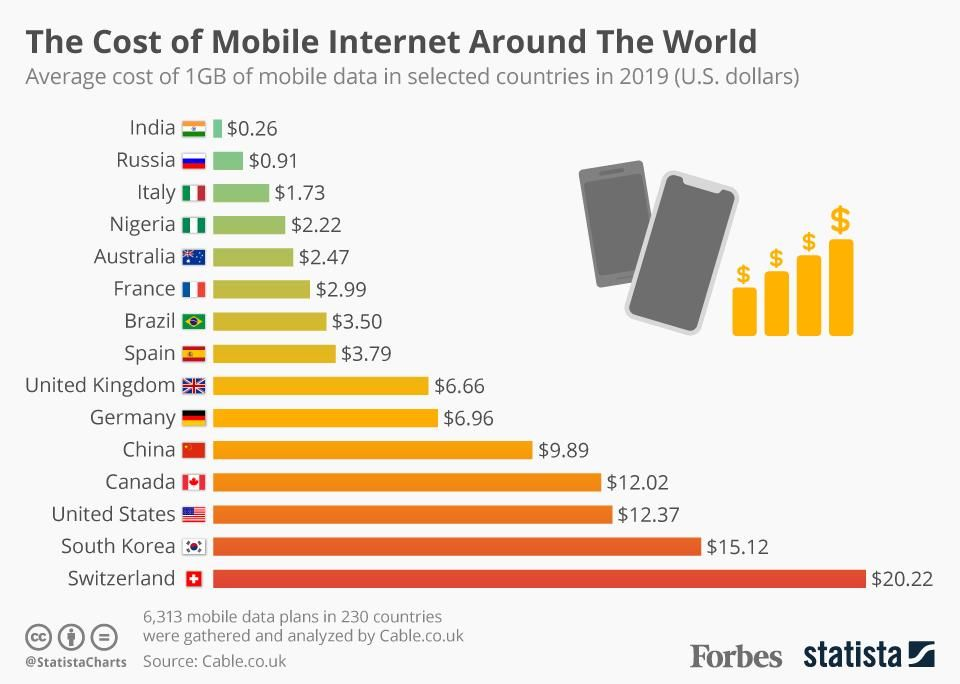

Consumer spending is quite limited. As data from the United Kingdom shows, consumer spending on mobility, mobile data or communications services does not change much from year to year. Data from the U.S. market shows similar trends.

The big takeaway is that consumer budgets tend to be highly fixed.

So the big business challenge for mobile operators is finding ways to increase the supply of bandwidth, for roughly the same retail prices, while maintaining profit margins.

And 5G, though touted for enabling many new use cases and applications, actually is one solution to the need for lower capex and opex.

To be sure, 4G can keep supplying additional capacity, up to a point. A few technologies, better radios and small cell architectures are key to that effort.

Among the technology improvements, many would point to MIMO radios, 256 QAM for more intense modulation and carrier aggregation (for 60 MHz bandwidth or more) as ways to get to gigabit 4G.

The 3GPP standards for 4G support aggregating up to 32 carriers for LTE. Not only does that create bigger channels that support more bandwidth, and therefore higher speeds, but doing so also increases efficiency, eliminating bandwidth that otherwise would be wasted for guard bands.

Operators are deploying massive MIMO antenna configurations with up to 128 antenna elements (64 transmit and 64 receive), which increases bandwidth by essentially creating multiple parallel channels where a single-antenna system has but one channel.

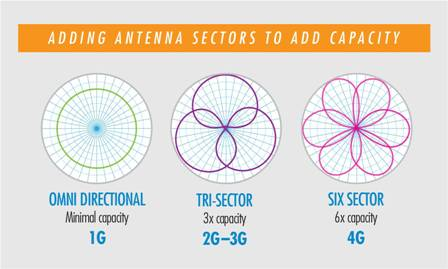

Radios also are using more heavily sectorized radios, which supply more effective bandwidth by reducing interference. Where traditionally cell tower radios have used three sectors, 4G cell sites now use six sectors or nine sectors.

Denser networks using smaller cells also are part of the solution, creating more effective bandwidth by more intensively reusing existing spectrum.

So one might ask why not simply use 4G and add more new spectrum. Part of the issue is that the 4G standard only includes frequencies up to 5 GHz, not any frequencies above that range. Standards-compliant network elements and platforms therefore cannot be purchased to support spectrum above 5 GHz.

The point is that 4G can continue to increase bandwidth, using a number of known technologies and architectures, but only up to a point. We cannot use spectrum above 5 GHz for 4G networks, by design.

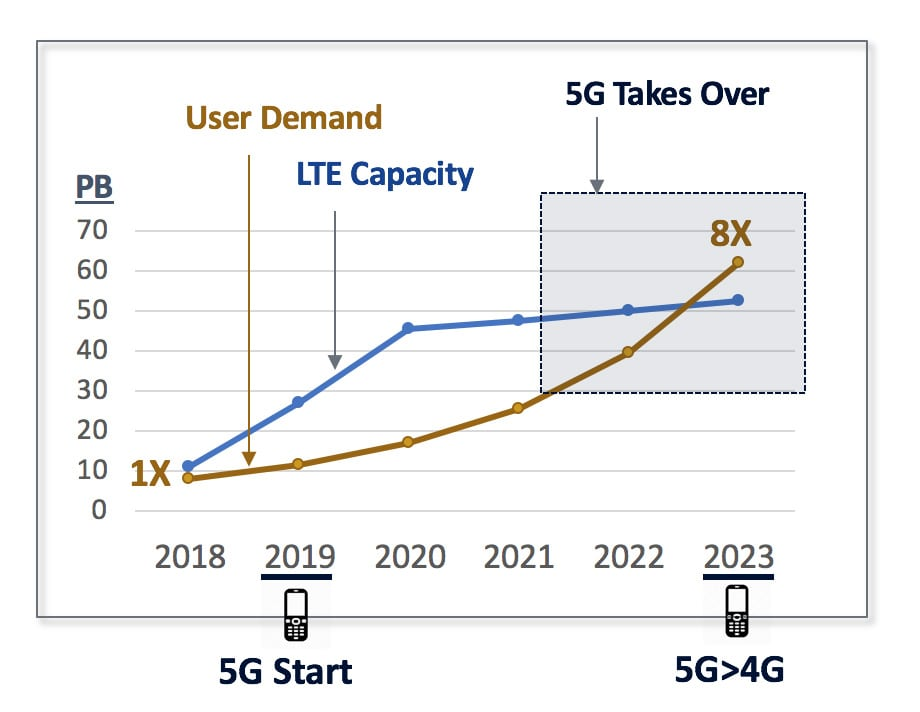

For that reason, LTE capacity will typically saturate for mobile operators from around 2020. And that is why some mobile operators already are moving to add 5G capacity.

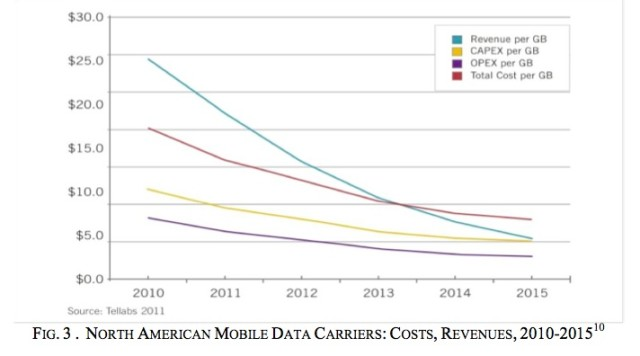

The cost of bandwidth--not just its supply--is another reason for the planned switch to 5G. As users continue to increase their bandwidth consumption, their propensity to pay does not.

In fact, the fundamental reality is that more bandwidth must be supplied at roughly the same retail price, all other things being equal.

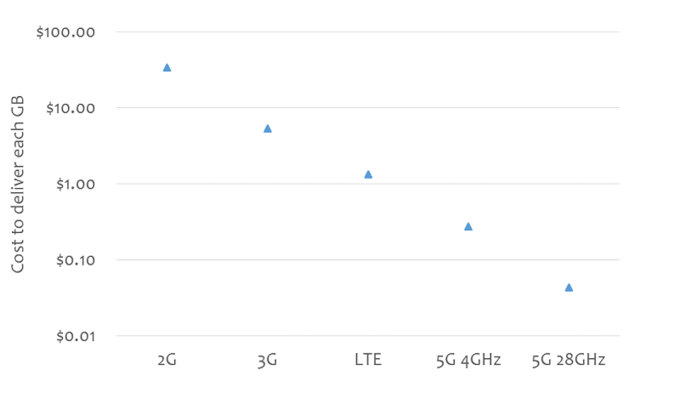

So 5G makes sense because it offers a cost per gigabyte at least 10 times lower than 4G, to start, and using a range of technologies and architectures might conceivably get to cost per gigabyte 100 times lower than 4G. That will especially be possible using millimeter wave spectrum.