Wednesday, January 29, 2020

NTT Global Data Centers Execs on What is Happening in Data Center Market

Joe Goldsmith,NTT Global Data Centers, Americas Chief Revenue Officer and Steve Manos, NTT Global Data Centers, Americas Vice President of Global Accounts talk about what they see happening in the data center market and what NTT is doing to meet customer requirements.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Tuesday, January 28, 2020

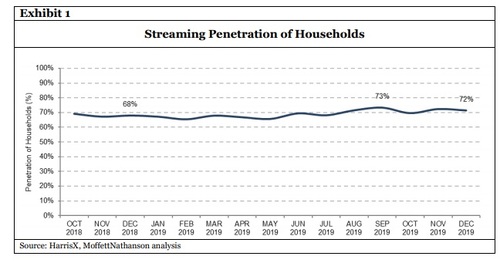

How Many Streaming Services Will Consumers Ultimately Buy?

Virtually nobody believes Netflix will be unaffected by new competition coming from Disney+, Peacock, Apple and HBOMax, as well as existing competition from Amazon Prime and Hulu. So far, Disney+ has gained about 20 million accounts in about a quarter.

Still, use of Netflix penetration remained steady throughout 2019 while the penetration rates for both Hulu and Amazon Prime grew about six percent, according to MoffettNathanson and HarrisX .

Some 90 percent of Disney+ customers appear to buy Netflix as well. At least so far, it appears that Disney+ is complementary to Netflix, not cannibalizing it.

It is of course possible that market share could start to shift more significantly when HBO Max launches in May 2020 and Peacock launches in July. The issue is how many different services customers will be willing to buy.

At the moment, that number seems to hover between two to three subscriptions in some studies; three to four subscriptions per household in others.

So the issue is whether the market saturates at five or more subscriptions per household.

That might seem a stretch, but some households looking at the landscape, and which services have “must see” content already estimate they might need to buy five different subscriptions.

The other issue is that Netflix is the first global service. The others arguably will compete primarily in the U.S. market, to start.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

What Will 5G Mean for the Rest of the Ecosystem?

What might 5G mean for all those in the ecosystem aside from mobile service providers? What will change, and what possibly could happen in the rest of the ecosystem, ranging from chips to apps; use cases to business models? How does 5G bring those changes? Where is the upside and the downside?

Dean Bubley, Director, Disruptive Analysis, United Kingdom

John Ghirardelli, Director, U.S. Innovation, American Tower Corporation, USA

Ramy Katrib, CEO & Founder, DigitalFilm Tree, USA

Yang Yang, Co-Director, and Professor, School of Information Science and Technology, SHIFT, and ShanghaiTech University, Peoples Republic of China

Gary Kim, Consultant, IP Carrier, USA

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

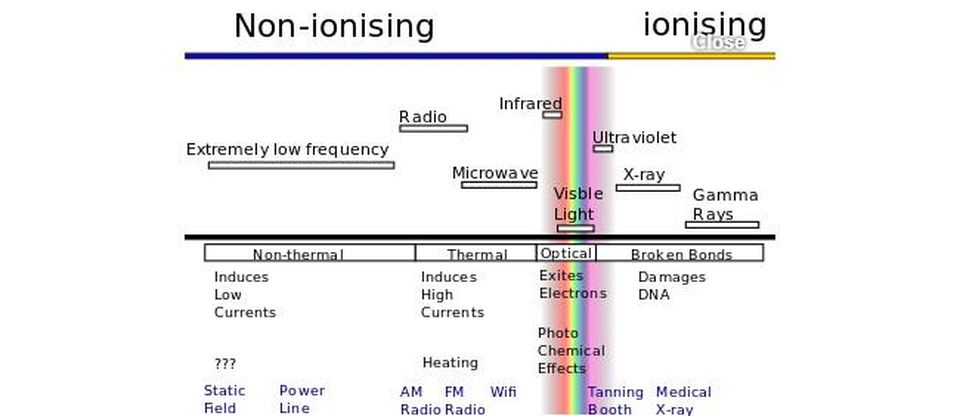

Are Wi-Fi Routers Dangerous to Your Health?

As long as I can remember, there have been periodic and generally low level concerns about non-ionizing radiation--the type of energy radio signals represent. By non-ionizing, we mean that the signals are not capable of dislodging electrons atoms or molecules, as are x-rays or gamma rays. Ionizing radiation, in high doses, is carcinogenic, though useful in low doses.

Non-ionizing radiation can cause tissue heating, as you can experience with food in a microwave oven. The health concerns about non-ionizing radiation come from the potential long term exposure. As with any form of natural radiation (sunlight, for example), the key is exposure levels.

The key thing about non-ionizing radiation is that it is found, in real-world communications cases, at very low power levels. Also, signals decay logarithmically.

This is an illustration of how a Wi-Fi router’s power levels drop rapidly with distance. Power levels drop more than half in the first two meters. Once people are about four meters from the router, signal levels have dropped from milliWatts to microWatts, about an order of magnitude (10 times).

Some people are concerned about power emitted from mobile cell towers. Keep in mind that mobile radios on cell towers have power levels that decay just as do Wi-Fi signals. Some liken the power levels of a mobile radio on a tower to that of a light bulb.

Radio signals weaken (attenuate) logarithmically, by powers of 10, so the power levels decay quite rapidly.

Basically, doubling the distance of a receiver from a transmitter means that the strength of the signal at that new location is 50 percent of its previous value. Just three meters from the antenna, a cell tower radio’s power density has dropped by an order of magnitude (10 times).

At 10 meters--perhaps to the base of the tower, power density is down two orders of magnitude. At 500 meters, a distance a human is using the signals, power density has dropped six orders of magnitude.

Though there is no scientific evidence that such low levels of non-ionizing radiation actually have health effects, such as causing cancer, a prudent human will limit the amount of exposure, just as one takes the prudent risk of wearing a seat belt in an automobile, minimizing time spent in the sun and so forth.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Would It Have Made a Difference If Telcos Had Stuck with ATM?

It is no longer a question, but there was a time not so long ago when global telcos argued for asynchronous transfer mode (broadband ISDN) as the next-generation protocol, rather than TCP/IP.

A report issued by Ovum in 1999 argued that “telecommunications providers are expected to reinvent themselves as operators of packet-switched communications networks by 2005.”

“Growth in Internet Protocol (IP) services is expected to fuel the transition,” Ovum argued.

Of course, all that was before the internet basically recreated the business, making connectivity providers a part of the broader ecosystem of applications, services and devices requiring internet connectivity to function.

In retrospect, it might seem obvious that the shift of all media types (voice, video, image, text) to digital formats would make TCP/IP a rational choice. But that was not the case in the telecommunications industry from the 1980s to the first decade of the 21st century. Telco engineers argued that ATM was the better choice to handle all media types.

But the internet, cheap bandwidth and cheap computing all were key forces changing the economics and desirability of IP, compared to ATM.

Once internet apps became mass market activities, network priorities shifted from “voice optimized” to “data optimized.”

Connection-oriented protocols historically were favored by wide area network managers, while connectionless protocols were favored by local area network managers. The relative cost of bandwidth drove much of the decision making.

WAN bandwidth was relatively expensive, LAN bandwidth was not. That meant the overhead associated with connectionless protocols such as TCP/IP did not matter. On WANs, packet overhead mattered more, so lower header overhead was an advantage.

It is by no means clear that the choice of a connectionless transmission system, instead of the connection-oriented ATM, would have changed the strategic position of the connectivity provider part of the internet ecosystem. Indeed, one key argument for IP was simply cost: IP devices and network elements were much cheaper than ATM-capable devices.

One might argue the global telecom industry simply had no choice but to go with IP, no matter what its historic preferences might have been.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Monday, January 27, 2020

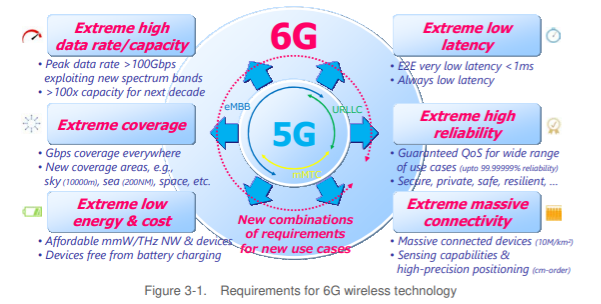

Applications and Use Cases are Big 6G Challenge

The whole point of any access network is send and receive user and device data as quickly as possible, as affordbly as possible, to the core network and all the computing resources attached to the core network. The future 6G network, no less than the new 5G network, is likely to feature advancements of that type.

Bandwidth will be higher, network ability to support unlimited numbers of devices and sensors will be greater, latency will be even lower and the distance between edge devices and users and computing resources will shrink.

The biggest unknowns are use cases, applications and revenue models, as has been true since 3G. The best analogy is gigabit fixed network internet access. Users often can buy service running at speeds up to a gigabit per second. Few customers presently have use cases requiring far lower speeds.

So it is likely that 6G, as will 5G, often will feature capabilities that exceed consumer use cases, initially.

NTT Docomo has released a white paper with an initial vision of what 6G will entail. Since every mobile generation since 2G has increased speeds and lowered latency, while connection density grew dramatically between 4G and 5G, we might look first to those metrics for change.

Docomo suggests peak data rates of 100 Gbps, latency under one millisecond and device connection density of 10 million devices in each square kilometer would be design goals.

Along with continued progress on the coverage dimension, 6G standards might extend to space, sky and sea communications as well. Docomo also believes quality of service mechanisms exceeding “five nines” and device performance (no charging devices, cheaper devices) would be parts of the standard.

Looking at commercial, economic or social impact, since the 3G era we have tended to see a lag of execution compared to expectations. In other words, many proposed 3G use cases did not emerge until 4G. Some might say a few key 4G use cases will not flourish until 5G is well underway.

For that reason, we might also discover that many proposed 5G innovations will not actually become typical until the 6G era. Autonomous vehicles are likely to provide an example.

So Docomo focuses on 6G outcomes instead of network performance metrics. Docomo talks about “solving social problems” as much as “every place on the ground, sky, and sea” having communications capability. Likewise, 6G might be expected to support the cyber-physical dimensions of experience.

Also, 5G is the first mobile platform to include key support for machine-to-machine communication, instead of primarily focusing on ways to improve communication between humans. Docomo believes 6G will deepen that trend.

It is worth noting that the 5G spec for the air interface entails availability higher than the traditional telecom standard of “five nines” (availability of 99.999 percent). 5G networks are designed to run at “six nines.” So 6G might well run at up to “seven nines” (99.99999 percent availability).

The legacy telecom standard of five nines meant outages or service unavailability of 5.26 minutes a year. The 5G standard equates to less than 32 seconds of network unavailability each year. A seven nines standard means 3.16 seconds of unavailability each year.

Some might say 4G was the first of the digital era platforms to design in support for internet of things (machines and computers talking to machines and computers) instead of the more traditional human mobile phone user. That trend is likely to be extended in the 6G era, with more design support for applications and use cases, with artificial intelligence support being a key design goal as well.

In part, that shift to applications and use cases is more important as the wringing of traditional performance out of the network becomes less critical than new use cases taking advantage of performance boosts.

As it already is the case that almost no consumer users actually “need” gigabit speeds, much less speeds in the hundreds of megabits per second, so few human users or sensors will actually “need” the 6G levels of throughput and latency.

Architecturally, the evolution towards smaller cells will continue, in part to support millimeter wave frequencies, in part to assure better connectivity. Where traditional cell architectures have emphasized non-overlapping coverage, 6G networks might use orthogonally non-aligned cells (overlapping), deliberately overlapping to assure connectivity.

That almost certainly will require more development of low-cost beam forming and signal path control. Having cheap artificial intelligence is going to help, one might suggest.

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Friday, January 24, 2020

Like it or Not, Dumb Pipe is the Fixed Network's Foundation

Perhaps you see the irony of cable TV executives saying their businesses, once founded on selling applications, now see the killer use case as internet access, a textbook example of “dumb pipe.”

“We’ve made a pivot to a broadband-centric cable company,” said Comcast CEO Brian Roberts. That is another way of saying the strategic product for a multi-product company is a classic “dumb pipe” service that is the prerequisite for using all TCP/IP-based apps and services deliverable by the public internet.

If you ask virtually any telecom executive selling services to consumers (business to business is a different matter), you are likely to hear executives say they are not just “dumb pipes,” in the sense of providing a low-value, commodity-priced product. Rather, you will hear any number of arguments that the full range of products provides higher value, differentiated products at a range of prices and profit margins, sometimes to more-attractive customer bases and geographies.

What many cable TV executives now argue is that their network services are based precisely on dumb pipe internet access, and not the traditional video subscriptions that historically drove value, revenue and profits.

That is but one example of how the internet, and the separation of applications from networks, has revolutionized the communications and computing businesses.

Until the internet era, all consumer mass market services were “apps,” not “dumb pipe.” Consumers bought the app called “dial tone,” the ability to place a phone call, not directly the use of a wire enabling the use of dial tone. Customers bought cable TV not to use a coaxial cable or modulated radio frequency signals, but to watch video. People bought mobile phones and used mobile services to send and receive text messages, not to use a data channel.

In the internet era, the “value” of fixed network voice, mobile voice, mobile messaging and linear TV subscriptions has dropped. The value of access to the internet (a dumb pipe service) has grown, in both mobile and fixed domains.

So consumer preferences--and the revenue earned--has changed. Though the value of mobile communications “anywhere” remains, the value of some apps (voice, messaging, linear video) has declined.

Or, put another way, dumb pipe has grown more important, while traditional apps have become less important and valuable.

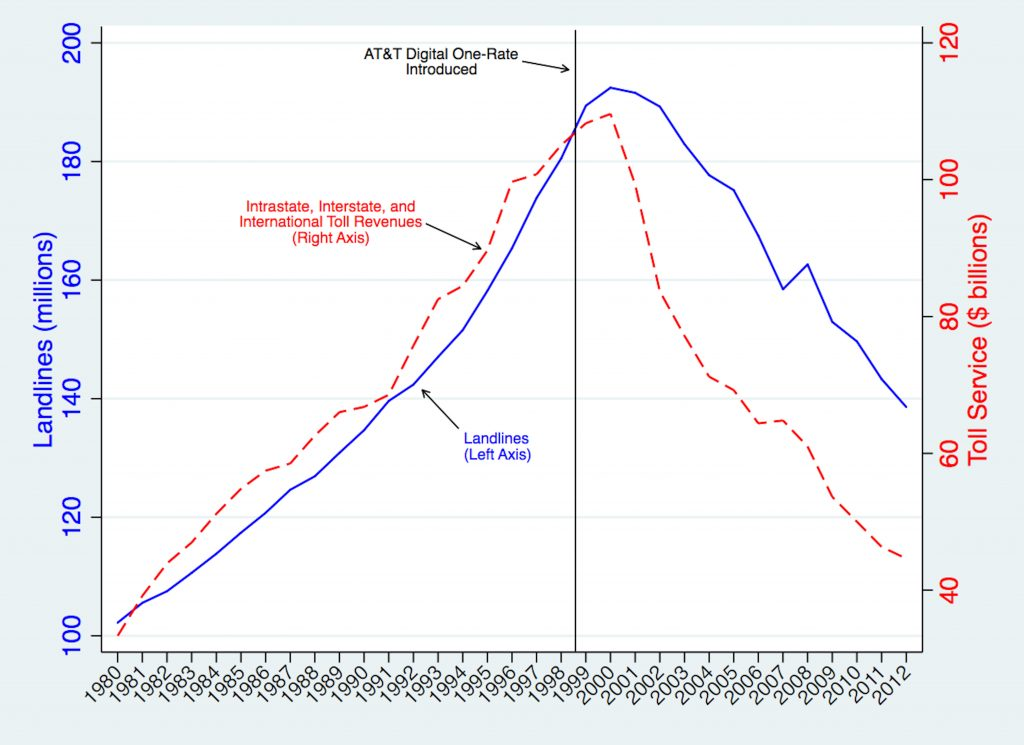

This can be seen clearly in the shifts of service provider revenue in the U.S. market from long distance--the former revenue and profit generator--to mobile service. What one sees is a 50-percent toll revenue drop over a decade, and its replacement by a new lead service, mobility.

But the mobile network uses rival facilities. The fixed network business model now hinges on dumb pipe internet access. Other services and apps are important: how many service providers would willingly surrender their voice or video revenues?

But new questions must be asked. To the extent the fixed network must rely increasingly on one service--internet access--how does the business model change, and how? Can the full value of capital investments be recouped solely or primarily from internet access?

If not, what can be done to find replacements for lost voice and video revenue? And how soon will most fixed network executives become comfortable saying their business models are built on dumb pipe? For how many service providers will this prove true?

Gary Kim has been a digital infra analyst and journalist for more than 30 years, covering the business impact of technology, pre- and post-internet. He sees a similar evolution coming with AI. General-purpose technologies do not come along very often, but when they do, they change life, economies and industries.

Subscribe to:

Posts (Atom)

Will We Break Traditional Computing Era Leadership Paradigm?

What are the odds that the next Google, Meta or Amazon--big new leaders of new markets--will be one of the leaders of the present market, b...

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...