Infrastructure investors are playing a bigger role in access network capital investment, often for the same reason they invest in airports, seaports and other forms of long-lived infrastructure. They see “moats” and stable, long-term demand with predictable cash flows.

As did other investors of 30 to 40 years ago, connectivity infrastructure and the cash flows built on it are seen as relatively stable sources of free cash flow bolstered by their relative scarcity. It started with cell towers but increasingly is moving towards optical fiber access networks, small cell network providers and data center infrastructure.

All of that raises new questions about where value lies in the connectivity business. To use the obvious analogy, money can be made operating a seaport or airport as money is to be made moving goods from manufacturers to end users and retail buyers.

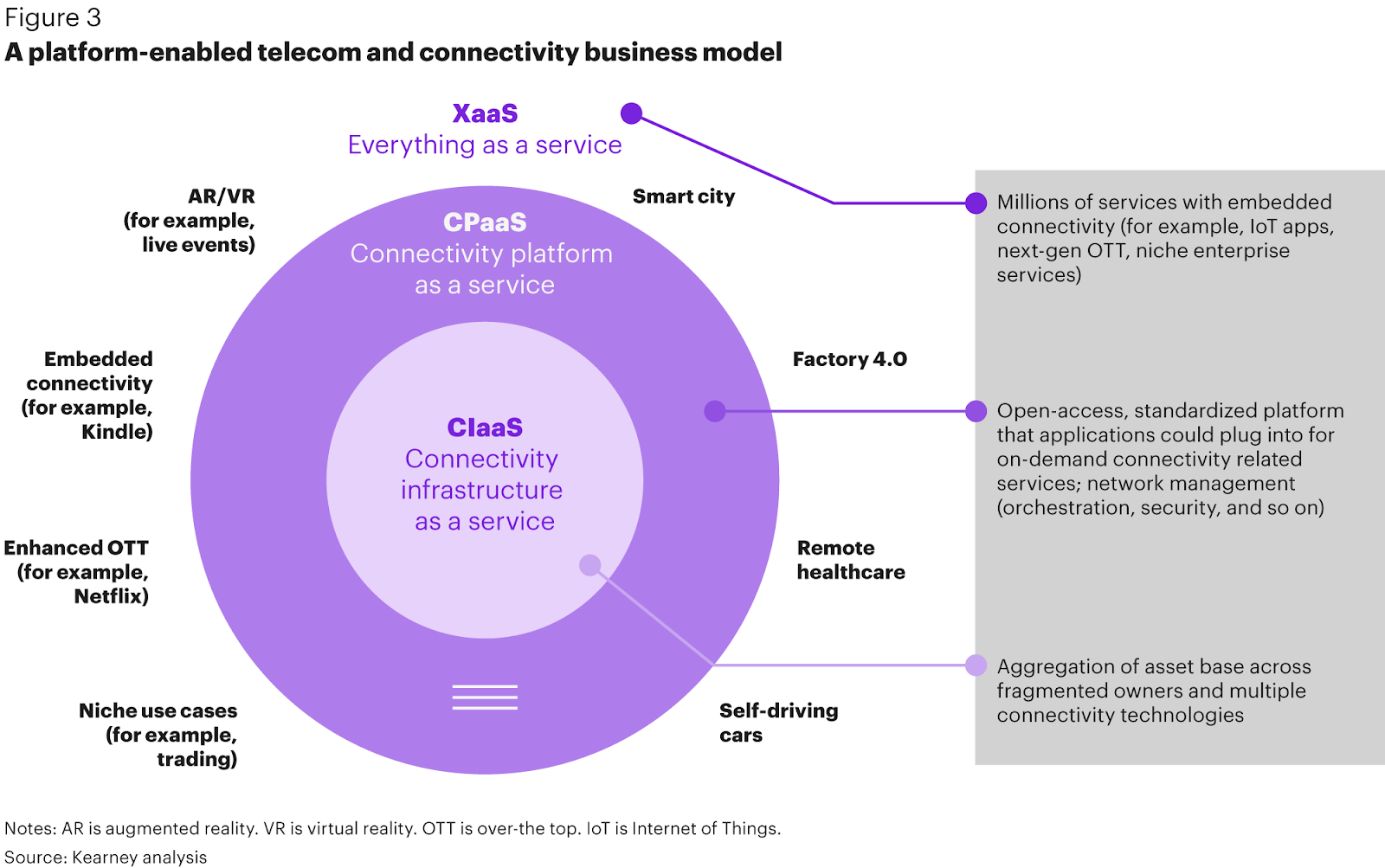

The best connectivity industry examples are wholesale access platforms, where one entity owns the infrastructure and retail service providers all use the one infrastructure.

The business choice between facilities-based versus leased network access is an issue in other contexts as well. At scale, the former tends to offer better economics than the latter. That is why the leading mobile service providers in almost-all markets own their own networks.

At lower volumes, and especially “outside” the core geography, leased access typically offers better economics.

Hybrid models seem to be developing, though, where the access infrastructure is partly owned by a service provider and an infrastructure investor. The advantage is lower capital investment by the service provider, at the cost of shared revenues and profit.

Monetization opportunities will often depend on the ability to sell infrastructure access to multiple buyers, where traditionally a network has been virtually exclusively for the use of the network owner or its wholesale customers. As data centers arguably do best when they are “carrier neutral,” access assets might in some cases also benefit from multi-customer business models.

Indoor coverage by small cell networks provides an example. It will make sense for all mobile operators to take advantage of an indoor coverage network, for example.

It is not yet clear just how far changes in the physical platform could evolve. It might be fair to say that if value tends to migrate elsewhere in the ecosystem or value stack, away from the “access” function, such moves create new possibilities.

As networks increasingly are virtualized, it is conceivable that a new division of labor could develop in some markets, with asset owners providing physical facilities and other participants providing the service enablement or services.

As we presently see with wholesale-only infrastructure, one entity might provide the access functions, while all retail service or app providers pay to use that infrastructure. Though this might always make more sense for fixed networks, even mobile networks might eventually consider such a pattern, if capital intensity were to increase for future very-dense networks.

As we have already seen, perhaps a consortia of mobile operators might join together to create and own the physical plant. The odds of such developments increase with potential infrastructure intensity and cost.