Lumen Technologies has said it is willing to consider divesting non-core assets that could include up to 18 million access lines, mostly found in rural and other lower-density areas. That might be a tall order.

The traditional rule of thumb for fixed networks in the U.S. market is that service providers make money in dense urban areas, break even in suburban locations and lose money everywhere else, including rural areas. The same sort of logic applies to fiber to home facilities: FTTH always makes most sense in urban areas, sometimes makes sense in suburban areas and most often requires subsidies in rural areas.

That likely still is a reasonable assumption, both in facilities-based competitive markets as well as those based on a single network and wholesale access.

So Lumen has to find a buyer willing to bet it can take the “least desirable” fixed network service territories and upgrade them for higher-performance broadband access, relying on that one anchor service to support the business model.

That represents a key change in payback models for fiber to home investment. For a few decades, the business logic was that the FTTH upgrade would be driven by a few anchor services: broadband, voice and video entertainment.

Ironically, the justification for fiber-based networks supporting internet protocol was that they could “support any media type.” The new assumption is that a new FTTH network will mostly be supported by broadband access. Most independent internet service providers, for example, have migrated away from offering voice plus broadband, or broadband plus video, to offering broadband only.

And, of course, it is harder to create an attractive payback model based on a single service than on two or three relatively popular services.

Whether in a wholesale or facilities-based competition model, where the hope once was that three anchor services would support the business model, it increasingly is the case that a single revenue stream--internet access--anchors the payback model. That broadband-led model arguably requires much more stringent cost control than an incumbent cable or telco business model.

To be sure, telcos and cable operators continue to earn significant revenues from either voice or video services. But internet access is viewed as the revenue driver going forward. All of which makes the facilities-based independent internet service provider business model so relevant.

The issues include not just infrastructure cost but also competitive dynamics. In an overbuild situation any independent provider of new FTTH services must compete against two incumbents. Even when that is not the case, few telcos can expect to grab more than 40 percent to 50 percent market share of broadband connections.

In the more-favorable two-provider scenario, it will be tough for a telco to justify an FTTH business case based primarily on the value of internet access services, though some independent ISPs, with lower cost structures, claim they can make a profit even at low housing densities.

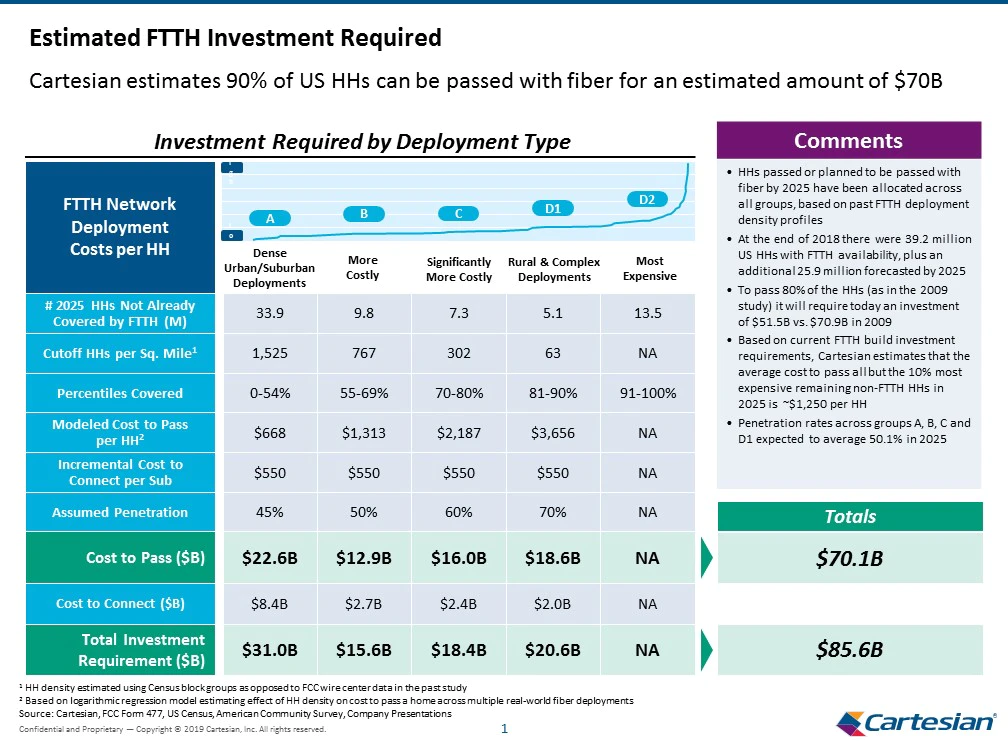

The total cost to build FTTH systems in rural Vermont was about $26,000 per mile, which included absolutely everything (NOC, main pass, laterals, drops and customer installs for six customers per mile) and a 12 percent contingency cushion, according to Timothy and Leslie Nulty of Mansfield Community Fiber.

“Just six paying customers per mile can be profitable,” they argue. Vermont’s density averages 12 people per mile, so six paying customers means a 50 percent take rate, which we always achieved by the end of the third year.

Other estimates suggest per-mile costs in the $18,000 to $22,000 per mile range, so the Mansfield figures do not appear out of line. On a “homes passed” basis, some estimate a network cost of less than $700 per passing in urban and suburban areas. In rural areas the cost per home might be in the range of $3656.

Those costs typically do not include the additional cost to serve a customer, which might double the full cost per customer. Most would agree equipment costs have declined over the past decade, though construction costs arguably have not.

Assume costs in urban areas ranging between $670 per passing and $1313 per passing, representing perhaps 70 percent of all households.

Assume customer premises equipment and installation labor adds $600 to the cost of serving an internet access customer on an FTTH network. Assume 40 percent take rates and an average cost per passing of $1,000.

That implies a cost per customer of about $2500. Assume internet access revenue is $80 a month, or $960 per year. Payback on invested capital might take a while, assuming 20 percent net margins after loading marketing, operations and other costs. Annual net profits might be as low as $192 per customer in that scenario, with break even happening in a decade and a half or so.

That will be a tough proposition. Independent ISPs operate with higher margins because their costs are far lower. Telcos and cable companies, on the other hand, do have additional revenue streams (voice and video).

All those are issues Lumen Technologies faces as it ponders the sale of its copper-based networks in rural and other lower-density areas.