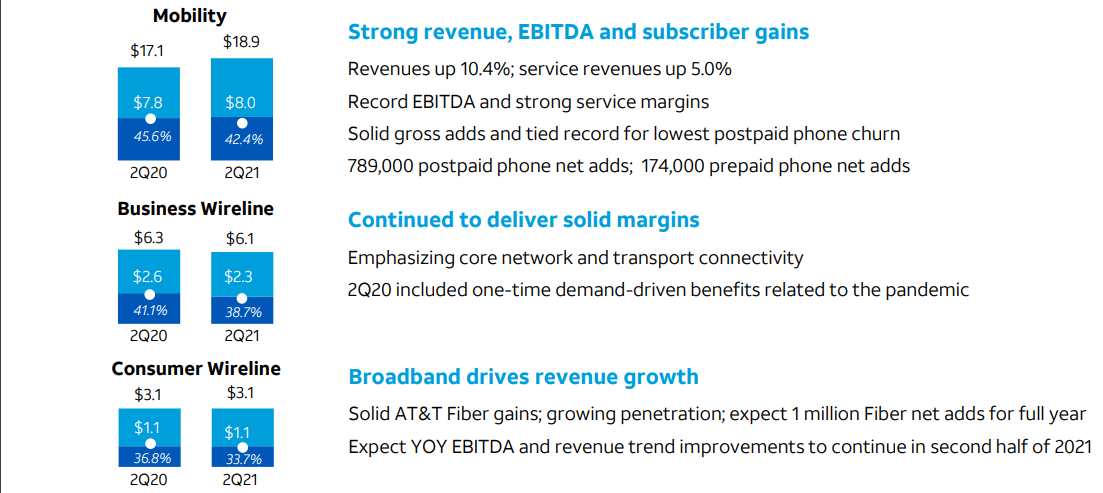

As is the case for Verizon, AT&T’s financial results hinge on its mobility unit performance. As always, it is helpful if revenue contributions from consumer fixed network and business services hold their own, but marginal improvement is driven by mobility segment performance.

Verizon’s second quarter 2021 results show the same pattern. Revenue growth is driven primarily by consumer mobility services. Business customer revenue was flat sequentially.

T-Mobile has no fixed line business, so all of its growth comes from mobility services. Also, T-Mobile has zero share of fixed network services for consumers, so will seek growth by taking home broadband share from cable operators and others. In its mobility business, T-Mobile has been under-represented in mobility sales to businesses, and will try to wrest share there as well.

New lines of business remain important for all three firms, though opportunities vary. The easiest path for an attacker in any market is market share gains, as one can see with T-Mobile over the last decade. Incumbents have far fewer opportunities, but even so, gaining share is still possible outside the existing geography, which is what Verizon banks on with its fixed wireless services.

AT&T has other constraints. It is the share leader in fixed network geography. So it has relatively less to gain if it seeks additional fixed network share outside its fixed network footprint (and regulators might not allow it to do so). AT&T plans to take additional mobility share, but

The company also has fallen to third in mobility account share, so it will try to recapture some share there. The constraints are T-Mobile’s higher rate of growth and the coming impact of competition from Dish Network and cable operators as well.

The point is that T-Mobile and Verizon are better placed to grow by taking market share in existing markets. AT&T is almost forced to look for growth elsewhere, as its opportunities to grow by taking share in existing markets is more limited.

Though the strategy has been panned by most observers, AT&T’s forays into video entertainment and content were driven in large part by that set of circumstances. The company simply could not grow revenues and cash flow significantly by taking market share, in any of its major lines of business.

Despite spinning out its Warner Media and DirecTV assets, AT&T still will capture 71 percent of the revenue and cash flow from both assets, even as those assets are removed from AT&T’s books.

Most characterize the asset dispositions as a case of AT&T “getting out of” the content business. It might more properly be characterized as moves to reduce debt by monetizing some of the value of those assets, while retaining 71 percent of the cash flow and business upside, while allowing its workforce to concentrate on growing the mobility business.