Digital business remains the top business priority of enterprise boards, a survey by Gartner confirms. Some 58 percent of boards said digital technology initiatives are the single biggest strategic business priority. What that means might vary.

If digital business “is the process of applying digital technology to reinvent business models and transform a company’s products and customer experiences,” then simply digitizing existing processes is not what boards might mean.

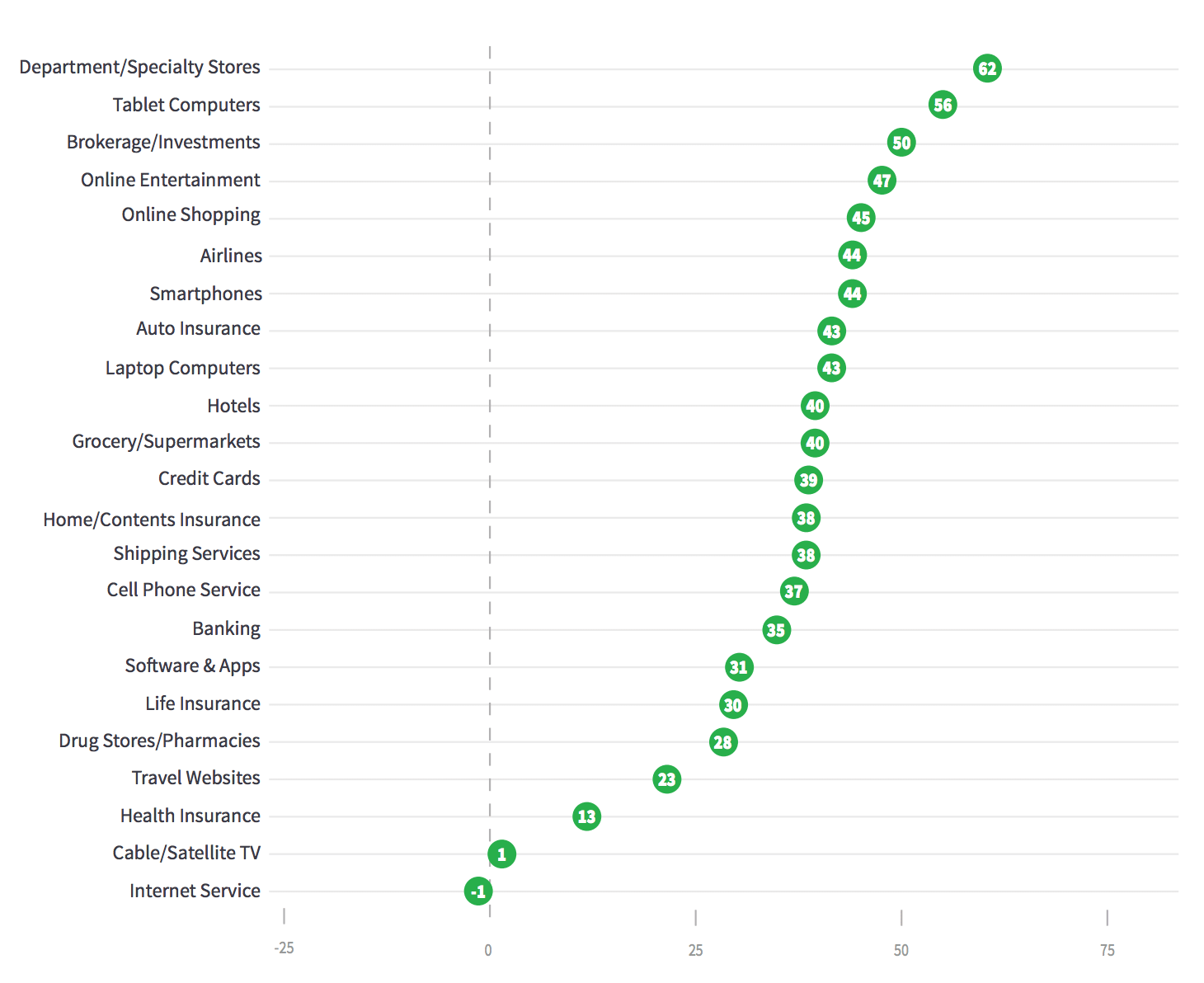

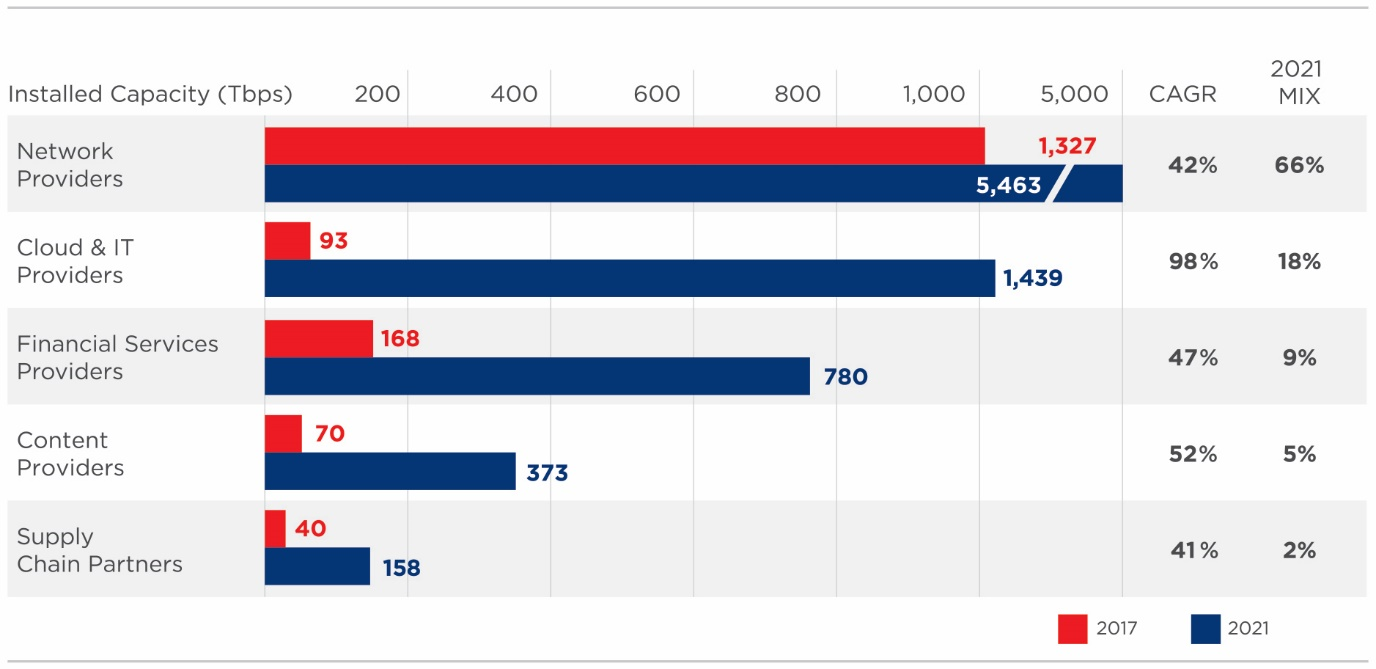

source: Simon Torrance

Aside from the perhaps-obvious goals of creating new products, services and experiences, digital business more fundamentally includes “reinventing how they interact with their customers, employees and partners” and “creating disruptive business models.” All that requires a clear understanding who customers are, what they want and how revenue is generated from those customers.

That begins with understanding the dynamics of the core business, more than understanding how technology is applied. Make a mistake with the former and the latter, in all likelihood, will amount to almost nothing.

That remains true for efforts to create platform business models or “platforms” in the connectivity business, for example.

source: Simon Torrance

Among the other issues, at least for connectivity providers, is the reluctance of equity and financial markets (more accurately “opposition”) to fully value mixed or conglomerate business models. In other words, the valuation of a connectivity asset is one thing. The valuation of a digital infrastructure asset is another thing. The valuation of a software asset or marketplace or exchange is something else as well.

There always is pressure to create clear assets that can earn the appropriate valuation, typically because the other assets get a higher valuation multiple than the core connectivity assets. That makes it hard for lower-value connectivity assets to add higher-value functions and assets under one umbrella, as financial markets will always demand separation.

Among the practical solutions is to allow separation, but retain an equity interest in the separated assets, allowing an owner to participate in the equity upside and the cash flow. That portfolio model will not be instinctive for connectivity asset owners, but is one way out of a conundrum.

Ideally, a firm would like to participate in faster-growing, higher-valued parts of the ecosystem, without facing constant pressure to spin out those assets so they can be valued appropriately.

Any connectivity provider that finds success in any higher-valued line of business will face pressure to divest, spin out or sell such assets, relegating that firm to the original core business, albeit with one-time upside from asset dispositions.

That “create to sell” mentality typically does not fit with a connectivity provider mindset, capital and human resource assets or manager time frames (which are often far shorter than required to create sizable new assets out of the core).

But even in the core connectivity business, patient capital might be necessary. That accounts, in some part, for the roles now played by “more patient” capital and the involvement of private equity in many connectivity settings.