Many observers have argued fixed wireless would not be a material driver of U.S. home broadband market share change. Just as vehemently, T-Mobile and Verizon have argued for precisely that impact.

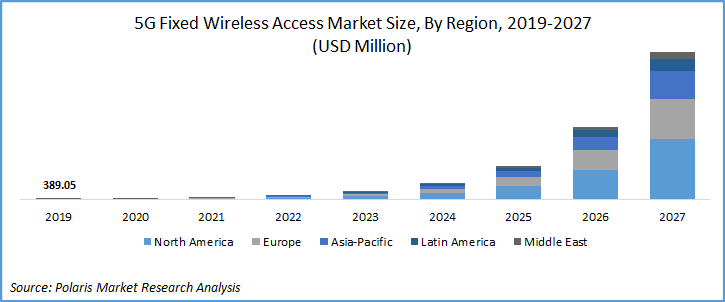

Cable operators say they have not seen material impact, yet. But at least some equity analysts now say fixed wireless will be highly disruptive. Wells Fargo telecom and media analysts Eric Luebchow and Steven Cahall predict fixed wireless access will grow from 7.1 million total subscribers at the end of 2021 to 17.6 million in 2027, growth that largely will come at the expense of cable operators.

source: Polaris Market Research

The impact on the installed base will occur more slowly, but the primary impact will be seen in net account additions. Accustomed to getting as much as 94 percent to 100 percent of net account growth, cable might see net new additions drop to perhaps 30 percent to 35 percent in 2023.

If 5G fixed wireless accounts and revenue grow as fast as some envision, $14 billion to $24 billion in fixed wireless home broadband revenue would be created in 2025.

How important 5G fixed wireless might be depends on which estimates we use for total home broadband revenues, as well as the expected 5G fixed wireless growth rate.

By some estimates, U.S. home broadband generates $60 billion to more than $130 billion in annual revenues. The worse-case scenario for cable operators would be the higher growth rate and the lower revenue base.

If the market is valued at $60 billion in 2021 and grows at four percent annually, then home broadband revenue could reach $73 billion by 2026. $24 billion would represent about 33 percent of total home broadband revenues.

If we use the higher revenue base and the lower growth rate, then 5G fixed wireless might represent about 10 percent of the installed base, which will seem more reasonable to many observers.

Assuming $50 per month in revenue, with no price increases at all to 2026, 5G fixed wireless still would amount to about $10.6 billion in annual revenue by 2026 or so. That would have 5G fixed wireless representing about 14 percent of home broadband revenue, assuming a total 2026 market of $73 billion.

If the home broadband market were $134 billion in 2026, then 5G fixed wireless would represent about eight percent of home broadband revenue.

Keep in mind that telcos and independent internet service providers also are expected to take share using fiber-to-home facilities as well. While Verizon expects most of its net additions to come from 5G fixed wireless, T-Mobile expects virtually all of its net additions to come from 5G fixed wireless.