Digital infrastructure is a term increasingly used by suppliers of connectivity services. But digital infrastructure arguably includes the rest of the information and communications ecosystem as well. To the extent that digital infrastructure includes connectivity, computing, applications and services as well as devices, it is synonymous with “internet ecosystem.”

When used in the more-narrow sense of “connectivity infrastructure,”however, some connectivity assets are of growing interest to private equity, institutional investors and others, as a form of alternative investment providing diversification.

As investment organizations sometimes desire to hold assets such as land or real estate, they now sometimes wish to own infrastructure assets that throw off predictable cash flows, have business moats and stable and recurring demand.

That interest on the part of buyers also accounts for service provider interest in monetizing some parts of their access infrastructure, steps that might not have been deemed wise decades ago, when ownership of scarce facilities was viewed as a primary source of business advantage.

But digital infrastructure now sees a confluence of supply and demand interest as much private equity views investments in digital infrastructure the same way other long-lived infrastructure (transportation, utilities, real estate) is seen: reliable providers of long-term cash flows.

So in addition to investments in infrastructure related to clean energy, water, and wastewater, some investors see digital infrastructure as part of the mix.

The capital-intensive nature of these assets also creates barriers for competition, while demand growth is robust. Still, infrastructure investing--digital or not--is an asset class expected to deliver low returns, but also with low volatility.

At the same time, interest in alternative asset classes and low dividend yields on bonds contribute to the interest in digital infrastructure asset investment, and the trend to monetize such assets on the part of service providers.

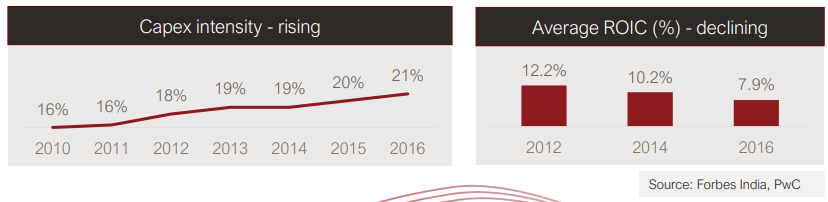

In substantial part, there also is corresponding interest on the part of infrastructure owners to monetize assets, driven in large part by increasing capital requirements and declining return on investment.

In Asia, for example, communications infrastructure faces higher capital intensity and yet lower returns on invested capital. In that sense, communications infrastructure faces potential investment gaps similar to those of other infrastructure categories.

That accounts for the prevalence of interest in “capital light” business models, public-private partnerships, wholesale access service models and privatization of assets.