Facilities-based competition radically changes the economics of any fixed network access market because it radically disrupts the ability to reap financial returns from any network investment. The math is pretty simple. All monopoly-era mass market networks assumed the customer or user base was nearly “all” households or consumers.

So “network cost per customer” or “per user” was nearly identical with “cost per location.” Likewise, “revenue per location” was nearly identical with “location.”

That all changes with facilities-based competition. Assume two equally-skilled facilities-based competitors operating ubiquitously in any area, one the legacy monopoly provider, the other a challenger.

Assume that, over a period of perhaps a decade, a former monopolist loses 50 percent market share to the new competitor. By definition, the revenue per location drops in half, while the cost per location doubles.

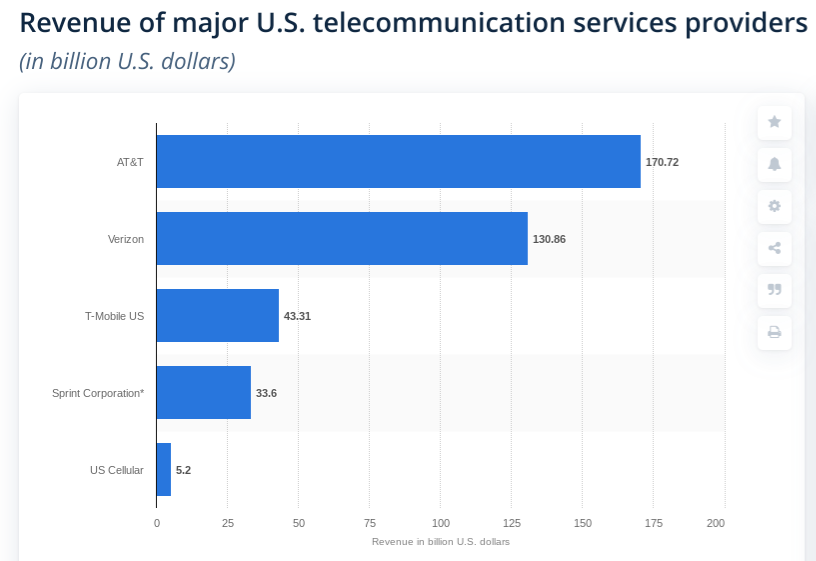

Telco losses in the U.S. market have been far worse than that. Taking all voice lines into consideration, fixed network share of voice lines (all suppliers) now is about 35 percent. Mobile has 65 percent share of accounts.

Looking only at fixed network accounts, U.S. telcos have about 36 million accounts, while competitors (cable providers and independent VoIP providers) have 62 million accounts. If there are roughly 146 million household locations, telco sales of voice reach only about 25 percent of locations. So voice stranded assets are as high as 75 percent.

In the increasingly core internet access business, telcos have about 38 million accounts, or about 26 percent of locations. So stranded internet access assets are as high as 74 percent. You might make roughly the same argument for video entertainment accounts.

It gets worse. Assume that for some services, there actually are three, possibly four facilities-based suppliers (satellite video providers, for example). Assume those competitors are competent as well. Assume those other competitors have a combined 20 percent market share.

Then the two fixed network providers have a theoretical 40-percent market share. That reduces revenue per location further, and raises cost per location. So 60 percent of the network investment is stranded.

Further assume customer demand changes that steadily reduce revenue to be earned on the network. You can see this in voice take rates and now linear video take rates. That further raises cost per location and reduces revenue per location.

To be sure, scale matters in the telecom industry, as it does in many capital-intensive industries, because heavy capital investment means financial returns are boosted by intensive use of those assets.

Perhaps another way of saying “scale matters” is to note that market share matters for profitability.

So network utilization--the ability to load revenue-generating traffic and services onto the network--has been a key issue for at least two decades, especially where facilities-based competition is possible.

Typically, in any market, the supplier with the largest market share also is the most profitable. In the mobile phone business, it has been true for some years that most actual profits in the handset supplier portion of the ecosystem have been reaped by just two firms, Apple and Samsung.

One salient feature of the internet ecosystem is that it tends toward “winner take all” market structures, whether one looks at the application, operating system, device or access parts of the ecosystem.

In the application space, advertising revenue is dominated by Google and Facebook, which claim 63 percent of U.S. digital ad revenue in 2017. In the operating system market, Android and Apple iOS were the leaders, with 99-percent market share. The device portion of the market is the least concentrated, although Apple and Samsung have earned most of the profits.

Mobile and fixed network access markets likewise are oligopolies, in virtually every market. Fixed markets in many cases remain virtual monopolies, while mobile markets tend to be oligopolies.

But scale alone is proving to be an elusive way of assuring profits.

Business strategies in the global telecom business have changed over the past four to five decades. Five decades ago, profits were driven by long distance calling and the base business was selling monopoly voice to everyone.

Sometime in the 1980s the revenue and profit growth shifted from fixed network long distance to mobility. Fixed network operators facing stiff competition switched to a multi-product consumer services strategy.

By the 2000s subscription growth drove mobile revenues. By the 2010s internet access began to be the revenue driver for fixed and mobile operators, not voice or subscriptions.

It might be a matter of debate how much internal industry decisions and external forces have shaped strategy.

As we enter the 5G era, it is possible to say that the fortunes of some mobile operators were determined early in the 3G era. Though it is reasonable to suggest that issues ranging from addressable internal market to regulatory policy have mattered, some argue that excessive spending on spectrum licenses for 3G created debt problems that hobbled mobile operator ability to foster growth.

But business strategy might also have played a role. When organic growth is quite slow, one obvious solution is to expand geographically, buying market share out of region, in other words. Many European firms, for example, went on a huge global expansion spree in the 3G and 4G eras.

It also is impossible to ignore the impact of the internet and IP generally. Those trends essentially opened up the communications networks, ending the walled gardens that historically characterized telecom business models.

At the same time, the end of walled gardens, and the ease of competing “over the top” also mean that any telco-owned apps often must compete with third-party apps. And telcos never have been known for their prowess at creating big and popular new apps.

Historically, there has been a simple solution for telcos wanting to enter new lines of business: acquisition.

The new problem is that app provider market valuations and multiples make acquisitions of such firms expensive for telcos. In other words, telcos contemplating big app asset acquisitions encounter the price of expensive-currency assets to be bought with cheap currency.

That has restricted the historically-important acquisition method telcos have used to enter new markets. In the past, most telcos have gotten entry into new and faster-growing markets by acquiring, rather than building, the new businesses.

That is much harder when the would-be acquisitions are of high-multiple application suppliers, using low-multiple telco stock or borrowed money. Most telco free cash flow typically must be deployed to pay dividends and reduce past borrowings.

Taken together, all those trends now suggest that decades-old geographic expansion plans conducted by some mobile operators now are unwinding, as the contribution to revenue growth has not often been matched by increases in profits.

And that poses new strategy issues: where is revenue growth to be found if geographic expansion, once a logical path to growing revenue, is unavailable? The other logical answer--acquisitions of fast-growing firms in new markets--often is impossible because the market multiples of such firms are high, while telco valuations are low.

In other words, acquisitions big enough to move the revenue needle cannot be made. Smaller acquisitions are possible, but often, because of small size, cannot move the revenue needle. And, in any market where scale matters, organic growth might never be fast enough to gain leadership.

Most telcos, in most markets, have learned from their experiences with overpriced spectrum bids. Seldom, anymore, do spectrum prices seem unreasonable. On the other hand, the core telecom business is in slow growth mode in most markets, if still relatively higher in some emerging markets.

Among the big new questions--if geographic expansion is not generally feasible--is how to reignite growth, especially in promising new markets.

Compounding those questions is the growing need to look at revenue growth from outside the legacy domains based on connectivity services. Almost everyone assumes that will be quite difficult.

The traditional fear is that telcos really are not good at running businesses outside their core. And there are good reasons for that opinion. But with growth so slow in the core business, and competition not abating, while geographic expansion often is unpromising, telcos may ultimately have no choice.

Of course, there are other paths. It might well be that most telcos will be unable to sustain themselves over the next few decades, as they are unable or unwilling to expand beyond connectivity. In that case, bankruptcy lies ahead, with potential restructuring of much of the business.

Precisely how advanced connectivity still can be provided, if today’s business models fail, is not clear. It long has been the conventional wisdom that, in any competitive market, the low cost provider wins. Who those low-cost providers might be then is the issue.

The other path, which only the biggest telcos might contemplate, aer risky, expensive acquisitions--exposing themselves to harsh criticism--to create new business models not so exclusively dependent on connectivity revenues.

We already can see some illustrations of the stark choices. When big and small cable operators alike start to say their future is internet access, not video or voice, one must ask whether such a single product strategy will work, long term. The major reason why telcos and cable operators in the U.S. market have survived competition is a switch from single-product to multi-product strategies.

Essentially, they sell more things to a smaller number of customers. That might not work if the new model is one product sold to many customers, especially if the main competitors in those markets are competent.

Cable operators clearly dominate market share in the U.S. fixed network internet access business. The issue is whether the business model works without other customer segments and products. If the answer is no, then the multi-product strategy will still have to be pursued.

The big shift might be from multi-product consumer bundles to multi-product operations based on consumer fixed network internet access, consumer mobility and business capacity services.