Are a few dominant mobile app stores better understood as being distributors or platforms? And if either case, what are the implications for antitrust or competition policy, if any?

Regulators care about such things, as monopoly or oligopoly power can exist in any supply chain. Perhaps few distributors tend to have market power over a whole supply chain, though it is conceivable. Almost every platform that operates at scale has power.

A distributor traditionally moves products or services between a supplier and an end user or customer; part of the supply chain.

A platform is a marketplace or exchange, when used as a business model. In another sense, as traditionally used within the computing industry, a platform is software or hardware upon which other software or hardware can be built.

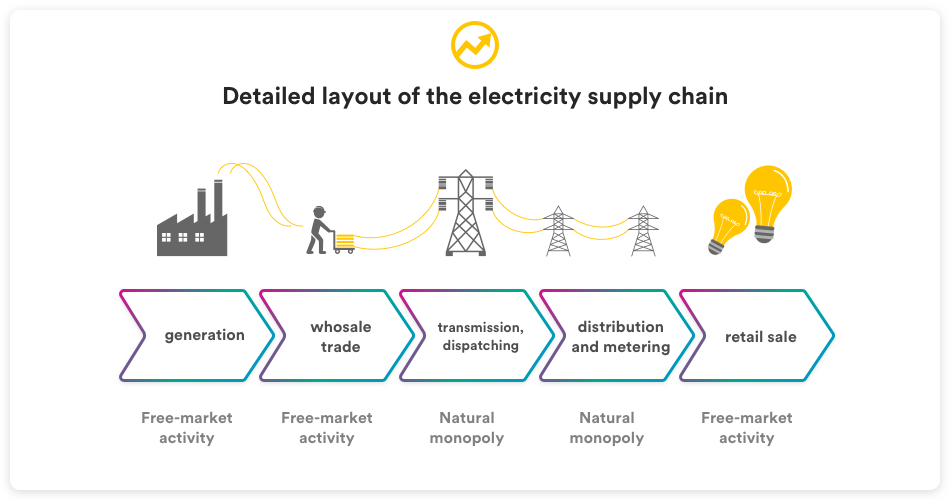

We typically think of supply chain market power as existing either on the final end consumer or product or service producer sides of any supply chain. The classic exceptions are electricity, natural gas, water supply or sewage suppliers, which tend to be viewed as natural monopolies.

Telecom services once were viewed as natural monopolies globally until the mid-1980s, when a wave of deregulation and privatization began to sweep the industry. What is salient is that telecom service providers are distributors.

One might argue that telcos also create some products, such as voice communications, messaging or data transport.

That is true, though the ability to do so also rests on infrastructure supplied by others in the value chain to the left of the distribution function.

Telcos also use indirect distribution partners as well as direct sales to customers.

The point is that market power in a supply chain (monopolies or oligopolies) can exist at many points in a supply chain. And though it is not the first instance that comes to mind, it can be possible for end user consumers to have something like “monopoly” power in a supply chain. The best example is military products, which might essentially have “one” or “just a few” potential buyers.

The issue is, as some argue, that in some cases, supply chains are no longer the central aggregator of business value. “What a company owns matters less than what it can connect,” some might say.

All that might matter for regulators. Distributors might, or might not, have power in a supply chain. A dominant platform--by definition--typically does have market power.

Two angles are worth noting. While app providers chafe at the revenue sharing that dominant app stores, for example, have charged (as much as 30 percent, in the past, perhaps 15 percent now), that arguably is a “cost of distribution” expense for any particular app owner.

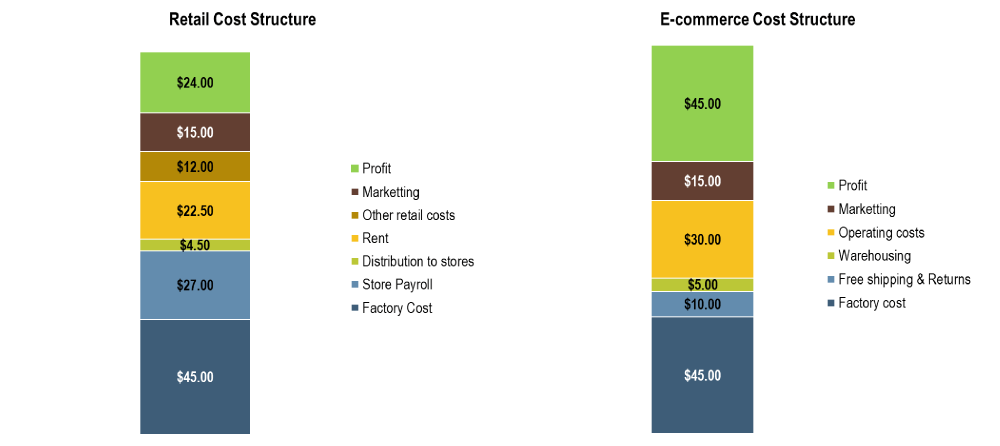

In other industries, the cost of distribution might range from five percent to 80 percent of retail sales amounts. The point is that if the dominant app stores represent distribution and retail costs, then there is an argument to be made that 15 percent to 30 percent is not necessarily outrageous at all.

Whether a product is “digital” or not, there still are sales, marketing and distribution costs. Clothing and apparel products typically have high distribution costs (including sales, marketing and logistics). But online sales are more profitable than other retail-based distribution methods such as “in store” sales.

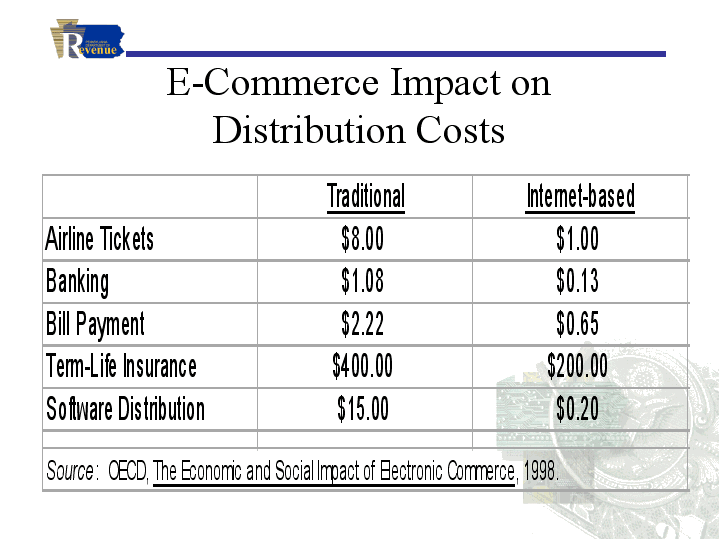

In the case of software distribution, a mobile app store platform adds significant value by slashing distribution and sales costs by as much as two orders of magnitude. The argument that a 30-percent revenue share is inherently unfair does not stand up to reason. The distribution cost is sliced by two orders of magnitude. That is worth a considerable amount.

The second issue worth noting is that powerful app stores also arguably have market power. That seems a more-serious issue, as the inability to appear in Apple’s or Google’s app stores would force app developers to create their own marketing and distribution channels.

That is not a problem for enterprise or business-focused app suppliers, who normally create their own distribution and marketing and sales channels.

It arguably is a huge problem for small developers who create consumer apps. And that is where monopoly danger arguably lies.

As an aside, the concern expressed over the last decade about internet service provider monopoly dangers seems almost comical, in retrospect. ISPs not only face competition, they play only small roles in the application ecosystem.

They are not gatekeepers in the same way as Google Play or the Apple app store have become. They cannot block a lawful application. They cannot prevent a lawful app from being distributed.

To reflect on the original question--whether app stores are distributors or platforms--they seem to be both. App stores are a dominant way app developers market their products. So app stores are distribution. They also are marketing and direct sales channels.

But app stores resemble platforms in some ways. They connect buyers and sellers.

Viewed as distributors, a commission or fee of 15 percent to 30 percent has never struck me as unfair, given the percentage of revenue earned by the suppliers of distribution functions in other industries.

Viewed as platforms, the danger of monopolization and anti-competitive behavior always has seemed much clearer.