Facilities-based access network business models are changing, and higher levels of government spending to bring down costs for networks in rural and other high-cost areas is among the reasons. The 2021 passage of an “infrastructure” bill by the U.S. Congress will reduce costs in several ways.

The bill includes $42.45 billion in grants to states for broadband projects, which can range from network deployment to data collection to help determine areas that lack service. Not all of that money will build infrastructure, to be sure. But much will. And the plan allocates at least $100 million in funds to every state, with lesser amounts to U.S. territories.

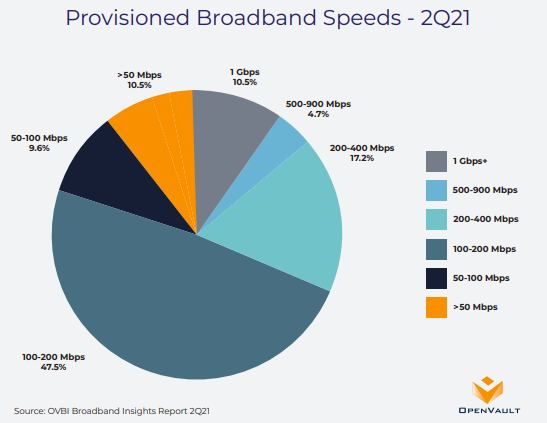

source: S&P Global Market Intelligence

If the money is not wasted, the cost of adding new internet access facilities should fall. Also, additional locations could find they are upgraded to increase connection speed.

There also are provisions that will stimulate demand. The bill allocates $14.2 billion for consumption subsidies. To be sure, there have been subsidy provisions before. But the new bill widens eligibility for such subsidies.

Included in the bill is a $30-a-month voucher to low-income Americans to pay for internet service.

This program replaces the temporary $50-a-month Emergency Broadband Benefit program that was part of efforts to sustain the economy during the period when work and schooling were mostly shut down, offering less money monthly, but increasing the number of those eligible.

Another demand stimulation effort is the allocation of $2.75 billion for digital inclusion and equity projects, such as improving digital literacy or online skills for seniors.

Additionally, $2 billion was allocated for rural broadband construction by U.S. Department of Agriculture, as well as another $2 billion for a Tribal Broadband Connectivity Program run by the National Telecommunications and Information Administration (NTIA). Both ideally will help create new facilities.

The bill also allocated $1 billion to build "middle mile" infrastructure to connect internet service providers to internet access points.

Finally, $600 million was authorized for bonds to finance broadband deployment projects in rural areas.

All that amounts to stimulating demand and supply of internet access, ideally. Undoubtedly some of the money will be wasted.

But that much additional demand and supply stimulation is going to change business models for the better in many cases, directly lowering the cost of building facilities and defraying consumption as well.

That is among the reasons many telcos are boosting their spending on fiber to home projects, AT&T, Lumen Technologies and Frontier Communications among them, and why other firms such as T-Mobile and Verizon are dramatically investing in fixed wireless on a national basis.

Business models are better on the demand side, while the cost of such facilities is lower on the supply side.