It appears that Verizon might be both "too optimistic" and also "not optimistic enough" about fixed wireless account growth, all at the same time. In either case, pessimists might be wrong.

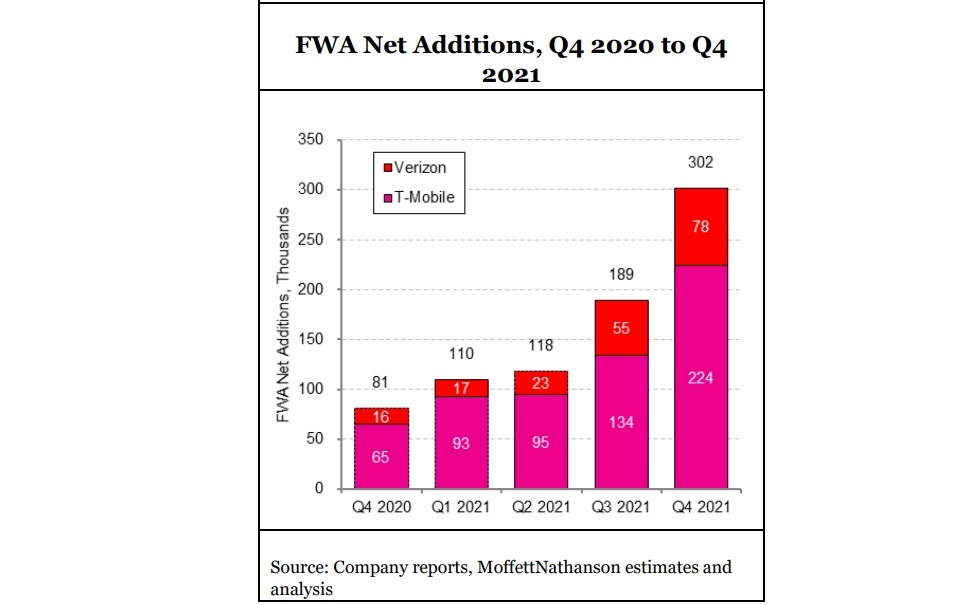

If present trends continue, Verizon might be understating the importance of fixed wireless as a means of gaining home broadband share. In the fourth quarter of 2021, 38 percent of all home broadband net account growth was gained by fixed wireless networks.

It is clear enough that there is much skepticism and hope about about the impact of 5G fixed wireless. T-Mobile and Verizon believe they will be significant winners in terms of taking home broadband share.

Verizon, in fact, believes fixed wireless will provide the initial incremental revenue upside from 5G, generating more additional cash than longer-term opportunities such as edge computing. Nobody would accuse T-Mobile of being too pessimistic, however.

T-Mobile expects to have between seven million to eight million fixed wireless accounts by 2025, and views an addressable market of about 30 million homes that are suitable from a signal quality and capacity standpoint.

Craig Moffett, analyst with MoffettNathanson, views T-Mobile's forecast, which implies 23 percent to 30 percent penetration of addressable homes, as an "arguably absurdly ambitious target."

But T-Mobile could be proven correct, and not chasing an overly-ambitious goal, to a point. If one assumes T-Mobile gets a disproportionate share of its fixed wireless accounts in rural areas, and if one assumes fixed network service providers in those rural areas will not, by 2025, significantly upgraded networks to either fiber to home or DOCSIS 3.1 standards, then T-Mobile could well grab 20 percent to 30 percent market share.

Perhaps the more-germane criticism is what happens in urban and suburban areas, longer term. Eventually, as “typical” home broadband users consume more data, fixed wireless capacity will have to increase as well.

To be sure, there are ways to compete. Millimeter wave assets are an obvious solution. More mid-band spectrum helps as well.

Small cells will help boost usable bandwidth by increasing specrum reuse. And usage patterns will play a role as well. Some argue that peak home broadband will happen at night, when usage of the mobile network is lowest.

Still, there are obvious challenges, if fixed wireless demand scales.

OpenVault data shows that the average U.S. cable broadband household already uses about 434 gigabytes of data per month, roughly 40 times more than the average unlimited usage plan mobile customer.

So if new fixed wireless households impose 434 GB of demand on the wireless network, how many customers can be added before there are capacity constraints? And how well will the coping mechanisms work?

Also, will T-Mobile and Verizon fixed wireless using mid-band assets primarily be attractive to "average" users or the "lighter user" segment? And will Verizon's millimeter wave network be extensive enough to reach further up the scale of usage support?

Verizon, meanwhile, is committing to about $1 billion in fixed wireless revenues by 2024, which MoffettNathanson believes implies 1.7 million customers. Verizon both agrees--and appears to disagree.

Verizon suggests it will add 4.5 million net new home broadband accounts by 2025. It also says fixed wireless will represent “more than one million” of those accounts.

The numbers seem incongruous. Fios already has adoption in the 40-percent range. So assume Verizon can boost adoption to 50 percent. That would only add about 650,000 additional Verizon Fios home broadband accounts. The rest has to be fixed wireless or acquired through purchases of existing accounts. The latter is unlikely to happen, so the growth has to be organic.

Nearly all of those accounts would have to be generated by the “out of region” fixed wireless network, to make the numbers work. To be sure, perhaps Verizon is banking on adding millions of new Fios-passed locations.

Verizon says it passes 16.5 million locations with Fios at the end of 2021, and expects to pass 18 million locations by the end of 2025. So add 1.5 million new Fios locations. Assume adoption is at 50 percent. That suggests a potential 750,000 accounts.

All together, that suggests 1.4 million new Fios accounts by 2025, with total net gains of 4.5 million accounts. That implies something more than three million fixed wireless accounts gained by 2025.

The point is that either Verizon seems conflicted about the size of the opportunity, to some extent. T-Mobile is viewed as too optimistic by some. But fourth quarter 2011 share gains by fixed wireless were unprecedented.