Many in the mobile ecosystem ask the question “how will we make money from 5G? Fixed network operators have been asking themselves similar questions--"how do we get a payback from fiber-to-the-home?"--for several decades.

For mobile or fixed network operators, competition and changing demand make payback models uncertain and challenging. Where facilities-based competiton exists, the infrastructure cost per customer account always rises.

Stranded assets are the reason, though more an issue for fixed networks. In a monopoly market, the single provider might hope to get close to 98 percent take rates. In a competitive market with two equally-capable providers, each provider might hope to get 50 percent share of the installed base.

That effectively doubles the network cost per customer, as revenue is earned from about half of locations passed. In markets with three or more facilities-based competitors, cost-per-account increases more.

Demand changes also effect payback models. Fiber to the home once was underpinned by the assumption that there would be high demand for up to three services (voice, video and internet access).

As demand for fixed network voice and linear video subscriptions declines, the business model increasingly is built on home broadband. Voice and linear video help, but both are expected to keep declining.

But that has key revenue implications. Where a home location might have been expected to generate revenue of $80 to $200, the growing reality is that a location is expected to generate perhaps $50 in home broadband revenue, and then some amount of voice or other revenue from some locations.

Basically, revenue expectations--average revenue per customer or location--are effectively cut in half. That forces changes to the payback model on the cost side. Basically, costs must drop.

Those savings can come from intrastructure cost declines; operating cost drops; higher subsidies; lower maintenance costs; lower headcount and overhead or any combination.

The key point is that revenue assumptions for fixed networks increasingly are founded on lower gross revenue assumptions; revenue from additional sources; shared costs between mobile and fixed networks and more importance attached to defending market share or taking market share.

The parallel question asked by mobile operators--"how do we make money from 5G?--embeds some of the same issues faced by fixed network operators.

What the question likely means is less an uncertainty about revenue drivers and more a concern about the distribution of value within the ecosystem: will mobile operators reap a fair share of 5G benefits (higher revenue, higher profits, higher market share, lower operating costs)?

Looking only at consumer retail costs--exclusive of experience advantages such as higher speed; lower latency; new services or capabilities--it is not yet completely clear that average revenue per 5G account is higher than 4G ARPA.

5G has proven to generate higher ARPA in some markets, however.

It is a virtual certainty that 4G and older connections will be replaced by 5G. So the baseline for 5G revenue is 4G revenue. Beyond that, there is expected upside from private networks, network slicing (virtual private networks), edge computing and new enterprise connections to support internet of things use cases.

To be sure, many wonder whether “we can charge more for 4G?” The long-term answer is not yet knowable, but the practical answer might well be “yes.”

And that can be true even when direct tariffs for 5G are not that different, if different at all, from 4G tariffs. Some mobile operators do not charge a premium for 5G, but expect to gain market share, which drives higher 5G revenue.

Other service providers provide incentives for customers to use 5G but with a price increase coming in the form of unlimited usage. The actual driver of higher revenue per account is the shift to a higher-priced “unlimited usage” tier, not 5G as such, though such plans include 5G access at no extra charge.

And though we have not seen it much, if at all, some mobile operators might decide to institute speed tiers for mobile service that mimic the ways access is sold on fixed networks. Customers might be offered lowest prices for lowest speeds; mid-tier pricing for mid-tier speeds and premium prices for the higher speed tiers.

But there is another sense in which the question of “how will we make money from 5G?” can be understood.

Customers got value in terms of higher speeds when 4G was introduced. Mobile operators expected to sell more data, which would generate more revenues, and also create new services that would further increase revenues.

But tough competition in many markets meant that mobile operators were not able to charge a price premium for 4G access. So the benefits went largely to consumers, according to ING analysts. “They got more data, better speeds and often paid less,” ING says.

Governments also raised billions in revenue from spectrum auctions.

So one way of understanding the question about 5G revenues is the distribution of value and revenue for mobile operators within the 5G ecosystem. The downside for mobile operators is lower recurring revenues from 5G, compared to 4G.

“Operators do not want to repeat these mistakes” seen in the transition from 3G to 4G, ING notes. But some might argue that the long-term trend will be difficult to break.

source: Statista

source: Strategy Analytics

source: Researchgate

Taking market share, shifting customers to pricier accounts and increased usage charges are the immediate ways mobile operators have boosted 5G revenues over 4G levels.

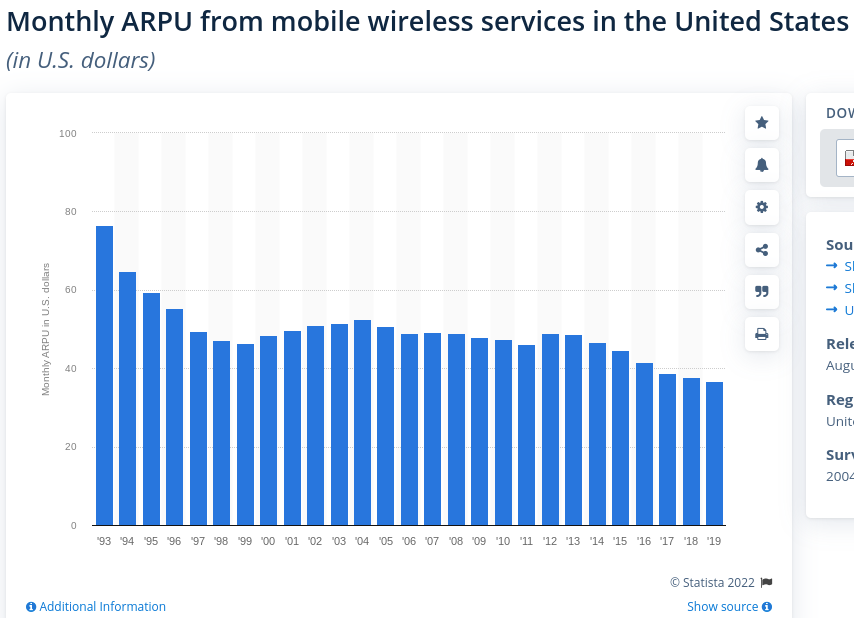

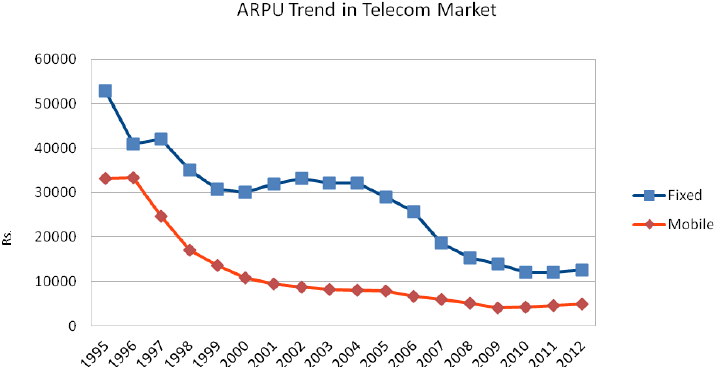

Longer-term pricing trends, though, might be difficult to change, as prices have been declining since 1996.

On the other hand, the whole reason we see a next-generation mobile network about every 10 years, since 3G, is that capacity demand by customers keeps climbing. And while mobile operators can increase effective capacity using small cells and better radios, at some point an increase in spectrum is required.

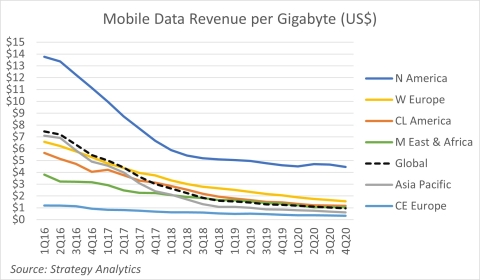

Also, as modulation and coding gets better with each successive generation, the cost to deliver a bit drops, allowing mobile operators to supply data consumption demand at lower costs.

So another way to look at the payback model is to ask “what happens to your business if you do not upgrade to 5G?” Defending existing market share is a legitimate business outcome.

Creating a more-efficient data network that supplies demand affordably also is an important business outcome. And to the extent 5G network capabilities are required to support dense internet of things networks, edge computing networks and network slicing, not investing in 5G forsakes any revenue opportunities in those areas.

In many ways, that is akin to the value of fiber-to-home networks. In many cases, higher revenue per account is not expected. The business value instead comes from consumer market share gains, market share defense and the ability to compete in those markets.

There is incremental value in terms of backhaul support for mobile small cell networks or business-grade services for smaller businesses. There is value in reduced operating expenses and possibly headcount.

In other words, there are lots of ways 5G contributes to overall business value for mobile operators that go beyond direct tariff increases.