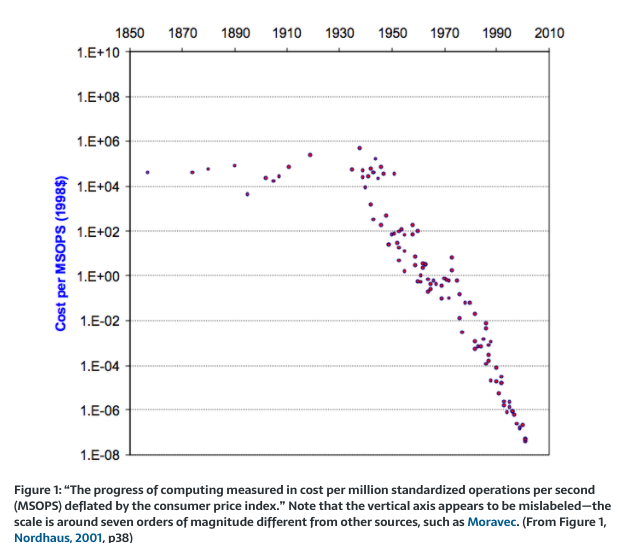

Economist William Nordhaus has estimated that computing costs have fallen dramatically since the 1940s, improving by an order of magnitude every four years in the 1980s and 1990s, for example. You can safely argue that this vast reduction in cost underpins the shift to affordable digital transformation of all types, not to mention the broader shift from physical to digital processes.

Monday, May 31, 2021

No Digital Transformation Without Computing Cost Reductions

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Scale Matters for Cloud Computing Economics

Scale matters where it comes to many computing use cases. As useful as hosted voice services are, total cost of ownership is higher for large enterprises than an “owned infrastructure” approach, primarily because costs are directly related to the number of lines supported.

Some companies with high reliance on computing facilities, such as software firms, will often find they can cut costs dramatically by shifting computing operations back to their own facilities, and off computing as a service platforms, partners at Andreessen Horowitz argue.

That appears to be especially true for public software companies, where the computing infrastructure is an unusually-high percentage of total costs, Andreessen Horowitz argues.

“When you factor in the impact to market cap in addition to near term savings, scaling companies can justify nearly any level of work that will help keep cloud costs low,” say Sarah Wang and Martin Casado, Andreessen Horowitz partners.

“A billion-dollar private software company told us that their public cloud spend amounted to 81 percent of cost of revenue,” they say. Also, “cloud spend ranging from 75 to 80 percent of cost of revenue was common among software companies.”

Citing the example of Dropbox, the partners note that “when the company embarked on its infrastructure optimization initiative in 2016, they saved nearly $75 million over two years by shifting the majority of their workloads from public cloud to ‘lower cost, custom-built infrastructure in co-location facilities’ directly leased and operated by Dropbox,”

Dropbox gross margins increased from 33% to 67% from 2015 to 2017, which they noted was “primarily” due to Infrastructure optimization and an increase in revenue.

Thomas Dullien, former Google engineer and co-founder of cloud computing optimization company Optimyze, estimates that repatriating $100 million of annual public cloud spend can often result in nearly $50 million in annual total cost of ownership from server racks, real estate, cooling, network and engineering costs, they note.

Other sources estimate savings ranging from 33 percent to 50 percent, they add. “A director of engineering at a large consumer internet company found that public cloud list prices can be 10 to 12 times the cost of running one’s own data centers, the partners say.

Smaller firms, earlier in their growth cycles, almost always benefit from cloud computing, rather than building their own computing infrastructures. But that can reverse when firms grow larger and growth slows.

“It’s becoming evident that while cloud clearly delivers on its promise early on in a company’s journey, the pressure it puts on margins can start to outweigh the benefits, as a company scales and growth slows. Because this shift happens later in a company’s life, it is difficult to reverse,” say Sarah Wang and Martin Casado, Andreessen Horowitz partners.

“You’re crazy if you don’t start in the cloud; you’re crazy if you stay on it,” the paradox becomes.

The issue is how cloud spending versus owned facilities plays out over time for firms in other lines of business that might not have computing cost as such a large driver of total cost of revenue.

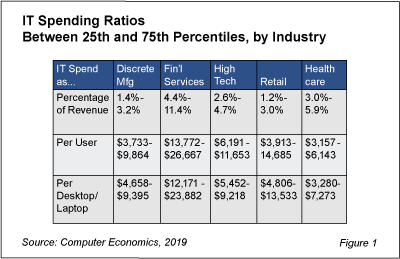

For most connectivity providers, computing cost is not likely a huge driver of total cost of revenue. Information technology costs vary by industry from 1.4 percent in manufacturing to 11.4 percent in the financial services industry, for example.

Others estimate information technology spending in about the same ranges, though spending varies by firm even within each industry. Some might argue maintenance levels of spending could range about two percent of revenues, while growth spending might range up to perhaps six percent of revenue.

Perhaps most firms spend between two and three percent of revenue on all IT.

Few industries have computing costs as such a large driver of cost as do software firms. Few firms in most industries can improve equity valuations or profits as much as software firms can by optimizing computing cost.

For most firms in most industries, the balance of owned versus “computing on demand” spending might not be crucial in that regard.

In principle, if the same savings software firms obtain by optimizing computing spend were to hold universally, most firms in most industries could save relatively little by optimising computing choices. Saving 33 percent, if possible, on an item that represents two percent to three percent of total cost of revenue is helpful, but arguably not all that significant as a driver of cost and profit.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Friday, May 28, 2021

Vertical Integration Versus Portfolio of Assets: Which Works Better?

“Vertical integration” can be problematic for any non-connectivity asset held inside a telco entity. Ask AT&T or Singtel.

AT&T’s purchase of Time Warner was an effort to vertically integrate into content. The goal, says AT&T CEO John Stankey, was to “help our domestic connectivity business.” As AT&T now sees matters, the streaming content business must be built globally, and not restricted to a single country, which is primarily AT&T’s connectivity business base.

That--at least as AT&T now positions the matter--requires a globally-focused business unencumbered by considerations of the domestic market. So AT&T wants to combine its Warner Media assets with Discovery, creating a larger new entity in which it owns 70 percent of the equity.

That will remove Warner from AT&T’s consolidated results. Needless to say, valuation of such a standalone business should exceed the valuation if the asset were embedded within a telco organization.

Among the other possible ways to view such assets is the ability to produce free cash flow, revenue growth and profit margins for the mother company, even if not fully consolidated within the telco itself.

In fact, valuation might be higher precisely because a “pure play” content or streaming asset is valued as other similar assets are.

Singtel, Southeast Asia's largest telecoms operator, reported that annual net profit halved to S$554 million ($418 million), the lowest net profit in at least two decades. That performance by a leader in exploring additional lines of business illustrates three related issues.

The first issue is the exhaustion of legacy connectivity services markets. The second issue is the traditional difficulty or entering new markets, either in other parts of the ecosystem or in content or applications.

The third issue is the valuation penalty any successful “up the stack” asset (content, platform, application) has when buried within the telco organization.

Singtel has been trying to diversify for years, and has been a leader in exploring growth “up the stack” in the application layer, and beyond connectivity. So the inability to reap profit rewards is troubling.

But some investments such as those in digital marketer Amobee and cyber-security firm Trustwave yielded weaker-than-expected returns, observers note. That is a recurring story for telcos who have tried for many decades to broaden their revenue bases in adjacent areas such as software or computing services.

The next moves might pair infrastructure asset sales to fund investments in other growth areas such as financial services or gaming.

At least part of the problem is valuation of telco infrastructure assets. Singtel notes that its infrastructure assets do not provide a valuation boost, compared to other suppliers that own fewer network assets.

The other issue is that Singtel executives believe ownership of towers, satellites, subsea cables and data centers has not boosted Singtel’s valuation, compared to peers who own less of such assets. The expectation is that selling some of those infrastructure elements will free up capital to deploy in other growth areas.

Weakness in mobile services revenue and market share is among the current issues. Mobile service revenue dropped 19 percent; blended average revenue per user fell 18.5 percent and subscriptions fell 3.6 percent over the last year, for example.

That is not a unique problem. Globally, other service providers face low growth rates and falling ARPU. Saturation of mobile services--the industry growth driver for decades--is part of the problem.

Beyond that, the typical telco must replace half of existing revenue every decade or so. We have seen that in fixed network voice services, mobile voice, long distance revenue and fixed network services generally. We have seen it in text messaging as well.

That might seem hyperbole, but is a demonstrable fact. Globally, that means telcos have to generate about $400 billion in new revenue just to replace what they will lose over the next decade.

Singtel’s issues really are the same issues every connectivity service provider eventually will face. The issue is how to create huge new revenue streams, outside the connectivity core. Those who argue that amount of growth can happen within the connectivity core, it seems to me, have the burden of proof.

Vertical integration might not be the only way--perhaps not the best way--to do so. Any sufficiently large asset outside the connectivity core will get a higher valuation if outside the telco, operating as a "pure play."

That might not help connectivity business revenue and profit matgin directly, but it arguably is a better way to grow the overall business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Thursday, May 27, 2021

Where AT&T, T-Mobile, Verizon See Fixed Wireless Value

“I don't expect that fiber will ever be the solution for all of the ILEC footprint,” said John Stankey, AT&T CEO, commenting on fixed wireless as a replacement. “We're not as robust in our point of view on what fixed broadband can do in urban and highly attractive suburban areas.”

“But what we do believe is that fixed wireless plays a role in other parts of our footprint,” he said, especially in rural areas. “That's a really nice replacement for some percentage of the data customers that are out there, and we'll continue to pursue that,” he added.

That more-cautious perspective on fixed wireless, compared to Verizon and T-Mobile, grows from the respective positioning each firm has in the market.

AT&T has the largest footprint of U.S. households among U.S. telcos, and therefore has the most to lose, and the least to gain, from new investments within the more-rural parts of its fixed network territory.

Verizon has a relatively small footprint of U.S. homes, and therefore has much more to gain from fixed wireless using its mobile network, out of region.

T-Mobile has zero market share in home broadband, and clearly has the most to gain, in terms of additional revenue and market share in that business.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

The Vertical Integration Downside: Lower Valuation

Singtel, Southeast Asia's largest telecoms operator, reported that annual net profit halved to S$554 million ($418 million), the lowest net profit in at least two decades. That performance by a leader in exploring additional lines of business illustrates three related strategic issues that eventually will be faced by every connectivity service provider serving the mass market.

The first issue is the exhaustion of legacy connectivity services markets. At some point, every customers that wants service will be buying it.

The second issue is the traditional difficulty or entering new markets, either in other parts of the ecosystem or in content or applications. Telcos have had a very-difficult time sustainably creating new roles for themselves elsewhere in the value system.

The third issue is the valuation penalty any successful “up the stack” asset (content, platform, application) has when buried within the telco organization. The same asset--inside a telco--earns a less robust valuation than that same asset, outside the telco organization.

That raises the issue of "how" a connectivity provider should "own" assets elsewhere in the value chain. Vertical integration actually seems to penalize the value of assets. Which suggests some strategy of ownership "outside" the connectivity organization.

Singtel has been trying to diversify for years, and has been a leader in exploring growth “up the stack” in the application layer, and beyond connectivity. So the inability to reap profit rewards is troubling.

But some investments such as those in digital marketer Amobee and cyber-security firm Trustwave yielded weaker-than-expected returns, observers note. That is a recurring story for telcos who have tried for many decades to broaden their revenue bases in adjacent areas such as software or computing services.

The next moves might pair infrastructure asset sales to fund investments in other growth areas such as financial services or gaming.

At least part of the problem is valuation of telco infrastructure assets. Singtel notes that its infrastructure assets do not provide a valuation boost, compared to other suppliers that own fewer network assets.

The other issue is that Singtel executives believe ownership of towers, satellites, subsea cables and data centers has not boosted Singtel’s valuation, compared to peers who own less of such assets. The expectation is that selling some of those infrastructure elements will free up capital to deploy in other growth areas.

Weakness in mobile services revenue and market share is among the current issues. Mobile service revenue dropped 19 percent; blended average revenue per user fell 18.5 percent and subscriptions fell 3.6 percent over the last year, for example.

That is not a unique problem. Globally, other service providers face low growth rates and falling ARPU. Saturation of mobile services--the industry growth driver for decades--is part of the problem.

Beyond that, the typical telco must replace half of existing revenue every decade or so. We have seen that in fixed network voice services, mobile voice, long distance revenue and fixed network services generally. We have seen it in text messaging as well.

That might seem hyperbole, but is a demonstrable fact. Globally, that means telcos have to generate about $400 billion in new revenue just to replace what they will lose over the next decade.

Singtel’s issues really are the same issues every connectivity service provider eventually will face.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Wednesday, May 26, 2021

SD-WAN Gains, As Expected

SD-WAN is gaining traction in the digital business environment, a new survey conducted by Altman Solon for Masergy finds. SD-WAN adoption is expected to rise to 92 percent of companies and 64 percent of sites by 2026 with most adopting it for efficiency (38 percent), cost savings (38 percent), and agility (34 percent).

A majority of companies will use hybrid SD-WAN. Some 58 percent expect to use a hybrid access model (a mix of both public and private access) over the next five years. Both private-only access users (63 percent) and public-only access users (55 percent) are considering a shift to hybrid access.

Among respondents using a public-only or internet-only approach to SD-WAN, 50 percent said they would incorporate more private access because performance is insufficient for their critical applications.

About 23 percent of respondents use a do-it-yourself solution, and 77 percent use a fully managed or co-managed solution.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Though "Just Another G," 5G Already Enables New Revenue Sources

Oddly enough, both challengers and incumbents in the U.S. mobile market make the same argument: they are monetizing 5G right now, irrespective of new use cases and revenue sources.

In Verizon’s case the actual revenue driver is not 5G as such, but a shift by customers to higher-priced unlimited-usage plans.

“Our service revenue is growing all the time because we have this migration going from limited to unlimited premium,” said Hans Vestberg, Verizon CEO. “So, we are going to have the majority of our customers unlimited.”

In a sense, 5G is being monetized as part of the shift to higher-priced service plans. “Sometimes people ask about when will you monetize 5G?” said Vestberg. “We're already doing it” in the form of higher average revenue per user, driven by the migration to unlimited-usage plans.

Beyond that, some mobile service providers believe they are better positioned to capture market share, or have better assets in place, and can simply introduce 5G using normal or relatively normal capex spending they invest annually.

"One of the questions I've gotten for years as we planned this midband-centric 5G mobile Internet pure-play is, 'how are you going to monetize 5G?' And I've always thought it was kind of a crazy question because 5G is just the next G," said Mike Sievert, T-Mobile CEO.

T-Mobile's equity valuation, for example, has far exceeded that of AT&T and Verizon, both of which have been seen as no-growth assets by investors. The reason is simply that T-Mobile can continue to grow without necessarily finding or creating new revenue sources. It simply has to keep taking market share. Cable companies are in the same position. Invention is not required.

T-Mobile’s merger with Sprint gave it a trove of 5G spectrum and other assets that arguably mean it will enjoy at least a temporary lead in 5G coverage and, soon, speeds across its footprint. And T-Mobile has been taking 4G share for years.

AT&T and Verizon, on the other hand, have had to spend heavily to acquire 5G spectrum, and also face market share losses to T-Mobile and cable operators. That being the case, they need new revenue sources to justify that spending.

So though there are two different ways of looking at 5G, the immediate boost in revenue from 5G is coming either from higher market share (T-Mobile) or higher ARPU (Verizon).

The first view is that 5G, by design, will support internet of things and other ultra-low-latency applications that 4G actually cannot. The foremost defenders of that view tend to be infrastructure suppliers, for the simple reason that this argument tends to spur purchasing by mobile service providers. That is a longer-term potential source of growth.

The second view is simply that mobile networks get upgraded about every decade, to support higher bandwidths and lower costs per bit, so the immediate advantage is simply lower cost per bit.

Mobile service providers tend not to want to talk about that so much, for the simple reason that investors never are too excited about capital investment that essentially is “maintenance” spending, rather than investment to capture new revenue sources.

But lower cost per bit enables the “unlimited” offer, which leads to higher ARPU. Lower cost per bit also enables home broadband using the mobile network. So 5G, by enabling lower cost per bit, also makes possible home broadband services using the mobile network.

In that sense, 5G enables fixed wireless for home broadband, a new revenue source.

Gary Kim was cited as a global "Power Mobile Influencer" by Forbes, ranked second in the world for coverage of the mobile business, and as a "top 10" telecom analyst. He is a member of Mensa, the international organization for people with IQs in the top two percent.

Subscribe to:

Comments (Atom)

-

We have all repeatedly seen comparisons of equity value of hyperscale app providers compared to the value of connectivity providers, which s...

-

It really is surprising how often a Pareto distribution--the “80/20 rule--appears in business life, or in life, generally. Basically, the...

-

One recurring issue with forecasts of multi-access edge computing is that it is easier to make predictions about cost than revenue and infra...