Definitions always matter, and especially so when considering eligibility for government funds to support whatever business a firm happens to operate. Lots of people disagree that the U.S. federal government definition of “broadband” should remain at 25 Mbps/3 Mbps. And, over time, the definition will be changed. The only question is when, and to what minimum level.

So some advocate a minimum broadband definition of 100 Mbps/100 Mbps. Support for that definition includes some in the U.S. Senate. As always, there are trade offs and business implications.

Capital investment requirements; efficient use of scarce capital; user behavior; willingness to pay; current and anticipated usage profiles all are important. Cable networks have an advantage in basically having upgraded virtually all U.S. plant to gigabit speeds downstream. Upstream improvements are much more difficult, costly and time-consuming.

How the upgrades can happen within the feasible limits of today’s business models, for all would-be suppliers, is key. Government subsidies are important at the margin, but most of the upgrade activity has to be undertaken by private suppliers.

And that means there must be a clear understanding of how the upgrades fit the business models. In that respect, the upstream definition will be more challenging than the downstream definition.

Up to this point, the key element in the broadband definition has been downstream speed, as that remains arguably the most-important single numerical indicator of “quality.” But all observers agree that upstream speeds now are more important. And that is the rub.

Telcos and independent internet service providers can rip out copper and replace it with optical fiber access at a faster pace, to be sure. But the business model is challenging. Were it not so, they’d already have done so.

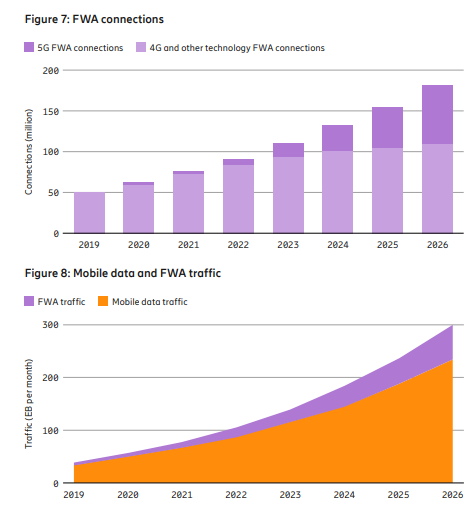

5G, fixed wireless and satellite networks also would be challenged to supply 100 Mbps upstream, though there is a path to incremental downstream upgrades that do not break the business model.

For the majority of U.S. households and locations served by cable TV networks, the 100/100 standard would be troublesome only in the upstream direction, but still would require reworking of most of the physical plant.

For telcos the challenge would be far greater, requiring a replacement of copper access facilities. For every fixed network operator save Verizon, the 100/100 definition would require ripping out and replacing a majority of physical plant.

Rural areas of low housing density would be especially troublesome.

Though cable operators might have a more-graceful upgrade path, telcos generally must rip out the existing legacy network and replace it with entirely-new infrastructure to meet the 100 Mbps minimum upstream standard.

Estimates vary, but a huge telco capital investment would be required to meet a 100/100 minimum. Customer demand is an issue, but less an issue over time, as most consumers now buy faster services than they used to, and often pay more money than they used to, for broadband service.

The 100 Mbps downstream goal is more realistic. About 49 percent of U.S. residents buy fixed network service operating between 100 Mbps and 200 Mbps.

Nearly 32 percent buy services running faster than 200 Mbps.

But a significant percentage choose to buy services operating at lower speeds. Some 20 percent of all customers purchase services running no faster than 75 Mbps, according to Openvault data.

We can argue that 80 percent of the market already buys service at speeds as high, or higher than, the proposed 100 Mbps minimum definition. But 20 percent of the market does not do so, possibly because they cannot buy anything else, but many also might choose not to buy service at 100 Mbps.

source: Openvault

Setting a higher minimum definition will happen. But it matters what the definition entails. Virtually no platforms could meet the 100 Mbps upstream definition quickly. FTTH networks could do so, but only at a cost that stresses the current business model.

And that matters. If 54 million U.S. homes are served by fiber to premises networks, and there are about 138 million total U.S. homes, then fully 61 percent of telco passings would have to be replaced to meet the 100/100 standard.

One might argue that fixed wireless, 5G or some other network could meet the 100 Mbps downstream speed. But none of the other networks are engineered to support 100 Mbps in the upstream path.

More than anything else, it is the impossibility of practical mass market networks hitting the 100 Mbps upstream speed that is the key problem.